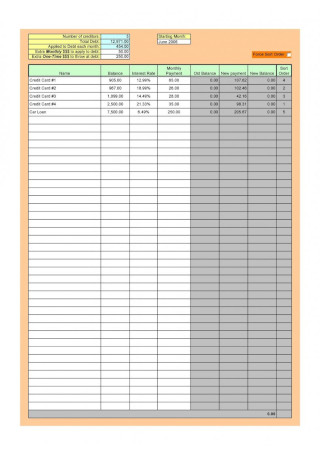

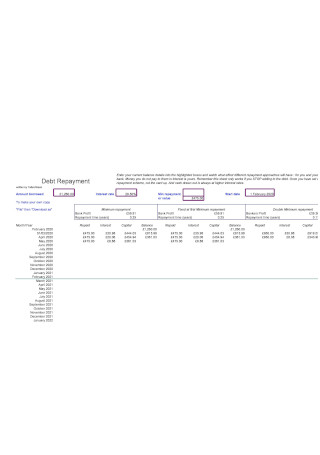

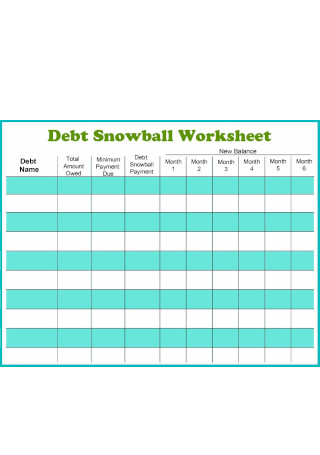

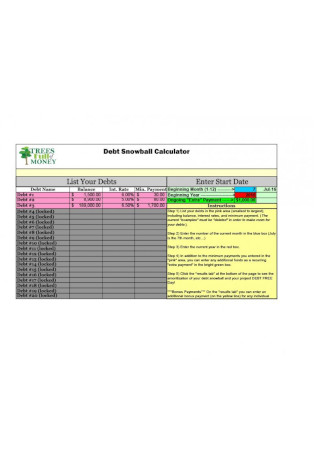

35+ SAMPLE Debt Snowball Spreadsheets

-

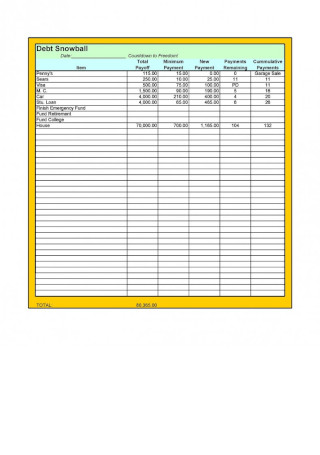

Debt Snowball Spreadsheet

download now -

Debt Reduction Calculator

download now -

Debt Snowball Management Spreadsheet

download now -

Debt Snowball Spreadsheet Template

download now -

Debt Reduction Calculator Sample

download now -

Debt Snowball Spreadsheet Guide

download now -

Debt Worksheet Template

download now -

Editable Debt Snowball Spreadsheet

download now -

Reducing Debt Sheet

download now -

Consumer Debt Snowball Spreadsheet

download now -

Debt Snowball Spreadsheet Sample

download now -

Debt Paydown Worksheet

download now -

Debt Snowball Worksheet

download now -

Paydown Debt Snowball Worksheet

download now -

Debt Snowball Spreadsheet Format

download now -

Simple Debt Snowball Spreadsheet

download now -

Debt Reduction Spreadsheet

download now -

Debt Reduction Spreadsheet Sample

download now -

Debt Payoff Spreadsheet

download now -

Debt Snowball Plan Form

download now -

Easy Debt Snowball Worksheet

download now -

Debt Snowball Form

download now -

Basic Debt Snowball Spreadsheet

download now -

Debt Snowball Spreadsheet Form

download now -

Sample Debt Snowball

download now -

Debt Snowball Form Template

download now -

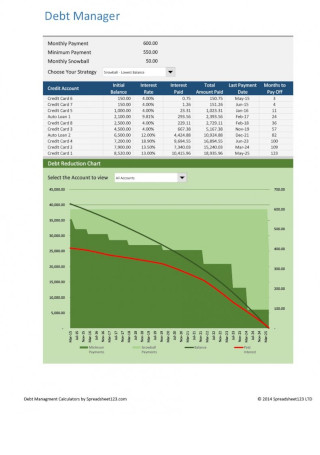

Debt Manager Spreadsheet

download now -

Debt Snowball Form (10)

