44+ Sample Cost Analysis

-

Price Cost Analysis Template

download now -

Framework for Initial Cost Analysis

download now -

Sample Cost Analysis Template

download now -

Financial Befit Cost Analysis Template

download now -

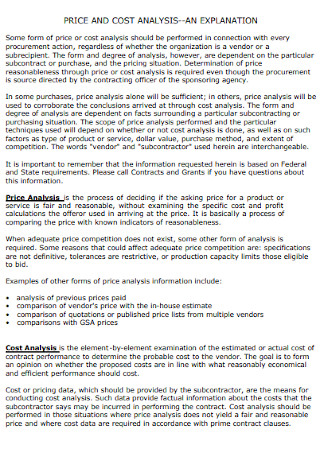

Sample Price Cost Analysis

download now -

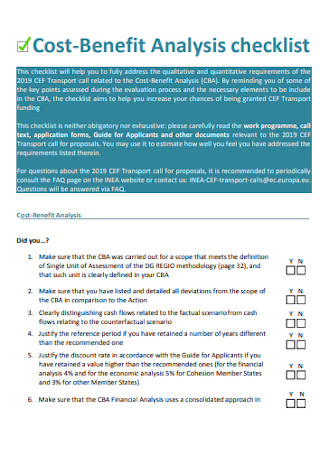

Cost-Benefit Analysis Checklist

download now -

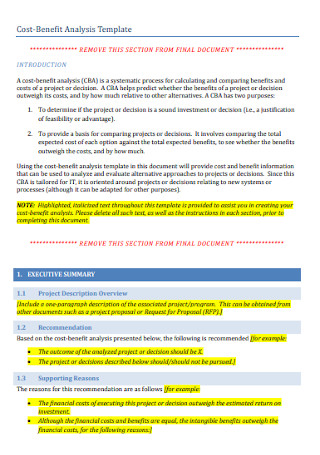

Cost-Benefit Analysis Template

download now -

Functional Cost Analysis

download now -

Distribution Cost Analysis

download now -

Cost-Benefit Analysis Questionnaire Template

download now -

Meal Cost Analysis Template

download now -

Life Cycle Cost Analysis

download now -

Canadian Cost-Benefit Analysis

download now -

Sample Cost-Benefit Analysis Template

download now -

Sample Project Cost Benefit Analysis Template

download now -

Nonprofit Cost Analysis

download now -

Bridge Life-Cycle Cost Analysis

download now -

Quality Cost Analysis

download now -

Market Cost Analysis Template

download now -

Comparative Benefit-Cost Analysis

download now -

Supplement Benefit-Cost Analysis

download now -

Basic Cost Benefit Analysis Template

download now -

Cost-Benefit Analysis of Research Template

download now -

Comparative Cost Analysis Template

download now -

Library Cost Analysis

download now -

Army Cost Analysis Template

download now -

Incident Cost Analysis

download now -

Water Cost Analysis Template

download now -

Theory of Cost Analysis Template

download now -

Cost-Analysis and Regulatory Reform

download now -

Cost Analysis for Community Based Climate Template

download now -

Transaction Cost Analysis Template

download now -

Cost-Benefit Analysis and Regulatory Reform

download now -

Manufacturing Cost Analysis

download now -

Simple Life Cycle Cost Analysis

download now -

Transportation Cost and Benefit Analysis

download now -

Cost and Profit Analysis Form

download now -

Paper Cost Analysis Template

download now -

Education Cost Analysis Template

download now -

Project Cost-Benefit Analysis

download now -

Cost-Benefit Analysis Report Template

download now -

Checklist for Cost Analysis Template

download now -

Machine Cost Analysis Template

download now -

Production and Cost Analysis

download now -

Non-Marginal Cost Analysis Template

download now

FREE Cost Analysis s to Download

44+ Sample Cost Analysis

What is Cost Analysis?

Purpose of a Cost Analysis

How to Create a Cost Analysis Document?

Different Methods in Cost Analysis

The Cost-Effectiveness of Using Resources

FAQs

Why is a cost analysis relevant?

What are the most challenging steps in the cost analysis process?

What are the deliverables from a cost analysis?

What can be done with the true-cost information?

