39+ Sample Household Budgets

-

Household Budget Sheet

download now -

Household Monthly Budget Example

download now -

Household Budget Receipt

download now -

Monthly Household Budget

download now -

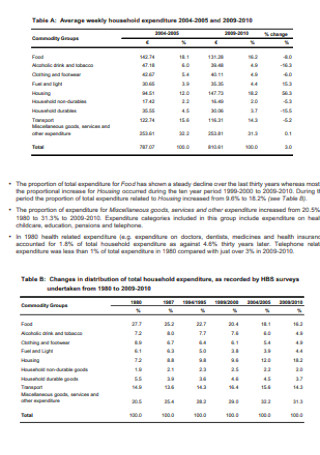

Household Survey Budget Template

download now -

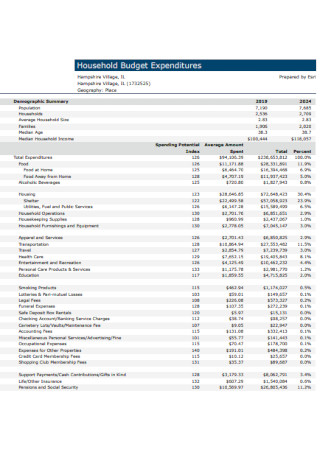

Household Budget Expenditures Template

download now -

Household Budget Notes Template

download now -

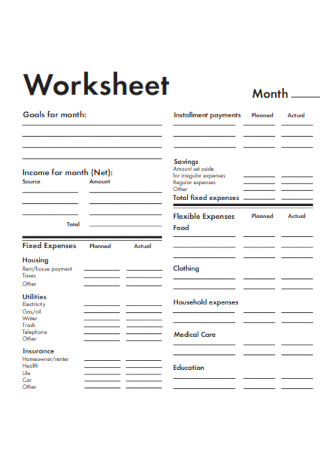

Household Budget Worksheet Example

download now -

Monthly Household Budget Template

download now -

Outlining Household Budget

download now -

Sample Household Budget Template

download now -

Household Expenses Details Budget

download now -

Household Distribution Budget Template

download now -

Sample Household Budget Worksheet

download now -

Formal Household Budget Template

download now -

College Household Budget

download now -

Household Negotiation Training Budget

download now -

Household Food Budget Template

download now -

Household Budget Checklist Template

download now -

Household Budget Survey Format

download now -

Household Budget Format

download now -

Household Work Budget Template

download now -

Printable Household Budget Template

download now -

Household Planning Budget Template

download now -

Professional Household Budget Template

download now -

Household Monthly Budget

download now -

Household Survey Budget Example

download now -

Household Budget Affordability Template

download now -

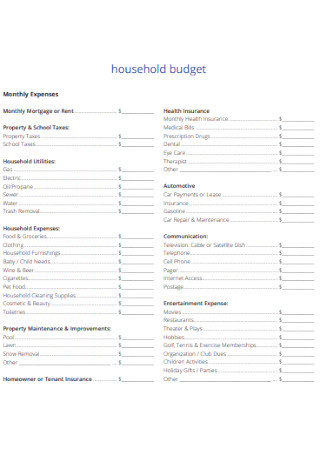

Household Budget Expenditures Example

download now -

Household Income Budget Template

download now -

Basic Household Budget Worksheet

download now -

Office Household Budget Template

download now -

Household Monthly Expenses Budget

download now -

Household Data Budget Template

download now -

Household Financial Budget

download now -

Household Original Survey Budget

download now -

Basic Monthly Household Budget

download now -

Household Financial Planning Budget

download now -

Household Budget Questionnaire

download now -

Household Management Budget Template

download now

FREE Household Budget s to Download

39+ Sample Household Budgets

What is a Household Budget?

Major Household Budget Categories

How to Create a Household Budget

Non-essential Household Budget Categories

FAQs

How can a household budget be used?

Why is it important to have savings in the household budget?

What does a good household budget worksheet look like?

Do household budgets need to be detailed?

What is a Household Budget?

A household budget, like a personal budget, is an itemized list of income and expenses that will help you plan on how money that you earn will be spent, saved, or shared. Aside from that, it will also help you understand your spending habits and gain accurate insight to analyze your spending behavior. In other words, this will help you better understand what you can and what you cannot afford.

It is especially important for people to have a household budget as it will help ensure that they do not run out of money each month. It will also allow you to save money for your goals or during emergencies as well as find some extra funds that you can share with charitable organizations, fundraising events, and even tithing.

A household budget can also give you an accurate picture of your cash flow—meaning you will see what’s coming into and going out of your bank account. If you rely only on credit cards and loans to pay for your bills, chances are, you will incur huge debts in the long run.

If you’re only starting out, it may feel like it’s a scary thing to tackle especially if you’re living on your or with a partner for the first time. And that’s a valid feeling to have—even experienced homeowners with kids find budgeting for a family and managing their monthly household expenses to be challenging. But what’s important is to face your financial situation head-on and create a household budget that works so you will have a better grasp of your finances and your limitations.

Major Household Budget Categories

Most American households have the same budget categories on their list of household expenses. These are the basic necessities such as shelter, food, transportation, and clothing. However, it may vary depending on your situation or stage in life. Budgeting for home maintenance may be included for homeowners, parents will want to allocate funds for childcare or college tuition, and healthcare and young adults may still be paying off student loans.

