49+ Sample Monthly Budget Worksheets

-

Monthly Household Budget Worksheet

download now -

Monthly Expenses Budget

download now -

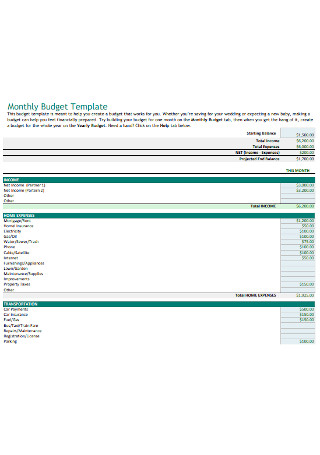

Detailed Monthly Budget Template

download now -

Sample Monthly Budget Worksheet

download now -

Monthly Financial Budget

download now -

Monthly Budget Worksheet Example

download now -

Basic Monthly Budget Worksheet Template

download now -

Monthly Home Budget Worksheet

download now -

Monthly Business Budget Template

download now -

Personal Monthly Budget

download now -

Monthly Marketing Budget

download now -

Monthly Budget Sheet

download now -

Teens Monthly Budget Template

download now -

Sample Monthly Budget Example

download now -

Monthly Course Budget Template

download now -

Sample Monthly Budget for Adults

download now -

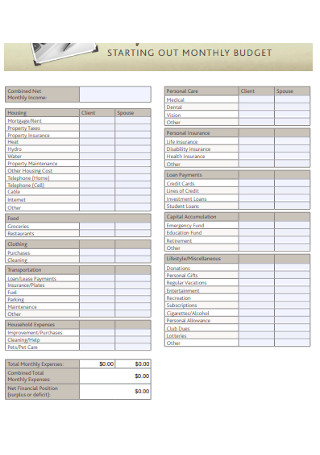

Homeowner Monthly Budget

download now -

Mutual Monthly Budget Template

download now -

Honest Monthly Budget

download now -

Basic Monthly Budget Template

download now -

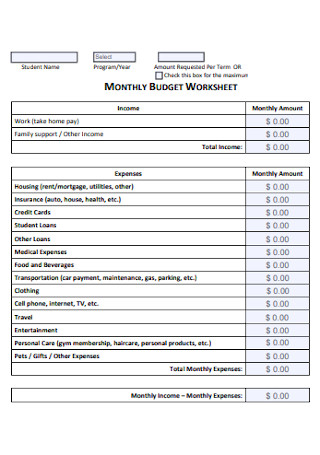

Monthly Budget Estimate for Students

download now -

Monthly Food Budget

download now -

Monthly Income Budget Worksheet

download now -

Formal Monthly Budget Template

download now -

Monthly Budget Format

download now -

Monthly and Annual Budget Template

download now -

Monthly Expenses Budget Template

download now -

Household Monthly Budget Example

download now -

Simple Monthly Income Budget

download now -

Individual Monthly Budget

download now -

Monthly Budget Report Template

download now -

Monthly Family Budget Template

download now -

Monthly Budget Verification Form

download now -

Monthly Budget Spreadsheet

download now -

Personal Monthly Budget Sheet

download now -

Monthly Spending Plan Budget

download now -

Current Monthly Budget

download now -

Monthly Expense Tracker Budget

download now -

Personal Monthly Budget Template

download now -

Monthly Budget Statement Template

download now -

Monthly Budget Planner Template

download now -

Standard Budget Worksheet Template

download now -

Your Monthly Budget Worksheets

download now -

Printable Monthly Budget Template

download now -

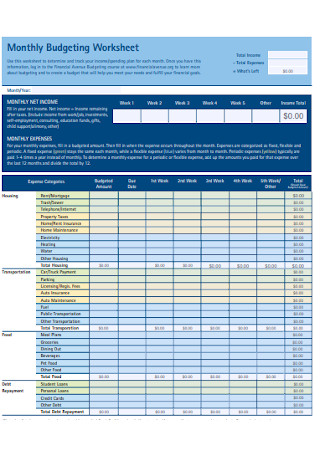

Monthly Budget Expense Worksheet

download now -

Simple Monthly Budget Worksheet

download now -

Office Monthly Budget Template

download now -

Financial and Monthly Budget Template

download now -

Monthly Rent Budget

download now

FREE Monthly Budget s to Download

49+ Sample Monthly Budget Worksheets

What is a Monthly Budget?