What is Cost Analysis?

Not to be confused with cost-benefit analysis where the cost of running the program or executing a project is compared to its benefits, a cost analysis breaks down a cost summary into different categories and constituents. It is the process of allocating estimated project costs and comparing them to other programs or opportunities. In general, a cost analysis will determine the effectiveness and profitability of a venture by tallying up the cost of the project or the decision and comparing it with the actual cost or for a given period with another project cost.

Conducting a cost analysis, as the name implies, focuses on the costs or expenditures that will be incurred when a business plan or a project proposal is implemented without any regard to the ultimate expected outcomes. It’s a crucial step to undertake before fully engaging in other types of economic evaluation of the sustainability and feasibility of a potential project.

In other words, cost analysis is concerned about determining the monetary value of the business or organizational operations such as supplies and materials, labor, logistics, tasks, activities, and other inputs that are associated with the project or the program.

Purpose of a Cost Analysis

Cost-benefit analysis examples will show you that the projected costs and their corresponding benefits will determine whether or not the decision to implement and execute the plan is worth it and makes sense from a business perspective. However, in cost analysis, the cost-benefit of a plan or a project is not measured. In cost analysis, you will be able to:

In a cost-benefit analysis, business plans—marketing, expansion, diversification, and all other else in between are deemed worth the efforts and resources if the projected benefits outweigh the costs and spending. If this is the case, one could argue that the decision made was a good one. If, on the other hand, the cost of executing the plan is more than the benefits, the project or the plan should be put on hold and the company may want to take some time to rethink the decision.

Unlike the cost-benefit analysis, conducting a cost analysis will not address the outcomes and the benefits for the business or the organization, but focuses on the costs, spending, and expenditures of a project or a program.

How to Create a Cost Analysis Document?

Performing a cost analysis is critical to any project may it be in the proposal or re-evaluation stage. A comparative assessment of all the anticipated benefits from the project and all the costs that will be incurred to launch the project, execute, and adjustments resulting from it. To perform a cost analysis, follow these five simple steps:

Step 1: Determine Purpose and Scope of Analysis

Spending some time thinking about all the questions that you need to answer before conducting a cost analysis is necessary. Knowing and understanding the purpose of the analysis can help you tailor the next steps of your analysis to what you really need to see. Generally, the purpose of cost analysis is to know the true cost of a project venture under analysis. By knowing the true cost of each program that’s part of the project will allow you to determine the revenue you will get from implementing the project and ensure that it will not cause the organization to bleed out its finances.

It is helpful to define the activities or programs under analysis and delineate one from the other. This step should not be skipped as delineating each item, task, activity, and program will enable you to allocate and distribute costs in different categories properly. For items that look similar, they should be carefully considered and grouped cohesively.

Step 2: Gather Important and Relevant Information

Having complete and accurate financial information is required for a comprehensive cost analysis. You should gather all relevant data accordingly. Some information you need to gather are as follows:

- All organizational costs—program costs (direct costs) and overhead expenses (indirect costs)

- Anticipated expenses during program implementation or project duration

- Number of people involved in the project in either full-time or part-time capacity and summary of job responsibilities of each person along with their payroll information

- Estimated working hours of each team member per program or project

- Estimated usage of infrastructure such as facilities, equipment, information technology licenses, etc.

Step 3: Allocate Monetary Value to Direct Costs

Direct costs refer to each items’ labor costs and other attributable expenses to the project or program. This part of the cost analysis should be straightforward especially for an organization that keeps a record of its finances in distinct categories. The key here is to take the existing cost information and sort each item according to their cost categories and program areas as defined in Step 2.

Other cost analysis templates may re-organize and re-categorize these items, but the principle behind it remains the same: distribute costs according to the areas or line items that you specified for the cost analysis.

Some examples of direct costs include salaries and benefits of people involved in the project, travel expenses, and personal equipment costs, procurement of supplies and materials, logistics like rent and venue, as well as contract fees of other partners.

Step 4: Allocate Monetary Value to Indirect Costs

Indirect costs are usually shared costs across the organization and not just about the program or the new plan. These include expenditures that are not directly associated with the business plan or specific activity of a current project under analysis. As these costs are not tied with the new project, these costs have not been distributed yet in the previous step.

