29+ Sample Monthly Household Budgets

-

Sample Monthly Household Budget

download now -

Monthly Household Income Budget

download now -

Monthly Household Budget Worksheet

download now -

Monthly Household Budget Spending Plan

download now -

Building Monthly Household Budget

download now -

Household Budget Worksheet Example

download now -

Monthly Household Budget Template

download now -

Monthly Household Budget Worksheet

download now -

Monthly Household Cash Budget Template

download now -

Monthly Household Budget Sheet

download now -

Household Monthly Budget Example

download now -

Monthly Household Budget Receipt

download now -

Monthly Household Survey Budget

download now -

Monthly Household Budget Expenditures Template

download now -

Sample Household Budget Worksheet

download now -

Formal Household Budget Template

download now -

College Monthly Household Budget

download now -

Monthly Household Budget Checklist Template

download now -

Monthly Household Budget Survey Format

download now -

Monthly Household Budget Format

download now -

Household Work Budget Template

download now -

Household Monthly Budget

download now -

Household Survey Budget Example

download now -

Household Budget Affordability Template

download now -

Sample Monthly Household Budget Worksheet

download now -

Monthly Household Income Budget Template

download now -

Basic Monthly Household Budget Worksheet

download now -

Office Monthly Household Budget Template

download now -

Monthly Household Original Survey Budget

download now

FREE Monthly Household Budget s to Download

29+ Sample Monthly Household Budgets

What Is a Monthly Household Budget?

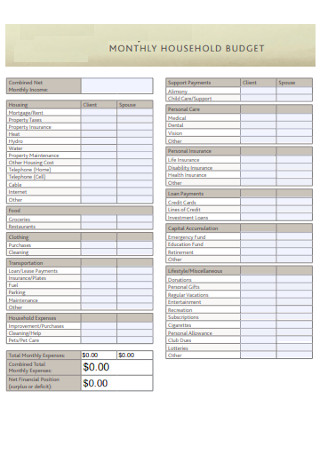

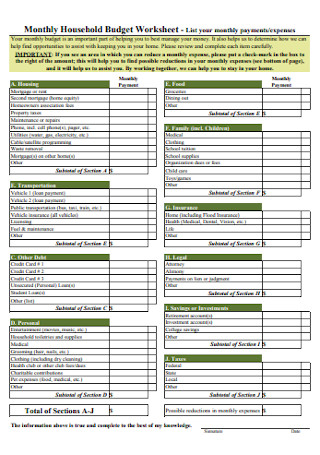

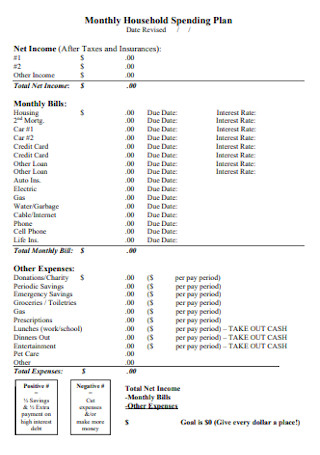

Components of a Monthly Household Budget

How to Create a Monthly Household Budget

FAQs

How do you budget for one-time expenses?

How to maintain and update the monthly household budget?

Why are there always expenses that do not fit into your budget?

What Is a Monthly Household Budget?

A monthly household budget contains similarities to a personal budget or a home budget. It is a financial plan that allocates future funds and income towards expenses, savings, or debt repayment. A household budget allows detailed, specific, accurate, and transparent data about future and current funds stipulated over a month and their effect on expenses and expenditure of a household. It also serves as a reference for record-keeping when there are inaccuracies or a shortage of funds. It is also essential to track the amount of money that enters the household and the amount that comes out, especially when increases in budget allocation happens or the use of emergency fundings.

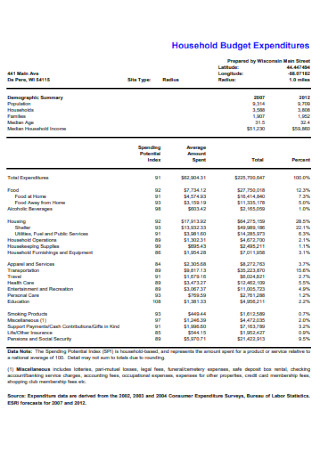

According to the Consumer Expenditure Survey conducted by the United States Bureau of Labor and Statistics, the average annual expenditures increased by three percent from 2018 to 2019, now amounting to 63,036 US dollars. Despite the rise in people’s incomes, the allocation of funds remains the same, and people are left to budget their spending according to increases and decreases of prices in the market.

Components of a Monthly Household Budget

The constant movement of money in and out of an individual’s account and a monthly household budget helps track where the money goes. Most monthly household budgets are in a tabular form. It is easier to understand and manage income and expenses. Below are the most common components found on a monthly household budget.

How to Create a Monthly Household Budget

For any household, it is imminent to have a comprehensive budget plan. After knowing the necessary parts of the budget, a well-structured household budget must follow. If not for a well-structured budget, overspending and inaccuracies of record-keeping are inevitable. Here are the steps to follow when creating a monthly household budget.

