23+ Sample Financial Action Plan

-

Financial Action Plan Template

download now -

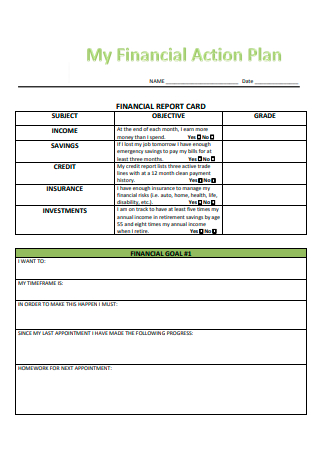

Basic Financial Action Plan

download now -

Financial Capability Action Plan

download now -

Financial Wellness Action Plan

download now -

Financial Action Plan Example

download now -

Financial Analysis Action Plan

download now -

Financial Education Action Plan

download now -

Financial Action Plan Worksheet

download now -

Future Financial Action Plan

download now -

Financial Management Action Plan

download now -

Financial Services Action Plan

download now -

Financial Assessment and Action Plan

download now -

Financial Action Plan in PDF

download now -

Formal Financial Action Plan

download now -

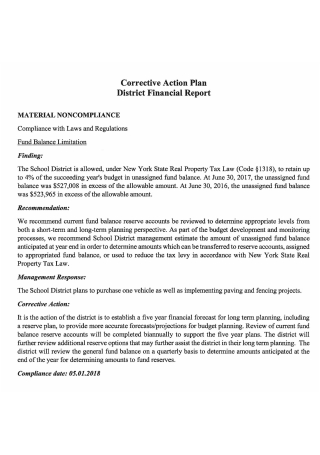

District Financial Corrective Action Plan

download now -

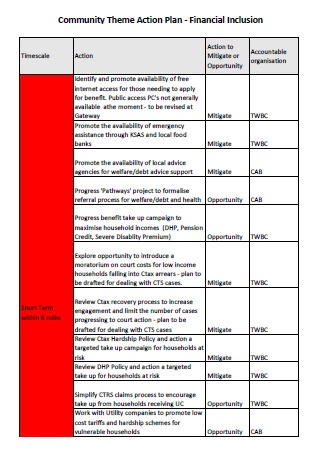

Financial Inclusion Community Theme Action Plan Template

download now -

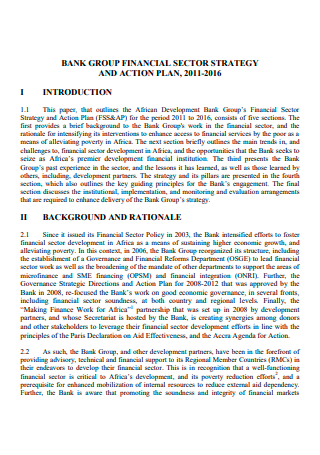

Financial Sector Strategy and Action Plan

download now -

Standard Financial Action Plan

download now -

Financial Goal Action Plan

download now -

Financial Market Transformation Action Plan Template

download now -

Financial Inclusion Action Plan

download now -

Simple Financial Action Plan

download now -

Financial Barriers Strategic Initiative Action Plan

download now -

National Financial Literacy Strategy Action Plan

download now

FREE Financial Action Plan s to Download

23+ Sample Financial Action Plan

a Financial Action Plan?

Benefits of a Financial Plan

Components of a Financial Action Plan

How To Create a Financial Action Plan

FAQs

What is your financial activity strategy?

What’s the difference between a business strategy and a financial feasibility study?

What is the primary assumption made in a financial plan?

What Is a Financial Action Plan?

A financial action plan is a document that details how you intend to manage your money to achieve your objectives. Simply knowing what you require will not get you there: you must have a concrete plan to accomplish it. And it should be documented, with specific goals and actionable steps that can be quantified. When a project is written with concrete, quantifiable measures, it is possible to determine whether or not it was successful. Additionally, the concrete, actionable steps eliminate hunches and guesswork from your planning. According to research, the majority of people are comfortable managing their money on their own. This may backfire. Despite statistics that many people live paycheck to paycheck and that less than half of all individuals could work an unexpected $1,000 bill, the majority of Americans reject financial assistance or advice. With this, 75% of Americans manage their money alone, without the aid of a professional or an internet service and only 17% of respondents indicated that they utilize a financial counselor.

Benefits of a Financial Plan

Have you considered your financial security? It’s natural to feel trapped, insecure, or overwhelmed. However, this is where a financial plan can assist. A financial plan identifies objectives, develops a feasible strategy for achieving them, and tracks progress toward success. Whatever stage of life you’re in — or whatever your financial plans may be — a financial plan can assist you in charting a path to success. Are you still undecided? The following are five advantages that financial plans can provide.

Components of a Financial Action Plan

Remember that the financial goals you create should state your objectives, how much money you’ll need to attain them, and when you’ll achieve them. They should also be achievable for you and measured in some way. Then, to ensure that you are making progress toward your objectives, develop a list of tasks to do. The following are five elements of a solid financial action plan:

Define the objectives of your financial plan.

The purpose of stating your objectives is to offer a focus for your plan. After all, you do not get into a car and begin driving blindly. Setting goals might be intimidating. Maintain a straightforward and understandable tone.

- Take some time to list down your thoughts.

- Once you’ve created a list, arrange your objectives chronologically.

- Following that, prioritize and focus on what is most important to you.

These objectives vary with time, so revisit your plan periodically to ensure it remains current with your life’s changes.

Create rudimentary cash flow estimates.