Different Types of Expenses

How to Create Your Own Monthly Budget

General Budgeting Tips

How to Prepare for Whammy Expenses

FAQs

When should I start creating my monthly budget?

What should I do if I overspend for a certain expense?

How can I ensure that I can reach my financial goals?

What is a Monthly Budget?

A monthly budget is a list of estimated monthly expenses and income that goes in and out of your financial accounts over the course of a month. It is usually compiled and evaluated on a regular basis to assess if it’s working or not. It can be your personal monthly expense list, for your family, business, government, or just about anything.

What’s important to know about the monthly budget is that it helps manage monthly expenses for unpredictable events that may come your way, allows you to afford big-ticket purchase without drowning in debt, and keep track of your cash flow.

The great thing about a monthly budget is that you don’t need to learn about complex math skills or refrain from buying the things that you like. Monthly budgets are records of your income and expenses. It gives you an idea of where your money goes like your average food and transportation expenses and allows you to gain more control over your finances.

In essence, a monthly budget is basically a financial plan for a definite period and can help improve the success rate of any financial undertaking.

Different Types of Expenses

Before taking out your monthly budget calculator and diving into your own personal budget spreadsheet, you must first know the different types of expenses and why they matter.

How to Create Your Own Monthly Budget

A monthly budget is not a magic trick—it’s a plan for every penny that you have. It’s a representation of your financial freedom and more relaxed and less stressful life. Here’s how you can set up your own personal budget spreadsheet.

Step 1: Calculate Your Net Income

Create your monthly budget plan by entering all of your net income. This means all of your earnings for the month including those that you get from your regular paycheck and any extra money you get from side hustles, freelance work, garage sale, and the likes. If you are self-employed and have variable income, you can use your lowest-earning month as a baseline when you set up your budget.

Step 2: Gather All Financial Statements and List All of Your Expenses

Your financial statements will provide you with the information that you need so you can list down all of your fixed and recurring expenses. The more information that you can dig up, the better coverage you will have. Armed with these facts, you will be able to get a monthly average of your expenses. This will also enable you to create a monthly expense list that includes payments for mortgage or rent, car, and insurance, utilities, groceries, entertainment, and other miscellaneous. It would be helpful if you use your bank statements, receipts, and credit card statements in the past three months so you can identify all of your spendings and get more realistic figures.

Step 3: Identify Fixed Expenses from Your Variable Expenses

After creating your expense list, you need to identify which ones on it are fixed expenses or those that are mandatory expenses that you need to pay the same amount every month on the same date. Variable expenses, on the other hand, changes from time to time such as groceries, gasoline, entertainment, and eating out. These expenses can either be recurring or non-recurring.

Step 4: Determine Your Average Monthly Expenses

You can look up you’re your bank, bills, and credit card statements to know how much you spend on each item on your expense list per month. Fixed expenses are easier to list and your variable expenses may vary each month, but is generally the same and falls within a certain range and do a little math to find the average rate. Once you have itemized your expenses and their respective amount, subtract it from your net income. You are off to a good start if your income is higher than your expenses. But if you are spending more than you’re earning, this means you are overspending and need to make necessary changes.

Step 5: Make Adjustments to Your Expenses

When you’re in a situation where you have more expenses than income, then you may be overspending or have not properly planned for big-ticket purchases or whammy expenses. In these cases, you need to revisit your lifestyle, check your expenses, and cut loose things that bleed your finances. Look for places where you can reduce your spendings such as opting to dine at home than eating out, cancelling gym membership, and other entertainment. Your aim is to at least have your income and expenses to be balanced which means your income is properly accounted for and budgeted towards specific expenses of savings goals. It is a good practice to reduce your monthly expenses and regularly make adjustments on how much you spend to avoid incurring debts.

General Budgeting Tips

After creating your monthly budget, the next step is to stick to your monthly budget list. Keep in mind that the goal of a monthly budget is to have your expenses lower than your income so you can work towards your savings goals. Here are some other tips so you can avoid overspending and focus on your savings goal.

Set a Preset Spending Amount

You can set reminders on your credit card and bank accounts if you have already reached your spending amount per month. Once you reached your limit, you can either stop your cash flow towards that expense or reallocate your finances from another category to cover any additional costs.