download now -

Professional Debt Snowball Spreadsheet

download now -

Debt Snowball in PDF

download now -

Standard Debt Snowball Spreadsheet

download now -

Debt Repayment Spreadsheet

download now -

Basic Debt Snowball Worksheet

download now -

Debt Snowball Worksheet in PDF

download now -

Debt Snowball Calculator Sample

download now -

The Debt Snowball

download now

FREE Debt Snowball Spreadsheet s to Download

35+ SAMPLE Debt Snowball Spreadsheets

What Is Debt Snowball?

How to Effectively Set Up Your Debt Snowball Spreadsheet

Types of Debt Payment Strategy

FAQs

What are the types of loans that you may incorporate in the debt snowball strategy?

How do you stay motivated in implementing the Debt Snowball Method?

Can we include mortgages in the Debt Snowball Strategy?

What Is Debt Snowball?

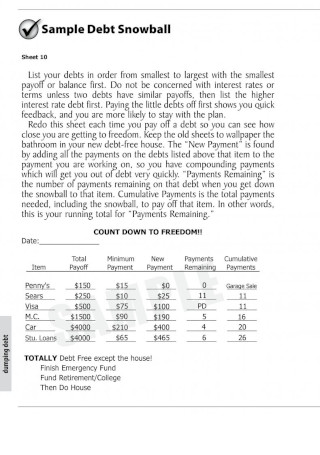

With the influence of finance expert, Dave Ramsey, the Debt Snowball has become one of the most popular debt-reduction strategies that anyone can use to pay off debts. In this strategy, you start by paying the small ones and move to the next smallest one until you pay off all of your debts. Now, you may be wondering what makes it work? Definitely, there are better strategies to pay off debt, but from a psychological standpoint, it may be the best. By achieving something in a short time, you get motivated to do it consistently, which is why many find this strategy effective.

Let us give you an example of how it works. Let’s just say below is the list of your debts.

$600 medical bill($60 monthly payment)

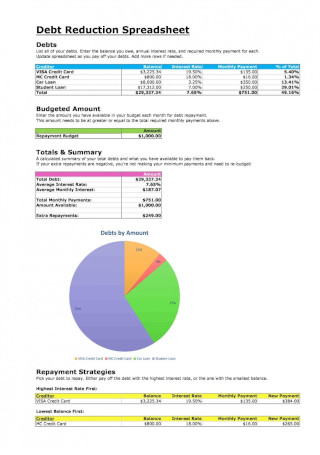

$3,000 credit card debt($87 monthly payment)

$7,500 car loan($140 monthly payment)

$20,000 student loan($169 monthly payment)

$25,000 personal Loans($180 monthly payment)

Normally, you will be paying a total of $636, but the goal is to pay off these debts sooner than their terms. Therefore, instead of paying the usual monthly bills, if you can pay more than that, you will use it to pay the smallest loan, which, in this case, is the medical bill. You are now completely free of one debt. You will continuously do it until you completely pay off all of your debts.

Did you know that Debt Snowball is part of Dave Ramsey’s 7 baby steps? In case you don’t know, Dave Ramsey is an American finance personality, who wrote on his website ways on saving for emergencies and strategically paying loans. In the article, he advised to pay off all the non-mortgage loans through Debt Snowball. According to thebalance.com, in 2019, the average credit card debt in the US is $6,194, which is three percent higher than the 2018’s average credit card debt. This type of debt has become the fastest-growing debt type in the country, making it a very common financial issue. That said, Debt Snowball Strategy may be a way to get out of this financial trap. Read further to know more.

