Welcome to the epitome of seamless collaborations! Our Professional Agreement sample guide is your compass in the intricate world of business contract dealings. Crafted for clarity and precision, this…

continue reading Rating :

Sometimes, it just cannot be helped that unexpected situations that call for emergency cash assistance will come up that our budget plans will fail to account for. Or, if not surprising expenses, it can be expenses that you need to indulge your dreams such as a vacation trip to a country on the other side of the globe or your dream wedding.

Unfortunately, not all of us are granted the money to fund our dreams in an instant. Most of us will have to look for loans and for personal and self-indulging reasons such as a dream house or a pool in the backyard, Personal Loan Agreements often referred to as a Personal Loan Contract or an IOU ‘I Owe You’ agreement plays an essential role in making this happen. Learn more about what this document is and its many types to determine which type fits your situation. You can also start drafting one of your own with 15+ of our downloadable and printable Personal Loan Agreements.

Before one can understand what a personal loan agreement is, it should be necessary to define the general category it falls under which is a Loan Agreement.

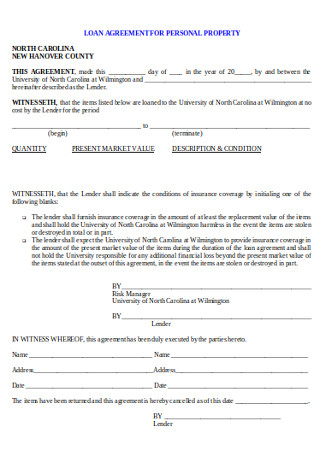

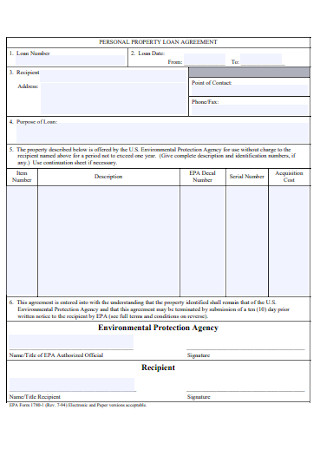

A Loan Agreement is any legally binding agreement that is made between a borrower and a lender, detailing the general terms and conditions both parties will adhere to and to protect them both in case situations such as failure to make timely payments or worse, none at all, will happen.

In most cases, the lending party pulls more of the strings in the agreement as they are the one that’s providing the money which means the borrower has to abide by their guidelines and secure the necessary documents in fulfillment of the financial lending institutions’ requirements. Aside from these provisions, a loan agreement clearly defines the total sum of money that the borrower will be receiving, what it will be used on and the interest rates that will be charged on top of the original loan amount.

In essence, a Loan Agreement legally enforces the borrower to repay the lender the money that was first borrowed plus the interest incurred throughout the whole duration of the loan which must also be thoroughly detailed in the contract agreement as well. As borrowing and lending money entails serious commitment, it must be recognized as such and a Loan Agreement effectively serves as evidence that the transaction does exist and both parties are in mutual understanding of the details regarding the loan.

It is encouraged that most loan agreements be written in form because if push comes to shove, a loan agreement done orally will be difficult to prove in court.

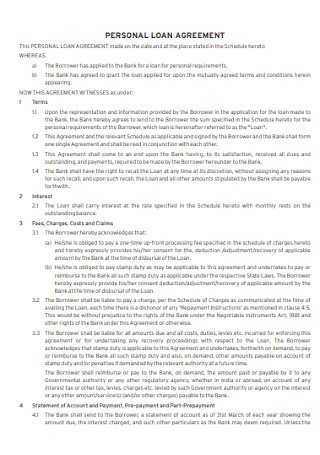

A Personal Loan Agreement is a type of Loan Agreement that is catered for loan applicants who are in need of a loan covering a variety of purposes which mostly include, debt consolidation, wedding budget, honeymoon expenses, home renovations, vacation costs and more personal expenses.

The reasons for a personal loan generally entail only a small amount of money that is to be borrowed compared to other loan types such as Mortgage Loans, Home Equity Loans, and Title Loans. Moreover, it requires money that can be quickly repaid, thus why it’s a loan option that is usually offered by most banks, credit unions and financial lending institutions.

