40+ Hardship Letters

-

Letter of Hardship

download now -

Sample Hardship Letters

download now -

Hardship Letter

download now -

Cost Recovery Letter

download now -

Hardship Letter of Example

download now -

Utility Hardship Letter

download now -

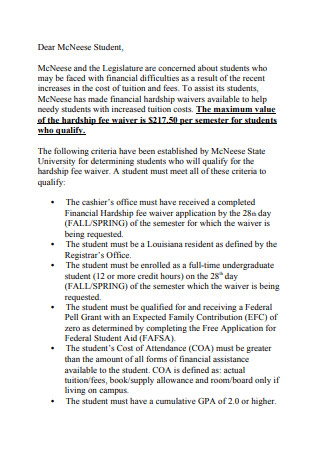

Financial Hardship Waiver Letter

download now -

Hardship Waiver Request

download now -

Official Request for Hardship Waiver

download now -

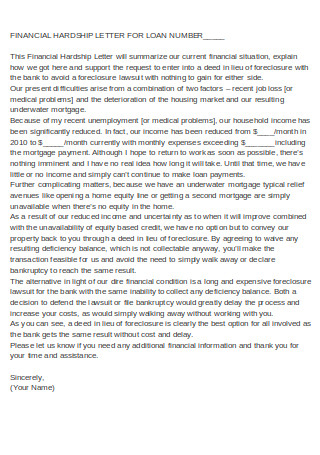

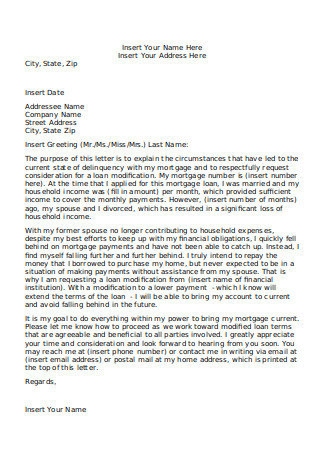

Financial Hardship Letter for Loan

download now -

Editable Hardship Letter

download now -

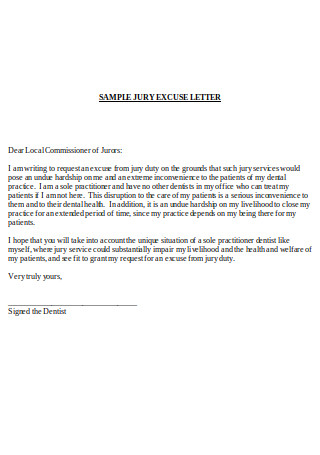

Sample Jury Excuse Letter

download now -

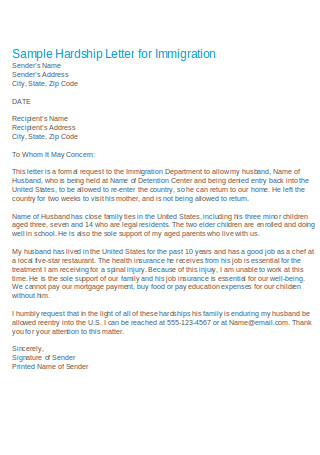

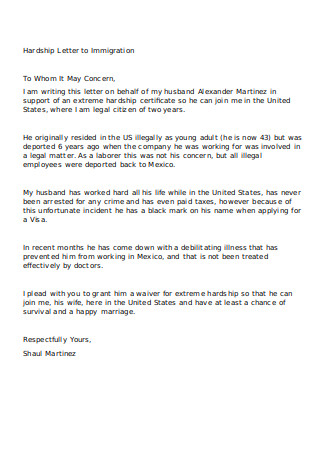

Sample Hardship Letter for Immigration

download now -

Hardship Letter to Immigration

download now -

Printable Hardship Letter

download now -

Basic Hardship Letter

download now -

Formal Hardship Letter

download now -

Standard Hardship Letter

download now -

Sample Hardship Letter Format

download now -

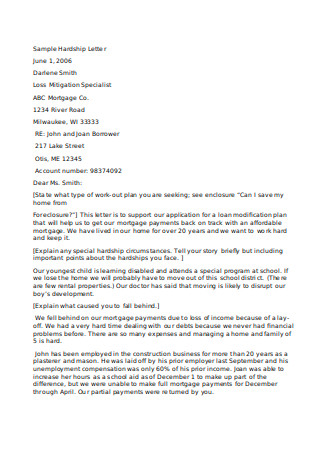

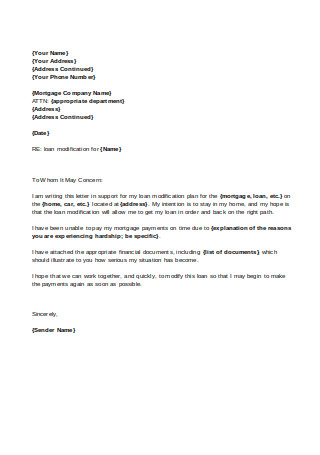

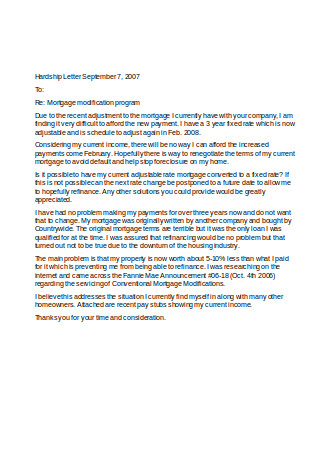

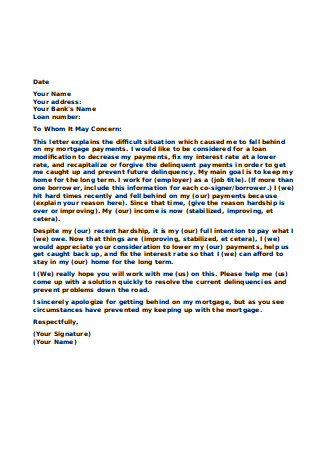