Step 1: Start by Creating a Tabular Budget Sheet

Most budgets are constructed in a tabular format, regardless if it is a travel budget, a personal budget, or other budget plans. Plenty of templates are available online to start in creating a well-structured plan for the month. Ensure that the template selected is easily accessible and understandable.

Step 2: List the Monthly Income

Identify the contribution of income each member of the household brings in during a month, and add all reliable sources of profit. Reliable sources meaning the monthly revenue is continuous and constant. Cash from inconsistent jobs and money from hobbies must not be in the budget. Only indicate dependable sources of income, including job wages, and if applicable, child support and alimony. In the case that an individual is self-employed or has fluctuations in terms of pay, use an average monthly income or an estimated amount of revenue in a single month.

Step 3: Add up All the Expenses

Monthly expenses can either be fixed or not. Fixed charges include rent or mortgage, property taxes, and state-mandated taxes. Others vary depending on the usage of necessity, and it includes items such as utilities, groceries, transportation, among others. List all fixed amounts along with the value of each. For fluctuating expenses, it is advisable to estimate a maximum value for spending or a prediction of the bill. Utilize previous bank or credit statements in calculating the total amount of payments per month. In reviewing records, uncategorized items help in calculating the amount spent in prior months. Some of the varying expenses do not occur each month, and it is essential to include them in the budget as it is easier to identify and afford them when necessary.

Step 4: Calculate for the Net Income

Net income is the total amount left over after the deduction of all expenses. The net income must show a positive net income to put into debts, and if there is still money left, move it into savings. It is necessary to compute the net income to see if the salaries make up for all the expenses in the household. Write the income even if it turns out to be negative.

Step 5: Adjust the Budget According to Necessary Expenses

Based on the net income, the monthly budget must undergo necessary adjustments, especially if the result turns out to be negative. It is vital to make the corrections to avoid unnecessarily overspending on the wrong items and eventually going into debt. The varying expenses are the easiest to adjust in terms of spending, and the fixed rates can also undergo substantial adjustments. The best way to balance the budget is to weigh between wants and needs. Reducing the budget for things out of desire makes room for adding funds in necessary categories.

Step 6: Always Track Spending Patterns

The final step to any well-made monthly household budget is to track actual spending. If there is a possibility of going over budget, doing this ensures an alternative in deducting money from the budget. In following the expenses, it shows patterns to prevent overspending or to make the necessary adjustments to compensate for it. There must always be a balance in budgeting expenses to ensure fulfillment of dues at the end of the month.

FAQs

How do you budget for one-time expenses?

One-time expenses are tricky to include in budget plans and may cause a dip in your budget if not planned properly. There are three types of one-time charges, and it is advantageous to learn about them to set yourself up from overspending. One of the three are expenses that come each year. It includes holiday gifts and annual taxes, and you can allocate a small amount each month for these expenses by looking at the previous year’s records and identify how much money is for these one-time charges. Occasional expenses are also one-time expenses. These unplanned expenses are usually called emergency funds and must reflect in your budget. One way of creating emergency funds is to classify them according to their use. Most people use cash in allocation and put it in sealed and labeled envelopes to keep funds handy for various purposes. The goal is to allocate a sufficient amount to cover the repair cost or emergency expenses. Lastly, real emergencies need a certain amount of funds, for example, losing your job or a medical accident not covered by insurance. In this case, make sure to allocate three to six months’ worth of funds to cover living expenses and other necessities connected to the emergency.

How to maintain and update the monthly household budget?

It is essential to review your credit and account statements regularly. In doing so, you’ll have an idea of your spending habits. Once you have an idea of the figures, use the opportunity to compare them to the amount you allocated for your monthly budget and support any adjustments made to balance out the amount to cater to your spending habits. In this way, budgeting becomes easy and almost effortless. There are situations when one-time expenses are necessary, and this allocation must add up over a year rather than every month. Not keeping your budget current to your needs, wants, and future goals prevents you from enjoying your current funds. Planning correctly and accurately ensures you have both fun at present and savings for the future.

Why are there always expenses that do not fit into your budget?

One of the common reasons people stop keeping a budget is because some expenses are not in a particular classification. It’s essential to indicate miscellaneous fees as part of the monthly household budget. These expenses come from previous purchases made in the course of a few months with an estimated average. A simple re-evaluation of the original budget for any missing categories goes a long way. Analyze the estimates of the amount if there are inconsistencies and inaccuracies and fix them as necessary. Classify and identify as many categories as you can from previous billing statements and tailor them to your spending patterns. The budget you make must reflect all spending possibilities of the entire household.

Having a household budget is an essential part of keeping track of expenses. It allows you to see where the family’s income goes and if there is money left over. It is necessary to allocate money for all necessities at home to ensure that the settlement of dues is without delay. There are plenty of ways to start budgeting, and it’s relevant that every person in the household is present while planning. It is essential that everyone knows the budget and stick to it to avoid over-splurging and debt. In the words of Rosette Mugidde Wamambe, a management coach and trainer, “Budgeting is not just for people who do not have enough money. It is for everyone who wants to ensure that their money is enough.” Plan your monthly household budget using the samples found above and ensure your money is where it’s supposed to be.