However, this does not mean that strict compliance of the requirements is not to be followed. Lenders still need to ensure that the personal loan applicant is financially capable of repaying the loan due to a personal loan’s nature of being unsecured, meaning in the case that the borrowers are unable to comply with the terms and conditions most times the payments, the lender is not assured that their financial loss can be satisfied. An individual seeking for a personal loan still must provide the necessary documents such as proof of assets, income statements, bank account statements and basically just a quick but thorough financial report that produces a good credit score and verifies their financial capability to repay the loan.

A personal loan is further divided into seven different types. To determine which kind of loan you can be comfortable and are capable of paying for before applying for one, use a budget calculator to garner an estimate of the monthly payments and total interest costs on a loan.

As previously mentioned, most personal loans are unsecured. This type of personal loan does not require a collateral or an asset of your possession that has equal monetary value as your loan. Due to this inability to provide a safety net for lenders when things go astray, they are put in a situation facing higher risks which is why lenders charge significantly higher interest percentage rates on top of the principal loan amount that are proportional to your credit score. A credit score pertains to the rating that the financial institution of choice bestows on you based on their assessment of the financial statements that you have provided in the first process of acquiring a loan that can usually be incorporated in your Loan Proposal. This is a score that ranges from 300-850 according to FICO or Vantage Score whose current version has the same range as FICO’s although some lenders have the power to employ a credit scoring system of their own that they see fit for the situation and the information gathered from the borrower. However, while a credit score can depict a borrower’s creditworthiness, it is not the sole basis of guaranteeing them a loan proposal because other lenders look into a loan application’s credit history and debt-to-income ratio. Repercussions usually faced when a borrower defaults on a loan agreement, fails to make payments or makes late payments is the inevitable wreckage of your credit score that can affect future loan applications.

Secured Personal Loans, on the other hand, are loans backed by collateral meaning, a borrower sets up an asset or a collateral of theirs that a lender can repossess in exchange for repayment failures. Mortgages and Car Loans fall under this type of personal loan as it would usually require collaterals from a borrower that can include but are not limited to: Real estates, cars, jewelries, cash assets, savings account, pensions, stocks and life insurance. Secured loans usually issue a lower interest rate due to the legal ability of a lender to be in possession of the borrower’s collaterals.

Most personal loans are fixed-rate, meaning your monthly payments and your interest rate are consistent and stable throughout the entirety of the loan duration. This way, it is easier to allot money for your personal loans in a budget plan you are encouraged to develop and you can expect the same consistency in the payments avoiding you from any potential financial scares.

Interest rates on this kind of personal loan are offered by banks but are the uncommon option that most borrowers go for. This is because, in contrast to a fixed-rate loan, interest rates are subject to fluctuation that is dependent on the market conditions and an increase in the market will reflect on the rate of your loan and is likely to increase monthly payments as well. While interest rates typically start low for this kind of loan, it eventually starts to pick up once a certain time frame passes; however, the rise of the rates can be issued a limit which the loan agreement shall cover. This way, while the market conditions are facing turbulence and your interest rates can increase, it won’t be as directly proportional to the market changes which means you can still anticipate and predict the monthly payments and budget better. Although the least sought for type of personal loan, it is an offered type for those that are capable of paying off the loan immediately and during the time frame where interest rates are low.

This type of personal loan is usually offered to borrowers who want to pay off existing debts, credit cards, and other personal loans. It collates multiple debts of yours with high interest rates into a single loan which can help decrease overall monthly payments as it also offers lower fixed interest rates and monthly costs. The most important thing in applying for a debt consolidation loan is to be keen on the payment schedule and make sure that the length in paying off debts is reasonable.

A cosigned loan can either be an unsecured or secured loan and is usually offered to applicants who are assessed to be incapable or find difficulty in repaying the loan. This type of loan will only work when a cosigner, as per request by the lender, can take the responsibility of assuming the loan payments if the original applicant were to default. The loan then becomes a secured loan in a way with the cosigner serving as insurance to the lender. It is then important that you have a harmonious relationship with your cosigner and that you both understand the terms and risks associated with this kind of personal loan, one of which is the cosigner facing similar consequences as you if you are to issue late payments that will impact their credit scores.