Cash flow estimates address the numerous “What if…” scenarios. For instance, suppose I retire at a given age. What happens if I spend this much money throughout my retirement years? Is my investment strategy compatible with my current expenditure requirements? Can I afford long-term care insurance if I require it? While no one can accurately determine the future, it is highly beneficial to “test” your strategy, assumptions, and capacity to survive unexpected events. Cash flow forecasts are used to evaluate these various scenarios. You will realize that the various components of your plan are interconnected during this process. For instance, your investment approach may be directly influenced by your income requirements or the number of years remaining till retirement.

Evaluate your risks.

Risks occur in a wide variety of shapes and sizes. For instance, how long will your money last? Without selling a kidney, how can you pay for education and save for retirement? How are you going to pay for long-term care? Specific hazards can be mitigated by the use of various types of insurance. As part of your strategy, others can be addressed through savings, investment methods, and basic planning approaches. While the tragedies we fear may not occur, it is critical to incorporate risk management into your plan. When people are experiencing significant positive or negative emotions, they are less able to judge likelihood appropriately. According to research, risk perception is strongly influenced by the unknowability, dread, and unequal distribution of risk among a community.

Develop an investment strategy based on the aforementioned considerations.

It is critical to have a financial investment strategy. It is, in many respects, the personification of your financial plan. A good investment strategy reflects the objectives you wish to accomplish. It is compatible with your Cash Flow Projection’s withdrawal requirements and time horizon. Finally, it strikes a balance between the risks you are willing to take as an investor and your required return.

Regularly review and adjust your plan.

Bear in mind that financial planning is an ongoing activity. It evolves as your life becomes. During periods of increased market volatility, it’s beneficial to remember that you’ve laid a solid foundation through planning. Maintain these time-tested principles. We enjoy guiding clients through the financial planning process.

How To Create a Financial Action Plan

Nobody worries more about your financial well-being than you do, which is why it’s critical to develop a financial strategy for yourself. A financial plan enables you to save money, purchase the items you truly desire and hold for long-term goals such as college and retirement. Financial preparation, in my opinion, is crucial, particularly for women, given the gender salary disparity. This should come as no astonishment, but everyone’s financial plan is unique. Therefore, whether you’re interested in learning how to develop a financial plan or why you should, you’ve come to the perfect place.

Step 1: Develop a personal financial plan for yourself.

If you’re single, it’s critical to develop a financial strategy that not only assists you in meeting your immediate smart goals but also guarantees your future self is cared for. This entails carrying out all of the preceding actions without making assumptions about how things will work out. A significant error is expecting to find someone to look after you and manage your relationship’s finances. If your relationship status changes or you marry, you’ll be well prepared to arrange your finances jointly if you’ve already taken care of your funds.

Step 2: Create a marriage finance plan.

If you are married, you must work unitedly on your finances. Discuss your household budget and financial goals with your partner and collaborate on financial decisions. While having joint accounts is beneficial, each individual should have their own personal savings account. As women, we must develop our sense of security and bring “our own” to the table. However, you are not required to keep your accounts private. Bear in mind that marriage and committed partnerships thrive on honesty and openness.

Step 3: Create a list of your financial objectives.

Setting financial objectives is critical to financial success. After all, it would be best if you first determined what you wish to accomplish to accomplish it. However, you want to ensure that your objectives are clearly defined and prioritized for goal setting. It’s terrific to have lofty ambitions! However, ensure that they are broken down into smaller parts. This way, you won’t feel overwhelmed while attempting to accomplish them, and you’ll be able to track your progress simply.

Step 4: Pay off your debts.

Make sure your financial plan includes a strategy for getting out of debt. Unfortunately, if you have a lot of debt, you won’t jumpstart your financial future. You’re better off paying your debts first because of the high interest rates, huge minimum monthly payments, and the damage that having a lot of debt may bring to your credit score. Create a debt-paying strategy and be patient but consistent in your efforts to get out of debt.

Step 5: Make a financial strategy for investing.

If you’re serious about accumulating wealth, you’ll have to put your cash to work for you. This is where financial investment comes into play. However, it’s critical to have well-defined objectives before investing any of your hard-earned money. Consider what the investment is for, when you’ll need the money, and how much risk you’re willing to take. If you genuinely want to see your money grow, investing is a long-term activity that you must commit to. Are you concerned that you’ll need your money soon? That’s why you have savings accounts in the first place: to put money aside for emergencies and short-term aspirations.

Step 6: Make tax preparations.

Taxes, of course! Taxes are inconvenient, but they aren’t going away any time soon. As a result, double-check that your long-term income predictions in corporate taxes. Taxes can have a significant influence on your cash flow if you don’t plan. Furthermore, you should look into tax-saving investment choices and stay current on any applicable tax deductions that can assist you in saving funds on tax payments. You can schedule an appointment with a tax accountant or financial adviser to ensure that your tax strategy is sound.

FAQs

What is your financial activity strategy?

A financial plan is a procedure that a firm lays out, usually in a step-by-step style, for utilizing its available capital and other asset lists to achieve its growth or profit objectives based on a plausible financial forecast.

What’s the difference between a business strategy and a financial feasibility study?

Feasibility studies are used to determine whether to pursue the business, whereas business plans are created after choosing to pursue the business. Methodology: Feasibility studies are essentially research projects, whereas business plans are future projections.

What is the primary assumption made in a financial plan?

All components of financial forecasting — balance sheets, income statements, cash flow statements, and business plans – rely on critical assumptions. They comprise expected sales volumes in detail and the cost of sales and general administration expenses.

Financial planning enables you to maintain an appropriate balance between the inflow and outflow of funds. It allows the firm or individual to adapt to changing market conditions and, as a result, change their plan. Are you excited about the possibility of developing your financial action plan? What are you waiting for? Begin now!