-

Business Non-Compete Agreement

download now -

General Insurance Non-Compete Agreements

download now -

Insurance Non-Compete Agreement Form

download now -

Insurance Non-Disclosure And Non-Compete Agreement

download now -

Standard Insurance Non-Compete Agreement

download now -

Insurance Non-Competition Agreement Form

download now -

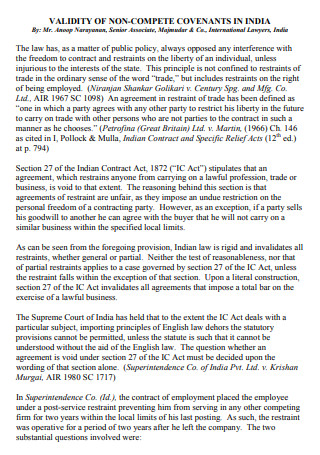

Insurance Validity of Non-Compete Agreement

download now -

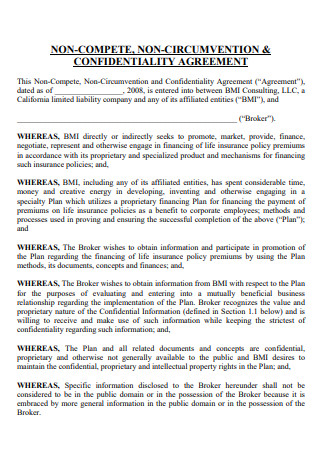

Insurance Non-Compete & Confidential Agreement

download now -

Aviation Insurance Non-Compete Agreement

download now -

Insurance Non-Compete Agreement Example

download now -

Health Insurance Non-Compete Agreement

download now -

Property Insurance Non-Compete Agreement

download now

What Is an Insurance Non-compete Agreement?

A contract is an essential document outlining how a company will establish its objectives and what procedures will be taken to attain them. The agreement should include this information. A business plan provides a general path of action for an entire organization, as viewed by its many sections in the marketing, finance, and operations departments. Business plans are frequently utilized to attract investment even before a company has developed a stellar track record. For instance, a business plan may be used to attract potential business partners for a joint venture. Even though these are most useful for new enterprises and corporations, every business should be able to construct a well-written business plan. This should make it possible for them to periodically examine and update the situation to determine whether or not the set objectives have been met and how their working conditions have changed. A solid business plan should include not just the anticipated and estimated expenditures of the joint venture but also the potential problems that could result from any decisions made by the management team. Even among competitive enterprises operating in the same market, it is scarce for two businesses to have identical business strategies. Even when collaborating in a joint venture, organizations often adhere to their tried-and-true business practices and approaches to their respective industries. 75% of U.S. businesses are underinsured, and 40% of small business owners have no insurance. In the event of a natural tragedy or legal action, many small firms are uninsured.

Benefits of Business Insurance

You have invested in your company. You’ve invested time and effort into launching the project and opening the doors. Protecting your investment is essential in ensuring your business’s success. Business insurance protects small business owners against property damage and liability claims. The operation of a firm entails both anticipated and unforeseen risks. There are various types of insurance that might be beneficial to businesses. Each sort of business insurance protects you and your firm in a unique manner. Insurance is essential, whether it’s property damage, providing your staff with benefits if they become ill or injured on the job, or covering the expenditures to assist your organization in recovering from a data breach. Most firms begin with coverages for general liability, commercial property, business income, commercial vehicles, workers’ compensation, and professional liability. Among the advantages of obtaining company insurance are the following:

Types of Business Insurance

Business owners require insurance coverage. Most states mandate that business owners carry at least general liability insurance. However, you must do more than stroll into an insurance firm and request business insurance. This is because there are about as many forms of business insurance as there are business types, and one size only fits some. What kind of business insurance is appropriate for your company? There are seven principal forms of commercial insurance:

1. General liability insurance

General liability insurance protects you from claims relating to business activities. This insurance will cover the cost of your defense and any damages awarded if someone is hurt on your business’s property or if you damage someone else’s property. Any company that interacts directly with clients must carry general liability insurance. For instance, suppose you own a retail store. A customer fell in your lobby and fractured their arm. They file a lawsuit against you for bodily harm, and the court gives them $100,000 in damages. Your insurer will pay for your injuries and court fees if you have general liability insurance. The majority of plans also cover your business from libel and slander claims.

2. Workers’ compensation insurance

Workers’ compensation insurance, also called “workers’ comp,” pays for medical bills and lost wages if an employee gets hurt. If the employee sues you, it will sometimes pay for your defense in court. Workers’ comp can come with disability insurance sometimes. Say, for instance, that you have a small clothing line; if one of your employees gets hurt, your workers’ compensation insurance will pay for sewing, their medical care, and lost wages. Workers’ compensation insurance is a must for any business with employees.

3. Commercial property insurance

This business insurance protects your business’s assets from damage or theft. If a fire destroys your office or someone steals your computer equipment, this insurance will cover the cost of repairs or replacements and lost income. Commercial property insurance is a must for any business with physical assets. Say, for instance, you own an accounting firm, and your office is broken into. The thieves rob your computer, printer, and furniture. If you have retail property insurance, your insurer will cover the cost of repairs or replacement and the income you lost while your team couldn’t work because of the missing equipment.