How to Effectively Set Up Your Debt Snowball Spreadsheet

With the printable debt-reduction free downloadable samples and templates that we have gathered in the previous section, you can now create your Debt Snowball Spreadsheet, but before you use them, because, just like executing an outstanding online marketing strategy, to ensure that you can utilize this strategy properly, there are certain steps that that needs to be considered. It will save your time as well since these steps will ensure that you have all you need before you get started.

1. List Down All Your Debts.

This may not be the case for everyone, but a lot of people don’t know the details of each of their debts, or they just forgot about it because they are only focusing on what they need to pay every month. It’s time to change that. Retrieve your medical receipts and other receipts that contain the details of your loans. Call the firm where you got the loan if you don’t have them anymore. These days, many loan businesses provide their clients the option to view their loan payments online. You may want to take advantage of that to save your time.

2. Compute Your Total Monthly Payment.

Once you have created a list of all your debts, list down each of its monthly payments and compute the total amount. If you have loans that let you pay quarterly or anything apart from the monthly, compute how you will pay if you pay it every month. For example, below is the list of your debts:

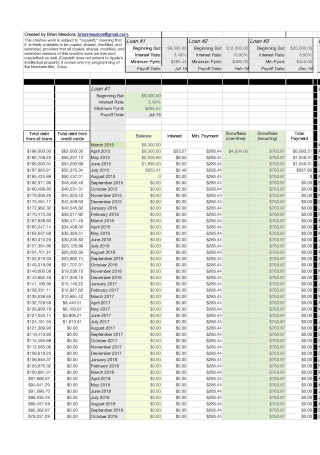

$460 medical bill($30 monthly payment)

$2,3400 credit card debt($70 monthly payment)

$8,000 car loan($145 monthly payment)

$20,000 student loan($507 quarterly payment, $169 quarterly payment)

Your total monthly payment is $414.

3. Compute the Total Remaining Amount of Each Debt.

In the previous step, you got your total monthly payment. Now, let’s get the total remaining amount of each of your debts. You can call the loan company to get this detail or view it online if the loan company allows you to do it. Alternatively, if you can still remember until when you will be paying for the loan, you can compute it on your own by multiplying your monthly payment and the number of months that you are yet to pay.

4. Determine How Much You Can Pay on Top of Your Monthly Payment.

This step can be the most tricky part. You may have to resort to another tool, such as a budget plan for you to determine how much you can pay on top of your monthly payment. Determine your monthly expenses, which should cover your monthly loan payments and all the planned expenses within a year. Then, deduct them from your expected monthly income. At this moment, you have the amount that you can pay on top of your monthly payment.

5. Make Necessary Adjustments.

The good thing with Debt Snowball is its flexibility. You can always make adjustments to the plan in case relevant events occur. For instance, after you have planned out your Debt Snowball, your family from another state decided to visit your home in a month. You may not want to decline them. If you want to, you can ditch the plan for the current month to prepare for a gathering, but, of course, you need to take it into account. If you are targeting a certain date to completely pay off all your debts, you can play around with your weekly expenses. Perhaps, you will want to end some of your streaming services for a few months or use the cheaper alternatives.

6. Compute the Snowball Effect.

This step may be your favorite because it will allow you to see the results of this strategy. Let’s say your total monthly payment is $414 and you can pay $200 on top of it. You will be debt-free in no time!

Types of Debt Payment Strategy

Just like specific sale strategies, while Debt Snowball may work for many people, it may not work for everyone. The drawback of using Debt Snowball as a way of paying off debts is, over time, you may still end up paying more money in the loan interest. If this is the case, you may want to consider using other types of Debt Payment Strategy such as the following.