Here are some of the major household budget categories that should be included in your plan:

How to Create a Household Budget

Typical household expenses follow a usual schedule—utilities are typically due around the same date, insurance payments can be enrolled in auto-payment schemes, and grocery shopping is done regularly. In general, a home budget is created monthly and adjusted accordingly. Refer to the steps below to get you started with your household budget.

Step 1: Calculate Your Household Budget Income

You start your household budget by figuring out your household income each month. Add all of your reliable sources of income such as paychecks and wages, alimony, and child support, among others. If you have other means of earning like from a hobby or odd jobs but not regularly, don’t include them as income in your household budget. Keep in mind that your budget should only reflect reliable income to make this document be more dependable.

Step 2: Make an Inventory of Household Expenses

Household expenses can either be fixed or variable. Some categories, such as housing, medical, and healthcare, and savings and debt payments are fixed while the others vary depending on usage and consumption. For your variable expenses, write down the maximum amount that you’re willing to spend on them. Tally your current spending to see how you’re doing right now to reflect accurate costs. You can also review your previous bank and credit card statements to help you figure out your usual expenses each month and uncover expenses that you might have missed.

Step 3: Calculate Household Net Income

After listing down your income and expenses, calculate how much you have left, and work from there. You want this to be more than zero and be on the positive side so that you have more room to adjust your household budget for other categories. A high amount of household net income will also provide you more opportunities to save or allocate more for debt payment. In the event that this yields a negative net income, you need to make adjustments to your expenses.

Step 4: Makes Adjustments to Your Expenses

In situations where your household expenses are more than your income, you will get a negative net income and will most likely result in more debts. To prevent this, you need to make adjustments to your spending habits. You are spending more money than you make, so you need to take a look at your budget and identify what you do not need or spend less on. Revisit your categories and see where you can adjust your costs. The easiest place to look at is your variable costs. You may reduce the number of times you dine out or get delivery and take-outs, opt for a movie night at home instead of going to the cinema, etc. Fixed expenses like your phone bill or gym membership can also be reduced. The key here is to make a distinction between your wants and your needs.

Step 5: Monitor and Track Your Spending

On each month, you need to monitor and track your actual spending versus what you have budgeted. Going over budget on certain things will help you determine where you spend most of your money. Tracking your spending will help you learn from it so that in the future, you will be more mindful of your spending habits and not overspend in that area. When you overspend, you also need to adjust your monthly household budget in one area and decrease in another category to keep your budget balanced and avoid incurring debt.

Step 6: Revisit your Monthly Household Budget as Needed

Just because you have completed writing down your monthly budget, it doesn’t mean that you don’t have to take a look at it anymore. If anything, you should revisit the figures you entered in your household budget as priorities, expenses, and income change over time. It is always wise to adjust your household budget according to these changes.

Non-essential Household Budget Categories

When you find that you have the extra money in from your household budget, this could go to your discretionary funds. This is the money that you can use for non-essential items like personal expenses, entertainment, and gifts, and rewards. As the name implies, these categories in your household budget are non-essential and should only have an allocation if and only if you have excess income.

These non-essential categories are also the areas in your household budget that you can easily cut back on should you want to increase your percentage of paying off debts or build your savings more quickly.

Personal Spending. This is the catchall phrase for anything you spend on yourself that is not necessary for your life. This could be gym memberships, home decors and furnishings, and gifts, among others.

Recreation and Entertainment. This category can be referred to as “fun money” and it is important that you remember that. Spending something for yourself is crucial to maintain that healthy work-life balance. Concert tickets, sporting events, vacations, and other family activities, hobbies, and video games, can be considered under this category.

Miscellaneous. In the event that your personal spending category has been maxed out, anything extra can go into this category. Also, other expenses that cannot be accounted for in the major categories and non-essential categories should be included here.

FAQs

How can a household budget be used?

A household budget is typically used every month. It’s a tool that you use to help you:

- Determine where you spend your money

- Find out where you can save money for the future

- Plan how you can spend and save money

Why is it important to have savings in the household budget?

Savings is a crucial category in your household budget. It can be difficult to save especially when you don’t feel its impact on a daily basis. Some of the reasons why you need to save even when it’s not easy are as follows:

- Emergency purposes or expenses that you do not expect to have

- Big-ticket purchases or to pay for expensive things like a car, trip, or security deposit for an apartment

- Financial and life goals like paying for tuition and classes, or visiting a family member or friends living overseas

What does a good household budget worksheet look like?

A household budget template or sample excel spreadsheet should reflect the reality of your household expenses. There are many downloadable budget worksheets on this website that you can use for free. These can be tailored to fit your current financial situation and can also be adjusted over time or as your circumstances change.

Do household budgets need to be detailed?

As much as possible, you must include every detail of your reliable income and all expenses or outgoings in your household budget. This will help you get a more accurate picture of your financial situation and will only help you manage all your finances better and make money management at home easier to do.

When you think about a household budget, remember that it is the foundation of any sound financial management plans that you might have. Building your own household budget requires a thorough step-by-step process and constant vigilance. With a good budget, you will be able to reach your ideal spending habits and achieve your savings goals. It is necessary to list down your income and expenses for easy tracking and monitoring. If you’re unsure of how to start, you may choose from any of the available templates on our website.