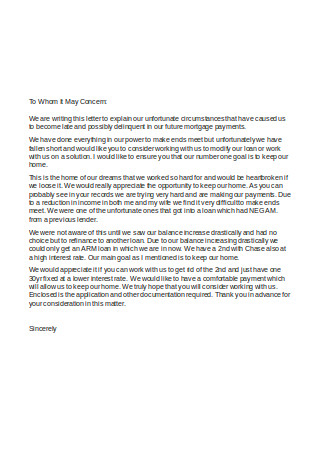

Hardship Letter for Mortgage Finance

download now -

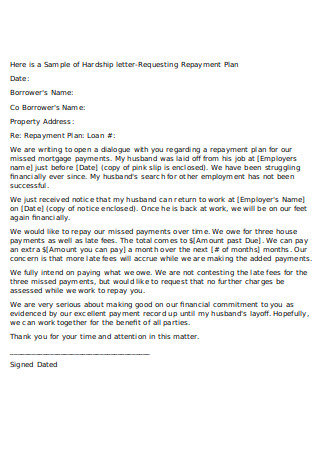

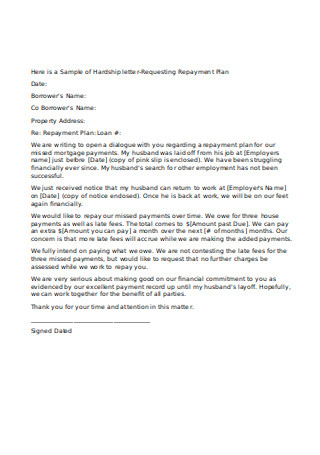

Hardship Letter-Requesting Repayment Plan

download now -

Hardship Letter for Creditors

download now -

Hardship For Loan Number

download now -

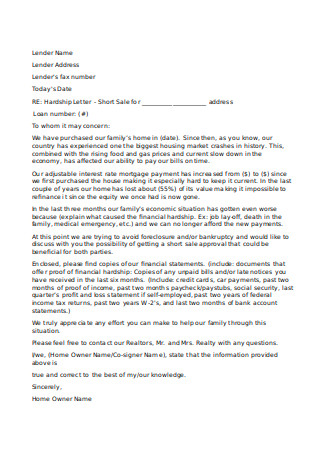

Hardship Letter for Short Sales

download now -

Format of Hardship Letter

download now -

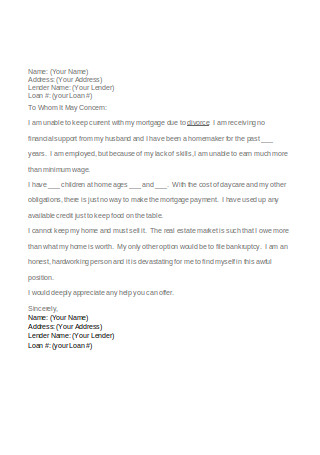

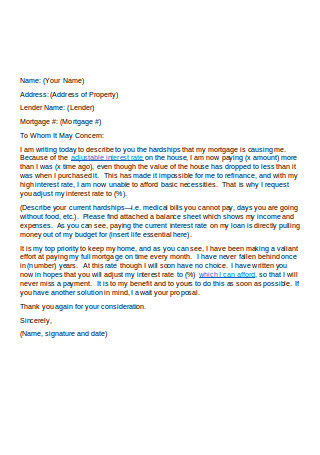

Financial Hardship Letter for Mortgage

download now -

Editable Financial Hardship Letter

download now -

Financial Hardship Letter

download now -

Consolidation Hardship Letter

download now -

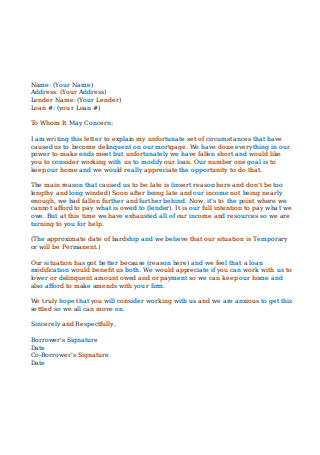

Hardship Letter on Mortgage

download now -

Basic Hardship Letter

download now -

Hardship Letter for Loan Number

download now -

Formal Financial Hardship Letter

download now -

Basic Financial Hardship Letter

download now -

Printable Financial Hardship Letter

download now -

Hardship Letter in Word

download now -

Fillable Hardship Letter

download now -

Hardship Letter to Creditors

download now -

Business Hardship Letter

download now -

Application for Medicare Co-Insurance

