11+ Sample Insurance Incident Report

-

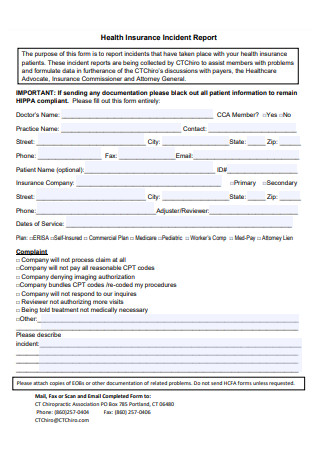

Health Insurance Incident Report

download now -

Medical Insurance Incident Report

download now -

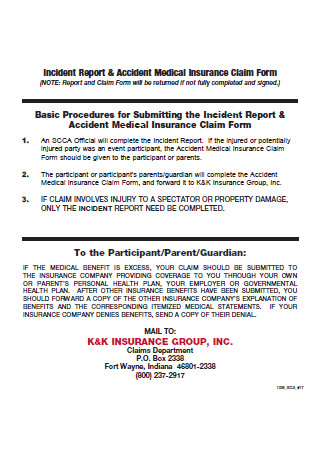

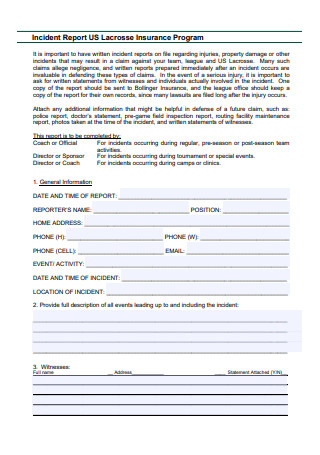

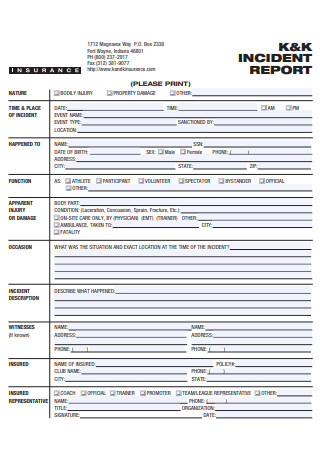

Insurance Program Incident Report

download now -

Insurance Incident Report Form

download now -

Insurance Incident Report in PDF

download now -

Formal Insurance Incident Report

download now -

Motor Insurance Incident Report

download now -

Insurance and Risk Management Incident Report.

download now -

Insurance Agent Incident Report

download now -

Public Entity Insurance Incident Reporting Form

download now -

Softball Insurance Program Incident Report

download now -

Property Insurance Incident Report Form

download now

FREE Insurance Incident Report s to Download

11+ Sample Insurance Incident Report

What Is an Insurance?

Benefits of Insurance Incident Report

Don’ts in Availing of Insurance

How to Prevent Workplace Incidents

FAQs

What is the difference between an accident and an incident report?

What is a non-reportable incident?

What is a risk incident?

What Is an Insurance?

Most people have insurance for their automobile, their home, and even their lives. However, most of them rarely consider what insurance really is or how it actually operates. Simply put, insurance is a contract, represented by a policy, in which a policyholder receives financial security or payment from an insurance provider in the event of a loss. The company pools the risks of its clients to make insurance premiums more reasonable for the insured. In 2021, an estimated 9.6% of U.S. citizens, or 31.1 million people, did not have health insurance, according to preliminary estimates from the National Health Interview Survey.

Benefits of Insurance Incident Report

There are numerous types of incidents and observations, including safety accidents and incidents, near-misses, environmental observations, IT security incidents, quality deviations, and claims, to name a few. Most of us know when something is out of place. And the most considerate among us even take corrective actions involving fixing the problem. In addition to identifying and resolving an issue, a crucial step must always be taken. This is the incident reporting portion. This section will discuss seven reasons why incident reporting is essential for businesses of all sizes and industries.