Track Your Expenses

If possible, list all your expenses as soon as you made them by writing them down into your monthly budget template or your budgeting app. Use budgeting hacks like switching to cash payment only or divide payments by week if you tend to spend on certain categories.

Adjust Your Monthly Budget Accordingly

If you find that you are either overestimated or underestimated your income and expenses, make adjustments. Make sure to watch out for expenses that occur every few months but will make a dent in your plans such as insurance payments or unexpected or emergencies.

Overhaul Your Monthly Budget Plan if It’s Not Working for You

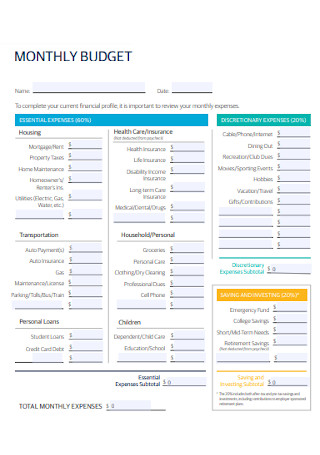

Many financial experts believe that a good monthly budget plan follows the 50/30/20 rule. This method suggests that your income should be divided into three categories: 50% living expenses or your needs, 30% goes to your wants, and 20% goes to savings and debt payment. But it isn’t a one-size-fits-all solution to your financial needs. If you feel like your monthly budget planner is not helping you reach your goals, it may need to undergo a serious overhaul.

Prepare for Whammy Expenses

Although unpredictable and unexpected, whammy expenses may happen at any time so it is best to prepare for them. This way, you won’t have to dip into your savings or prevent incurring huge debts. One of the best ways to prepare is to have your own emergency and calamity funds which you can use for your worst-case scenarios.

How to Prepare for Whammy Expenses

Knowing the different types of expenses is crucial in understanding how budgets work and how you can prepare for unexpected ones.

Reduce Your Fixed Expenses

You already know that your monthly bills such as housing, phones, internet, and insurance are necessities that take up a huge chunk of your budget. These are important fixed expenses but ones that can be reduced especially if you have a savings goal. Some of the things you may consider are:

- Finding a more affordable and less expensive place to live

- Changing your phone plan to a cheaper one

- Getting a new insurance company with more coverage at a lesser cost

- Avoid food waste by doing grocery shopping once a week

Clear Off Debts

When your budget allows, pay off your debts slowly and start with the lowest balance first or the one with the highest interest to save you more money in the long run. Most importantly, allot a space for debt payment in your monthly budget. Set up payment plans even if you can only afford a few dollars at a time. This way, you can show your lenders that you’re paying something and it can also help you improve your credit score.

Build Your Emergency Funds

Any financial advisor will tell you that aside from paying off your debts, the next best thing you can do for yourself is to build your emergency funds—even if you save only the bare minimum. At the end of the day, your emergency fund will pay for your large and unexpected expenses such as unforeseen medical expenses, repair or replacement of important home appliance major car fixes, and unemployment. Emergency funds are designed to create a financial buffer in these situations so you should have saved an amount that can cover all your living expenses for at least 3 to 6 months or longer. Remember the right amount of savings depends on your financial situation.

FAQs

When should I start creating my monthly budget?

Now. You don’t need to wait for payday to start budgeting or for you to pay off your loans and debts. The right and best time to start is now so you can work towards your financial freedom sooner. Take a good look at your financial situation and assess where you are right now from your financial goals.

What should I do if I overspend for a certain expense?

Reallocate your funds from other categories to cover the additional costs. You should also stop cash flow towards it to ensure that you do not overspend your overall monthly budget.

How can I ensure that I can reach my financial goals?

Stick to your monthly budget and automate your savings. Think about your savings as a fixed expense that’s non-negotiable. Your income, expenses, and priorities will change over time, so you will also need to revisit your budget and adjust accordingly.

A monthly budget is designed for you to track your income and expenses. It ensures that you pay your bills on time and prevent overspending. It also helps you prepare for upcoming bug ticket expenses and set aside funds for unexpected expensive repairs or home appliance replacements. But most importantly, monthly budgets can help you reach your financial goals and work your way towards your financial freedom and independence.