This kind of personal loan is a flexible one offered by a lender allowing the borrower to withdraw funds for a specified period of time known as the draw period. It functions the same way as credit card wherein you are given access to draw funds within a credit limit for the terms of a loan anytime you choose to as opposed to loans that offer the lump sum when the loan is approved and interest is charged immediately. Personal Line of Credits are usually unsecured loans which means lenders will have to charge higher interest rates. However, lenders can require borrowers to provide collaterals and this way, favorable terms usually a lower interest rate can be secured.

Personal Loans, in fact, most loans in general require three essential documents to validate an applicant’s creditworthiness. These are credit score, credit history and debt-to-income ratio.

1. Credit Score

A credit score is determined after a lending institution applies a formula to the data gathered from an applicant’s credit reports. FICO is an abbreviated term for Fair Isaac Corp who were responsible for first introducing FICO in 1989 despite existing since 1956. Most credit scores follow the FICO score range of 300-850.

A good FICO score ranges from 670-739 and above that obviously means you have a credit range that is indicative of a reliable creditworthiness guaranteeing you with the best loan deals with lower interest rates. Credit scores encapsulate your financial status which is why it is necessary for lenders to extract an applicant’s credit score as it significantly influences decisions on approving one’s loan application. There are five factors that determine how one’s FICO score is calculated and they are as follows:

Despite FICO’s popularity, Vantage Score, created in 2006, is slowly gaining the same reputation as FICO. With an initial range of 501-990, Vantage Score has adopted the same scale that FICO uses which is one thing they are similar with. A Vantage Score was created by the three national credit bureaus, Equifax, Experian and TransUnion, as an alternative to FICO scores employing an advanced formula to produce accurate scores than FICO but it fails to take into consideration “race, color, religion, nationality, gender, marital status, age, salary, occupation, employer, employment history, where you live or even your total assets.”

There are four key factors that Vantage Scores considers in their calculation which are more extensive than FICO’s but have evident similarities.

2. Credit History

Credit History, as indicated in an applicant’s credit report, simply communicates to the lender a borrower’s ability to repay debts and their financial responsibility of managing them. It is a detailed report of the types of credit accounts an applicant is managing including when the accounts were first established, how long they have been managed, the total amount of money that is owed and most importantly, the payment history of the loan applicant. It plays a pivotal role in determining your credit score which is why lenders require the document to be as extensive as possible that also includes bankruptcies, liens or judgements. A credit history that demonstrates an applicant’s prompt payments produces a good credit history and is likely to increase their credit scores which ultimately would give them access to loan deals with lower interest annual percentage rates.

3. Debt-to-Income Ratio (DTI)

A debt-to-income ratio, expressed in percentage, is calculated by dividing your gross monthly income and monthly debt payments. The result is another way for lenders to assess your ability to make monthly payments and ultimately repay the total loan amount borrowed. A DTI with a ratio of 43% is relatively the highest a ratio a borrower can have that can ensure them of mortgage loans but lenders can approve DTIs having 36%.

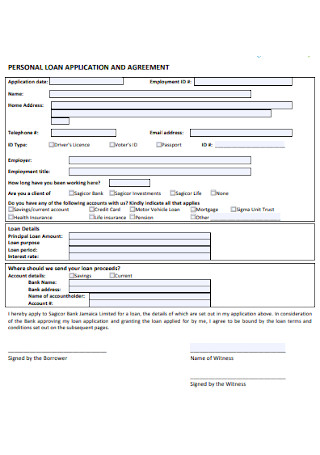

A Personal Loan Agreement is a legally binding document between a lender and borrower that details the amount of money that a borrower requests the lender to fund personal expenses.

A Personal Loan Agreement is composed of basic elements such as: The personal information of the parties involved including the cosigners if need be Transaction Details which includes the total amount owed, the method of payment and the payment terms that are mutually agreed upon. Collaterals which include personal possessions of the borrower that have monetary value.

A Personal Loan Agreement can be a legally binding document when both parties are in mutual understanding of the terms and conditions stated in the document and once signatures are affixed to prove the negotiation is sealed.

Before applying for a personal loan or any loan in particular, it is important that one’s financial situation is taken into serious consideration. Only borrow what you are confident you can repay.

Welcome to the epitome of seamless collaborations! Our Professional Agreement sample guide is your compass in the intricate world of business contract dealings. Crafted for clarity and precision, this…

continue reading

Welcome to the pinnacle of property transaction efficiency! Our Property Sample Agreement document is your key to navigating the intricacies of real estate with ease. Tailored for the United…

continue reading