Don’ts in Availing of Insurance

There are numerous reasons to think about buying a life insurance policy, such as a recent union, the birth of a child, or the investment of a substantial debt that your loved ones might have difficulty paying off in the event of your death. Or perhaps you have observed firsthand the effect an end has on the finances of remaining family members. If you are in the market for life insurance or have recently purchased a policy, avoid making these blunders that could jeopardize your family’s financial security. Regardless of the insurance you choose, the application process will be comparable. You must enter your basic information, financial situation, and health survey responses. Frequently, you will also be required to undertake a paramedical exam, during which a skilled healthcare practitioner will examine you and may request blood and urine samples for analysis. This is due to the correlation between life insurance premiums and the statistical possibility that you will pass and the insurer will have to pay a claim. Consequently, insurance rates are frequently lowest for younger people and healthier individuals. Those with health issues or riskier habits might anticipate paying a higher premium. If you’re still interested, here are some things to avoid while purchasing insurance.

1. Delay in Purchasing Insurance

When acquiring life insurance, evaluating the coverage amount and cost is essential. Your life insurance premiums are determined by various variables, including age and overall health. Purchasing a life insurance policy rather than later can be advantageous if you wish to acquire a policy at the most affordable price. In general, life insurance premiums rise as people age, or their health deteriorates. In rare instances, illnesses or health concerns may exclude you from coverage. The longer you wait to make an investment decision, the more expensive the insurance will likely be, assuming you can purchase it.

2. Buying the Least Expensive Plan

While shopping for an affordable policy is crucial, assessing the coverage you receive in exchange is also essential. It’s a good idea to know about the features and benefits of life insurance policies, as they can be somewhat complex. For instance, temporary life insurance is typically less expensive than permanent life insurance. However, there is a caveat: term life insurance only covers you for a defined time, whereas permanent life insurance can cover you until your death, so long as the premiums are paid. If you anticipate only needing life insurance for a limited time, perhaps 20 or 30 years, a term life policy can be a cost-effective choice. Alternatively, paying more premiums for permanent coverage may be worthwhile if you choose lifetime coverage or a life insurance policy that accumulates cash value as an investment vehicle. Compare the quotes of various life insurance policies to evaluate what you may be giving up for a cheaper policy.

3. Permitting Premiums to Expire

In exchange for coverage, you must pay a premium for life insurance. Again, these rates may be determined by your insurance risk class, which is correlated with your age, health, and other characteristics. Late premium payment may affect the policy’s benefits if you’re contemplating purchasing a universal life policy with secondary guarantees — low-premium guaranteed death payments for life or for a predetermined amount of time. Universal life insurance is a permanent policy marketed as providing long-term protection at the lowest feasible premium; it is significantly different from term insurance. While many of these plans have a cash surrender value, universal life with secondary guarantees aims to maximize the coverage offered per dollar premium. Some of these policies may be sensitive to a premium payment schedule.

4. The Cost of Ignoring Insurance Is an Investment

Permanent life insurance protection with cash value is provided by variable life insurance. A portion of the premium is allocated to life insurance. At the same time, the remainder is deposited into a cash-value account that is invested in your choice of investments compared to mutual funds. Similar to mutual funds, the value of these accounts fluctuates based on the underlying investments’ performance. People frequently expect these policy values to boost their retirement income in the future. It would help if you adequately funded a variable life insurance policy to maximize its cash value growth. This necessitates continuing to pay enough premiums, especially during periods of low investment returns, and spending less than anticipated can significantly influence the future monetary value accessible to you. As with any investing account, it is essential to monitor your policy’s performance and periodically rebalance your funds to your desired allocation. This will ensure that you don’t take on more risk than you intended when you opened your account.

5. Borrowing Against Your Insurance

Permanent life insurance policies that develop cash value may be a source of funds in a financial emergency. Properly utilized, the cash value of a permanent policy can be used for any purpose, including tax-free withdrawals and loans. This is a significant advantage, but it must be appropriately managed. If you withdraw too much money from your policy and it expires or runs out of funds, all gains you have started will become taxable. In addition, you may substantially lower the death benefit payable to your beneficiaries upon your passing. If you have removed too much money from your insurance and it is set to lapse, you may be able to keep coverage by paying more premiums, provided you can afford them. When collecting the cash value of your life insurance policy, be careful to monitor it properly and consult your tax expert to avoid unintended tax liabilities.