4. Professional liability insurance

This type of insurance, also called “errors and omissions,” insurance protects businesses from the cost of damages or injuries that happen because of the company’s professional services. If you work for clients and they say you didn’t do it right and that your mistake cost them money, this insurance will pay for your defense, and any damages are given. For instance, let’s say you’re a builder. You designed a house for a client, and they say that because your design was wrong, the roof leaked during the first storm. If they file a lawsuit against you, your professional liability insurance will pay for your legal fees and any damages they give you.

5. Commercial auto insurance

When you drive a vehicle for business purposes, commercial auto insurance safeguards your company against the cost of any damages or injuries that may occur. This insurance will cover the cost of car repairs or replacement, medical expenses, and lost earnings if you or one of your employees is involved in an accident. Every company with automobiles must have commercial auto insurance. Suppose, for instance, you own a food truck and are interested in an accident. Your commercial auto insurance will cover the cost of truck repairs or replacement, medical expenses, and lost income.

6. Product liability insurance

Product liability insurance protects you against claims arising from the sale of items. This insurance will cover the expense of your defense and any damages awarded if a customer alleges that your goods caused them bodily harm or property damage. Suppose you sell a cleaning product that causes hospitalization due to a severe allergic response. Your product liability insurance will protect your legal fees and any damages awarded if a customer sues you.

7. Business owner’s policy

A business owner’s policy (BOP) is a type of business insurance that combines many coverage types. General liability, property damage, business interruption, and workers’ compensation are the most frequent types of coverage included in a BOP. Consider that your small business is an ice cream parlor. Your business has been broken into, and your cash register has been taken. You must close for two weeks so that repairs can be completed. Your insurer will compensate you for missed revenue and office equipment repairs or replacement if you have a business owner’s coverage.

How Can You Form a Joint Venture

A joint venture is a contract between two or better businesses to work on a project or start something new. The business goal is usually short-term, and this joint business plan can be made with an agreement. Both sides will say in the deal that they are on the same side. In this business agreement, the resources will be combined to help the business reach its goal. A joint venture can involve any legal structure. When entrepreneurs want to get into a foreign market, they often join forces with a local business in this way. It’s easy to make a business plan with someone else. There are some steps you must take.

1. Choose the Right Partner

If you wish to be successful on this journey, ensure that your firm is in capable hands. Each side must be on the same page and pursue the same objectives. Understanding the gaps in your business plays a crucial role here as well. A clearly stated company purpose will aid in finding a suitable fit. Then, you will select a company that aligns with your business objective. More than choosing a reputable company is required. You must ensure that you get along with your new “partner.” Spend time together to determine if you are compatible. It is crucial to decide whether or not they care as much about this collaboration as you do. Check whether you can trust these individuals. Nobody wants to entrust their business to an untrustworthy individual.

2. Pick a Type of Joint Venture You Want

There are two ways to make a business plan together. One way is to make your joint venture business a new, separate business. Each person or group owns a part of the new legal entity. For example, you could start a corporation, a limited liability company, or a partnership. Then you would do business through this new group. The second choice is to work together under a contract. With this choice, the terms of the business relationship are set in a contract. This choice is less expensive. Before choosing between these two, you should consider what your business needs and how much money you want to spend to get it started.

3. Prepare Your Joint Venture Agreement

Regardless of the type chosen, a written agreement is required. In the end, it makes sense to establish a business contract. Start with a term sheet or an intent letter. This will assist you in revealing the subsequent steps. A term sheet should contain pertinent terms and conditions. Likewise, a letter of intent summarizes the significant words and requirements. Your joint venture agreement may be lengthy and straightforward or vice versa. This depends on the nature of the business and the parties involved. Consider how you will divide the gains and losses. Include the number of each party’s resources.

4. Decide If Your Business Requires a Joint Venture

As stated above, it is only sometimes beneficial to combine resources. It can be detrimental to your business as well as helpful. Therefore, you must think carefully before beginning the process. Still, trying to figure out how to choose?

FAQs

Is non-compete a good thing?

A non-compete clause might prohibit the seller of a firm from launching a competitive enterprise within a specific distance or time limit after the transaction. This ensures that the original owner will not rivalry unfairly with the newly acquired business.

What is too long of a non-compete?

In contrast, in many businesses, a non-compete agreement with six months will be deemed reasonable and enforceable. The general rule is that the duration of the contract should be, at most, what is reasonably required to defend the employer’s legitimate business interests.

Does getting fired void a non-compete?

In most circumstances, the non-compete agreement remains in effect even if the employee is terminated or laid off. You may be able to ask your former employer to waive the condition. In such situations, employers are occasionally more willing to waive the requirement.

One thing to remember is that business plans are not intended to be static documents. They should remain “alive” because they are adaptable and receptive to change. Reacting to the business plan as necessary and adjusting to the evolving environment in which the joint venture is striving to operate is crucial to its success. It should expand and develop in parallel with your enterprise.