Debt Avalanche: Similar to Debt Snowball, with Debt Avalanche, you will pay an amount on top of the current total monthly payment, but the difference is you will tackle the biggest amount first. Meaning, instead of paying the extra amount to your smallest debt, you will apply it to the biggest amount first. Mathematically speaking, this strategy is more effective because some loan businesses may lessen the interest that you would normally have to pay if you pay them earlier than promised. The thing with this strategy is you may easily lose your motivation since it may take time to tackle each loan. The good thing is it gets easier every time you completely pay off each debt. Debt Consolidation: Thinking about your multiple loans can be messy. Thus, if you have the option, you may want to consolidate all of them into one loan to make it simpler through Debt Consolidation. There are several methods to apply Debt Consolidation, but the most common ones are through personal loans and balance transfer credit cards. A balance transfer credit card allows you to move a high-interest loan to another credit card that has a lesser interest, which is one of the best benefits of applying Debt Consolidation as your debt-reduction strategy. The thing with Debt Consolidation is it usually requires good credit, making it not applicable to everyone. Debt Management Plan: As we have mentioned, the worst case of having several debts is getting drowned to them. If you are in this situation, this debt payment strategy is for you. By approaching a credit counseling agency, you may solve this problem. This agency type offers a debt management plan. As part of it, they may negotiate with your creditors with your loan details, such as the monthly payment amount. They can even waive the other fees that you would normally have to pay. The best thing with this plan, just like debt consolidation, you will only have to make one payment. The agency will be the one to distribute the amount to your creditors accordingly, sparing you of the hassles that come with paying your creditors individually.

FAQs

What are the types of loans that you may incorporate in the debt snowball strategy?

Using a strategy to pay off debt is a smart move. However, it is also important to determine what type of loan you are signing up a loan contract with before you apply a strategy on paying it up. Below are the types of loans where you can apply the Debt Snowball strategy.

1. Consumer Loans

When a consumer receives it from the creditor, it’s a consumer loan. The creditors mostly provide a lump sum to the consumer, who will pay it back in the form of an installment contract. In this case, you may sign an installment contract. Below are the common loans that consumers get.

Student loans – Student loans intend to finance the post-secondary education of the students, which may cover fees, such as tuition, books and supplies, and living expenses, giving everyone in any financial status access to proper education. If you are a student who aspires to hold a degree but cannot afford to pay, consider getting this type of loan.

Personal loans – Of all the consumer loan types, a personal loan is the most common one and you may easily avail. Intended for vacations, daily personal expenses, etc., personal loans usually have a term length of 10 years or below, with an amount of up to $100,000. This type of loan is so versatile that you can also use it to pay up existing loans by utilizing it as a Debt Consolidation Method.

Auto loans – Owning a car has become a norm for every American household, but you cannot own one if you don’t have a big amount of cash. You can either save up to buy one or get an auto loan.

2. Small Business Loans

A small business loan(SBL) is a type of loan that intends to help businesses/entrepreneurs achieve their business goals, making it an essential item in a business continuity plan. Some of the common types of small business loans that you may avail are as follows:

Small Business Line of Credit – A small business line of credit allows you, as a businessman, to borrow money to fund your business. Similar to a regular credit card, in this type of loan, you only have to pay the interest of the money you borrow.

Account Receivable Financing – If you intend to meet cash needs, Account Receivable Financing is a type of loan that you can resort to. Also called factoring, it works by selling your business’ accounts receivable to a third-party company.

Working Capital Loans – Working capital loan is another type of loan that you can get as a business owner to obtain short term finance for your business operations.

How do you stay motivated in implementing the Debt Snowball Method?

The Debt Snowball Method is designed in a way that we, as consumers, will stay motivated in paying off our debts, but if we don’t use it wisely, we may not achieve what we are aiming for. As we have mentioned earlier, Debt Snowball Strategy is effective due to its psychological effects. Therefore, to achieve the goals of this method, it is empirical that you regularly check and use a Debt Snowball Tracker. By doing it, you’ll get yourself constantly reminded of what you are aiming for and keep track of your progress.

While it is advisable to pay off debts as soon as possible, which is the main purpose of the Debt Snowball Strategy, it is important to tackle the most urgent first. Pay off all your non-mortgage loans and build your emergency fund before considering paying off the rest of the items of your priority list, such as the mortgages.

Can we include mortgages in the Debt Snowball Strategy?

There are several strategies and ways that you can choose from in becoming debt-free. That said, it is important to determine which one fits your needs. In this article, we have provided the guidelines that you can use, which is one step towards becoming debt-free. Additionally, you can further your learning about becoming debt-free by doing proper family budgeting.