23+ Sample Financial Budget Plan

-

Financial Budget Planning Template

download now -

Financial Road Map Budget Plan

download now -

Multi Year Financial Budget Plan

download now -

Financial Budget Plan Report

download now -

Financial Budget Planning Example

download now -

Financial Budget Plan in PDF

download now -

Financial Annual Program Budget Planning

download now -

Financial Budget Allocation Plan

download now -

Financial Education Budget Planning

download now -

Office Financial Budget Planning

download now -

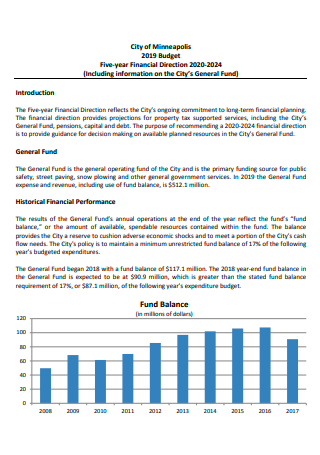

Five-Year Financial Direction Budget Plan

download now -

Basic Financial Budget Plan

download now -

Financial Budget and Master Plan

download now -

Financial Final Proposed Budget Plan

download now -

Financial Annual Budget Plan

download now -

Financial Budget Planning Policy

download now -

Financial Budget Strategic Plan

download now -

Financial Future Budget Planning

download now -

Financial District Action Plan and Budget

download now -

Financial Budgeting Planning in PDF

download now -

Simple Financial Budget Plan

download now -

Financial Budget Planning in DOC

download now -

10 Year Financial Budget Plan

download now -

Financial Manage Budget Plan

download now

FREE Financial Budget Plan s to Download

23+ Sample Financial Budget Plan

What Is Financial Budget Plan?

What Is the Purpose of a Financial Budget Plan?

What Are the Types of Budgets?

Levels of Involvement in Budgeting Process:

Steps on How to Create a Financial Budget Plan:

FAQs

What are the challenges in budgeting?

What are the factors to consider when developing a budget?

What are the advantages of financial planning in business?

What Is Financial Budget Plan?

A financial budget plan means predicting the income and expenses of the individual on a long-term and short-term basis. Exact projections of cash flow help the business achieve its targets in the right way.

Financial budget planning comprises a detailed budget, the sources of incomes and expenses of the business, etc. The evaluation of incomes and expenses is done on a monthly, quarterly, half-yearly or annual basis, depending on the suitability of the organization or individual. Moreover, a financial budget is a prevailing tool to achieve the long-term goals of anyone. Most importantly, it also keeps the shareholders and other members of the organization updated about the functioning of the business.

What Is the Purpose of a Financial Budget Plan?

The purpose of the financial budget is to guesstimate the firm’s cash budget, capital expenditures, and balance sheet line items like assets, liabilities, and owner’s investment. The financial budget is the last budget to be developed by the firm every year since all other budgets—like the individual budgets in the operating budget—are necessary first. The financial budget helps the firm by allowing it to calculate net profit when the budget process is done.

What Are the Types of Budgets?

There are four types of budgets that companies use:

Levels of Involvement in Budgeting Process:

You want buy-in and acceptance from the entire organization in the budgeting process, but you also want a well-defined budget and one that is not manipulated by people. There is always a trade-off between goal equivalence and involvement. The three themes outlined below need to be taken into consideration with all types of budgets:

Imposed budgeting. This is a top-down process where executives follow a goal that they set for the company. Managers follow the goals and impose budget targets for activities and costs. It can be effective if a company is in a turnaround situation where they need to meet some difficult goals, but there might be very little goal congruence.

Negotiated budgeting. This is a combination of both top-down and bottom-up budgeting methods. Executives may rough draft some of the targets they would like to hit, but also, there is shared responsibility for budget preparation between managers and employees. This amplified involvement in the budgeting process by lower-level employees may make it easier to adhere to budget targets, as the employees feel like they have a more personal interest in the success of the budget plan.

Participative budgeting. Participative budgeting is a roll-up approach where employees work from the bottom up to recommend targets to the executives. The executives may provide some input, but they more or less take the recommendations as given by department managers and other employees. Operations are treated as autonomous subsidiaries and are given a lot of freedom to set up the budget.

Steps on How to Create a Financial Budget Plan:

You probably need some way of determining where your money is going each month even if you don’t use a budget spreadsheet. Creating a budget with a template can help you feel more in control of your finances and let you save money for your goals. The style is to figure out a way to track your finances that works for you. These following steps can help you create a budget:

Step 1: Note your net income

Identify the amount of money you have coming in. It is easy to overestimate what you can afford if you think of your total salary as what you have to spend. Remember to exclude your deductions for Social Security, taxes, and flexible spending account allocations when creating a budget worksheet. Your final take-home pay is called net income, and that is the number you should use when creating a budget.

Step 2: Track your spending

It is helpful to keep track of and categorize your spending so you know where to make adjustments. Doing so will help you identify what you are spending the most money on and where it might be easiest to cut back.

Step 3: Set your goals

Make a list of all the financial goals you want to accomplish in the short-and long-term before you start sifting through the information you’ve tracked. Short-term goals should take no longer than a year to achieve. Long-term goals, such as saving for retirement or your child’s education, may take years to reach. Remember, your goals don’t have to be set in stone, but knowing your priorities before you start planning a budget will help.