This type of cost usually includes general administration and management expenses like staff salary and benefits, infrastructure costs, and other costs that are not directly tied with the project but all programs or projects within the organization will be able to benefit. Marketing costs and advocacy expenses are some examples of indirect costs.

Step 5: Check Your Cost Allocation

Once you have all your program and financial information gathered, check to see if it makes sense to you. Make sure to double-check your numbers and figures to see that you did not miss anything and your data is error-free. These simple checks will help you ensure that all data are allocated properly and everything makes intuitive sense:

- Check to see that all cost has been allocated properly and accordingly

- Review descriptions/rosters against your cost allocation

- Verify your cost-utility results

Different Methods in Cost Analysis

The main purpose of cost analysis is to understand the organization’s finances. There are many ways to conduct a cost analysis, but two of the most substantially different approaches to analyzing the cost data are “top-down” and “bottom-up”. To some extent, using both in one cost analysis can be helpful to identify errors or find any omissions in the life cycle cost of the program management.

Top-Down Method

With a top-down analysis method, you get to do a detailed study of the cost reports. This approach can be easily started immediately by using copies of the organization’s budgets such as operational costs, capital, funding for the current year, last year, and the proposed budgets for the next year, etc.

Details on every expense should be displayed and the internal documents should be compared to the public financial statements and public reports and the most recent reports of the auditor. Generally, these documents should show a breakdown of the revenues and expenditures. In most cases, the most obvious places to look for savings are on large programs and large expense items on the list. With the top-down approach, you look for exceptions—explaining the changes in costs or revenues and look for ways to fill in the gaps or the deficits.

Bottom-up Method

To understand the activities of concern in detail, the bottom-up analysis method may be used by interviewing relevant people involved in the program. It is generally useful to this approach by observing operations, managers, and staff descriptions of activities to determine their desires and not just the actual practice.

The incremental cost method particularly fits the bottom-up analysis where you strive to understand the factors that drive external events and internal decisions which could incur major costs. The total cost for each event or decision made is assessed and compared with a baseline cost that was set beforehand.

The Cost-Effectiveness of Using Resources

It may seem logical to view project costs as a straightforward process and find ways to reduce costs. While it is maybe true to some extent, it is generally helpful to assess the problem and see it in a different light to effectively manage costs as its reduction alone may not be the best approach to achieve financial and organizational health. A budget is only effective if the savings actually exceed the value of the costs or the income lost. Remember, the cost-effective use of resources is the main objective of the cost analysis.

Cost-effectiveness analysis is not only helpful for any business venture, but also in the healthcare industry facing limited resources. It helps them understand how every penny is spent or not spent will contribute to more services delivered, added value created, and the earned or contributed income so they may be able to determine the optimal interventions that they should provide.

FAQs

Why is a cost analysis relevant?

An effective true-cost analysis gives you a clearer picture of the financial status and demands of every program and project that was proposed to your organization. It offers relevant information so a smart and strategic decision can be made and prioritize and fundraise.

What are the most challenging steps in the cost analysis process?

Perhaps the most challenging part in creating a cost analysis are the sections that require the most thought and generate more insights. It would be helpful to pay particular attention to categories and items that drive costs. Asking for help and assistance from more knowledgeable staff members can guide you about certain cost drivers.

What are the deliverables from a cost analysis?

The typical deliverables from a cost analysis are: • Tables that show the total cost of the program, project, or service changes under various assumptions • Calculations of the potential added or eliminated short-term and long-term incremental costs to or from a program, project, and service • Compilation of unit costs for every line item in every category

What can be done with the true-cost information?

Completing a cost analysis will show the true cost of executing a project or implementing a program. This information can be immediately used in making key decisions that are related to the costs and effectiveness of a project or a program that will prioritize a cost-effective way of savings and cost reduction.

In a cost analysis, a cost is calculated by gathering all financial records and collating information relevant to the project or program under analysis. This will help organizations and teams to determine the true cost of a program or a project and aid them in their decisions to pursue or shelf it. It may also be possible to determine the value of a project before it’s implemented. The cost analysis can also help identify the benefits of a potential project and determine its feasibility.