How to Prevent Workplace Incidents

According to the Bureau of Labor Statistics, in 2020, there were 2,7 million injuries and 4,654 deaths at U.S. workplaces. Many have had injuries so severe that they are unable to work. But it shouldn’t take a terrible accident to convince business owners and managers to emphasize employee health and safety in the workplace. Use the following guidelines to prevent workplace accidents.

1. Conduct periodic risk assessments

Carry out a risk assessment of your complete workplace to identify potential health risks and injury causes. Consider the equipment employees use, the jobs they must complete, the training requirements, and the individual burden. Consider the significant dangers that disabled, elderly, and pregnant team members experience. Instruct employees to inform their boss or a superior if they believe certain activities increase their danger. Develop particular safety practices for mitigating each identified risk. Also, consider ways to enhance protection where such measures currently exist. It is usually a good idea to speak with the person performing the task since they will better understand the related process or apparatus. Record the threat posed by each hazard, the steps personnel must take to mitigate it, and routinely reevaluate each wager. If hiring new employees or relocating equipment within your facility, you should do an individual risk assessment to reduce new hazards.

2. Conduct physical evaluations for physically demanding roles

Some jobs are physically demanding, and those with a physical ailment or disability will find it significantly more difficult to execute them. For instance, a person with a history of back problems may be unable to work on a construction site or with a concert venue’s lighting rig. Numerous employers now demand that potential employees undergo physical and mental health assessments before employment offers. Some positions necessitate annual physicals if they are very labor-intensive. This may sound intrusive, but the purpose is to guarantee that the team member’s health is not at risk due to their profession.

3. Provide frequent safety and wellness training

Inform your personnel from the outset that health and safety is a company priority and what conduct you expect from them. Ensure that all applicable health and safety directives are communicated to newly hired employees. Immediately recall all affected personnel for retraining if a risk assessment shows a change in safety regulations. Numerous employees value fringe benefits, some of which are useful to the organization. Wellness initiatives, for example, encourage employees to enhance their physical and mental health. When team members’ wellness is prioritized at work, they are often more attentive, responsive, and productive.

4. Employ qualified personnel

Certain businesses and positions require licenses to function. Others are better suited for those with specific degrees and practical expertise. Conducting the necessary research to guarantee that prospective employees are competent for the position is essential. If a person is not as capable as they look or lacks real-world training, they can endanger their safety and those around them.

5. Employ enough employees

Accidents are more likely to occur when personnel is overworked. If you observe that they are struggling with the task, try to alleviate some of the burdens by recruiting additional personnel. If you do not, your employees will be more susceptible to accidents and burnout. Additionally, absenteeism may increase, which will compound the issue.

6. Maintain a tidy workplace and unobstructed pathways

A cluttered, dirty place of work is a dangerous place to be. Ensure your staff follows best practices, even simple ones like putting computer cables and power cords in the right place, so they don’t get in the way. Other things that can help are putting things away properly, cleaning up spills immediately, and only eating in certain places.

FAQs

What is the difference between an accident and an incident report?

An accident is an accidental event that results in damage, injury, or other harm. An incident is an unintended occurrence that may or may not result in damage, liability, or injury. Consequently, every accident is an occurrence.

What is a non-reportable incident?

The officer will likely label your collision as “non-reportable” if the vehicle damage is judged to be less than $1,500 and there are no reported injuries at the site.

What is a risk incident?

An incident is an adverse event associated with risk. This may include IT-related hazards, such as a data breach, or physical dangers, such as a tornado or an employee slipping and falling.

Writing or composing insurance report templates may be challenging, but doing so for your client or future attempts could be beneficial. Claiming the benefits of your plans is your right as a policyholder, consumer, and payer for the product in question. Our website also provides various options based on your requirements for action plan templates. What are you expecting? Avail of our templates now!