Step 4: Make a plan

Use the variable and fixed expenses you compiled to help you get a sense of what you’ll spend in the coming months. You can predict accurately how much you’ll have to budget for with your fixed expenses. Use your past spending habits as a guide when trying to predict your variable expenses.

Step 5: Adjust your habits if necessary

After doing all these, you have what you need to complete your budget. Having documented your income and spending, you can start to see where you have money left over or where you can cut back so that you have money to put toward your goals.

Step 6: Keep checking in

It is important that you assess your budget on a regular basis to be sure you are staying on track. Few elements of your budget are set in stone: You may get a raise; your expenses may increase or you may have reached your goal and want to plan for a new one. Remember to follow the steps you’ve read.

FAQs

What are the challenges in budgeting?

These are the common budget challenges and key steps you can take to tackle them:

- Being indecisive about finances. There is nothing worse than being indecisive about finances. Financial indecisiveness can stop you in your tracks and prevent you from accomplishing your financial goals. Just the thought of even making a budget may be overwhelming, but the most productive thing you can do is to just start.

- Not having financial goals. The key to overcoming the challenges of budgeting is having financial goals in place. It can cause you to lose focus on why you created a budget in the first place if you don’t have a clear goal in mind. Financial goals can motivate you to stick with your budget and become financially successful.

- Not using the right budgeting method. One of the reasons you are facing budget challenges may be because you are using the wrong budgeting method. There are many budgeting tools and templates to choose from, and the trick is to find the one that suits you best.

- Fear of facing debt. Ignorance is bliss, but it’s devastating to your finances because you don’t have a financial plan in place. The thought of sitting down and adding up just how much debt you have can be one of the most difficult budget challenges yet. However, the only way to regain control of your financial future is to create a debt payoff plan with your budget.

- Not budgeting for savings. Even if you are paying your bills on time, it doesn’t mean you are budgeting correctly. For instance, if you aren’t building savings into your budget then you aren’t preparing for your future. Moreover, one of the most important things to do when budgeting is to pay yourself first. The fastest way to save money is to build it into your budget. This way, you aren’t tempted to spend it, and it becomes a good money habit.

- Unexpected expenses. This is one of the hardest budget challenges to tackle. That is why it is vital that you build up your emergency savings account so you will be prepared for the unexpected. Things like car repairs, medical expenses, or losing your job can throw you off track.

What are the factors to consider when developing a budget?

Your Income Structure. The way in which money comes into your income statement is critical for planning cash flow.

Your Spending Habits. How money exits your income statement is equally critical to your cash flow.

Being Tech Savvy. The actual physical incarnation of your personal budget will also depend on the degree to which you are comfortable with technology.

Your Personality. This factor sort of intermingles with some of those mentioned above. You may be a hardwired spender or saver. You may embrace or shun technology. The key is to know yourself and play to your strengths. If the thought of figuring out how to use a computer gives you a rash, forget about it. Budget in a way that fits who you are.

What are the advantages of financial planning in business?

Correctly managed cash flow. Keeping a keen eye on cash and debt levels will help keep your business finances on an even keel, especially important for newly launched businesses.

Personal finances. It is essential to take a salary whatever the size of your business. Salary does not need to be high while using business capital in the early growth stages. Many small business owners will pay themselves enough to cover their National Insurance threshold so that their salary is tax-free. In the short term, this may prove to be an advantage, but a sound financial plan can help accumulate savings for life events in the future.

Achieving personal goals. Business owners should also allocate time to work out their personal goals in the same way that they put together long-term business plans. Knowing what is personally achievable is just as important in planning the finances for a business.

Clear retirement goals. Whether you decide to close down a business or sell it on, you’ll need to determine how much is required in order to fund personal finances post-employment. Keeping tabs on personal expenses will help to establish what is needed to be financially sound in the future.

A secure retirement income. Most business owners dream that the sale of their business will be enough to fund their retirement years, but in reality, this is often an unknown. A business finance plan will go a long way to putting the business in a position to help achieve this goal, but it’s essential to plan for a more modest outcome, too. Putting away retirement savings on a regular basis should be incorporated into financial plans.

Reduced risk. It is a common mistake for smaller businesses to reinvest their assets straight back into their own business, but doing this increases financial risk. Preferably, business owners should divide risk across different industries, and this will then reduce the chance and extent of losses. Furthermore, any investments should be adequately diversified and in keeping with the amount of risk your business can sustain. Find a well-managed investment policy that, so that focus can be on managing the business.

Insurance. In starting or running a business, it is vital to take out the right insurance to cover business and personal assets. You may need more than one insurance policy. If a key employee in a small company is suddenly unable to work, the business may become vulnerable. As a protection for your company, insurance against illness, disability, and death should be an essential part of financial planning.

Succession planning. Depending on the nature of the business, an alternative option may be to retain ownership and successional plan. If you’re planning on the company continuing to be part of the business once you’ve retired, a good exit strategy is required, ensuring leadership transition is smooth. With a wisely chosen successor, time can then be spent enjoying retirement while still retaining oversight, strategic input and a potentially significant income.

Your budget will be as exceptional as you are. As long as you keep it balanced and allow for enough savings to allow you to eventually become financially independent, you really don’t need to worry too much about exact details. A budget is simply a tool you need to achieve your shorter-term and longer-term goals and manage your cash flow.

Generally, overcoming the challenges of budgeting can help you stick with your budget and help you manage your money successfully. Remember that picking the right budgeting method is vital to your success. Don’t forget to make a list or a vision board of your financial goals to keep you driven.