download now -

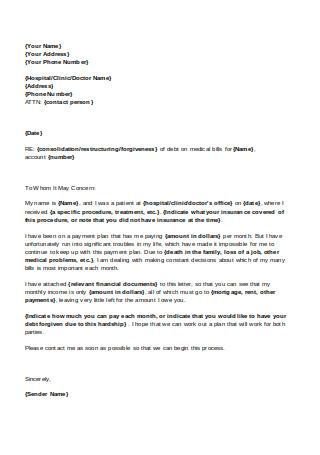

Patient Hardship Letter

download now -

Hardship Waiver Letter

download now -

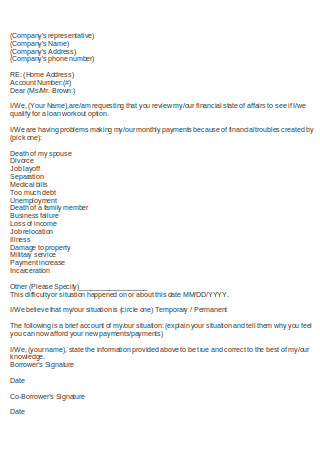

Financial Hardship Application

download now -

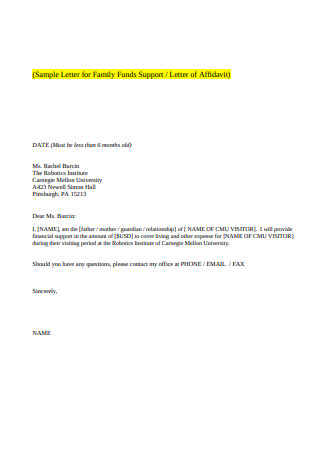

Sample Letter for Funds Support

download now -

Sample Hardship Letter in PDF

download now -

Sample Financial Request Letter

download now

What is a Hardship Letter and When Can You Use It?

A hardship letter is a letter explaining your current financial situation–why you can’t commit to the payment schedule that you have initially agreed upon with the financial institution. It’s different from a promissory note in the sense that you are requesting for a loan modification or adjustments in your current payment plan. Many factors constitute a hardship, although the bank or lender can only accept a few reasons. Since it talks of your financial situation, you can use it for areas that require debt payment. Here are a few instances where you can use a hardship letter to negotiate your current payment plan:

Whenever it comes to financial hardship, whatever debt you are in, you can always try to negotiate with your bank. They, too, will find a way to help you make your payments as much as possible.

What Qualifies as a Hardship?

“Hardship” is a broad terminology. It can describe just about any aspect of life. Every day we experience difficulties as we go about our daily routine, whether it’s trying to fight your way through the subway train or trying to beat a deadline at work. However, there are only a few instances or examples that your financial institution may consider as “hardship.” Here are a few examples of what can qualify as a hardship:

Although a hardship letter is useful for situations where you find it hard to make a payment due to your financial crisis, it’s not something you can qualify for all the time for any given situation. That’s why financial institutions need to take a look at your situation first before making a decision.

Are There Other Options Available For Me?

Renegotiating the terms of your payment through a hardship letter is an excellent way to make ends meet. But, did you know that there are other ways for you to pay your debt other than writing your bank? If you have a retirement account or a 401(k) account, you can try to make a “hardship withdrawal” to cover some of your expenses. If you are already over 59 and a half years old, you can already make a hardship withdrawal at any time. However, for people below 59 and a half years old, you have to be in extreme hardship first before they approve your request for a hardship withdrawal. And once approved, you will be subject to a 10% penalty tax for early withdrawal. Investopedia lists a few criteria set by the IRS for you to be eligible for a hardship withdrawal such as burial or medical expenses. Once qualified, your employer or financial advisor would require certain documents from you for submission. Refer to this link for further information regarding eligibility on hardship withdrawal.

How To Write a Good Hardship Letter

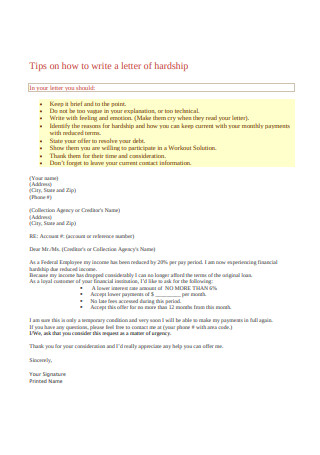

Mastering the art of persuasion takes a lot of practice. You have to know the workings of the human brain to make a convincing argument. And with creditors and banks having dealt with too many people to last them a lifetime, it would be hard to turn their decision around. Fortunately, we can change their minds by explaining our situation using a hardship letter. You can download our available templates and sample to save you from the hassle of writing a letter. You can also opt for doing it yourself using our step-by-step guide on how to write a hardship letter. So how do you write a convincing hardship letter that would make hearts bleed while remaining professional?

Step 1. State Your Reason

State in your letter why you could not make your payments like how you used to, or why you are delinquent. If it’s because of a medical condition, tell them straight out the “when” and “what then” of your situation. For example, you could say to them that you recently received a dismissal letter and could not make any payments for the time being. Don’t try to make it longer than necessary. That, in itself, is already enough for reasons we will state later.

Step 2. State Your Request

Specify what kind of help you are needing. Most of the time, people write to request for a loan modification. That means they need help in modifying the dollar amount of their payments initially written in their loan agreement. If, though, you could not make your payment at all, then state that you are requesting for help on putting your payments to a halt until you find a source of income.

Step 3. State Your Plan

No lender or creditor will agree to a loan modification request if you don’t have a plan on how or when you can make your payments again. Don’t make a promise like “making my payments again once I win the lottery.” Make your plan concrete, realistic, and doable. Something like “getting a second job” or “applying for a personal loan” would suffice. It would be great, too, if you can state a timeframe on when you can put your plan in motion.

Step 4. Keep It Short

Don’t make it wordy. A human’s attention span can only last for a few seconds. If your letter is worth two pages, your creditor would not want to read that, especially if he knows it’s a hardship letter. Try to keep it all on one page, and don’t drag your explanation.

Step 5. Attach All Supporting Documents

It’s easy to explain your situation in writing, but your financial institution would require concrete proof of the hardship that you are experiencing. With that, attach all the documents you have–medical bills, medical certificates, receipts, final payslip, certificate of employment–that will support your claim regarding your situation.

As long as your situation is genuine, your financial institution will find a way to help you settle your payments. At the end of every good letter (approval letter or consent letter), never forget to thank them for the help that they will be giving you. Whatever hardship you are experiencing, never give up. As the saying goes, “A river cut through a rock not because of its power but because of its persistence.”