18+ Sample Weekly Budgets

-

Weekly Budget Form

download now -

Weekly Expense Budget

download now -

Weekly Time Budget Template

download now -

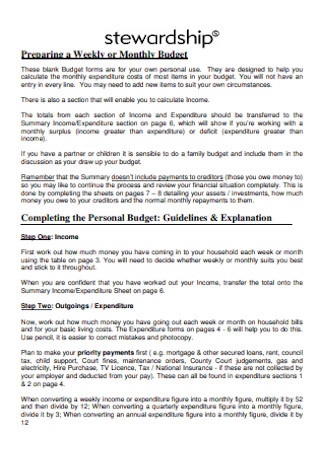

Weekly and Personal Budget

download now -

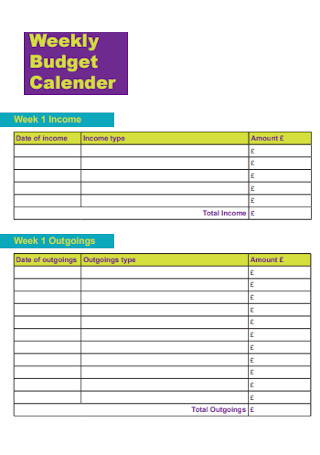

Weekly Budget Calebdar Template

download now -

Simple Weekly Budget Template

download now -

Weekly Budget Planner Template

download now -

Simple Bi-Weekly Budget Template

download now -

Student Weekly Budget Template

download now -

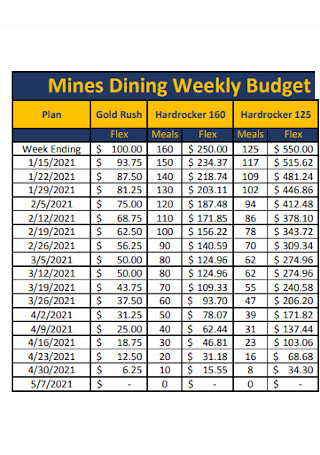

Mines Dining Weekly Budget

download now -

Sample Weekly Budget Form

download now -

Weekly and Monthly Budget

download now -

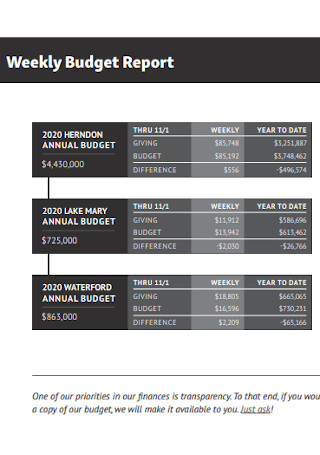

Weekly Budget Report Template

download now -

Dining Dollar Weekly Budget

download now -

Sample Business Bi-Weekly Budget

download now -

Weekly Budget Plan Template

download now -

Off-Campus Weekly Budget

download now -

My Weekly Budget Format

download now -

Weekly Budget Report Example

download now

FREE Weekly Budget s to Download

18+ Sample Weekly Budgets

What is a Weekly Budget?

Why Weekly Budget is Better than a Monthly Budget

How to Create a Weekly Budget

Checking-In with Yourself

Weekly Spend, Save, and Share

FAQs

What should a weekly budget include?

How much savings should be saved each month?

What is the difference between 50-30-20 and 70-20-10 budget rules?

What is a Weekly Budget?

Most likely than not, when you hear the word budget, the first thing that comes to mind is to spend tracking. While this is true, budgeting isn’t just about where you spend your money—it’s about understanding your spending habits and effectively allocating where your funds go.

Although this idea can be true for every budget, a weekly budget is a better option in tracking personal expenses. A weekly budget template can help you allocate your finances for a single week or a bi-week for various expenses. This is usually done before a week starts and then calculate the difference at the end of the week or even at the end of the month.

Many people budget their money based on their weekly or biweekly paycheck and weekly budget sheets are designed for that purpose. A weekly money management plan will allow one to track accounts and record their financial transactions—paying bills, transportation costs, food, and other miscellaneous expenses. By recording all of their transactions, it allows them to compare their spending to their budget. It also helps them analyze and plan for future expenses and manage their cash flows especially if they are saving up for rainy days, emergencies, or a holiday vacation.

Sticking to a weekly budget does not mean being harsh on yourself, it’s simply organizing your finances in a manner that will fit your lifestyle while giving you the leeway to reward and pamper yourself. This is just a simple step that you need to take to secure your present and future self. So, if your monthly plan isn’t working for you, creating a weekly budget is definitely worth a shot so you can manage your finances.

Why Weekly Budget is Better than a Monthly Budget

Most people prefer creating a monthly budget. But according to Dan Ariely, a behavioral economist at Duke University, people are generally bad at this whole money thing, and keeping track of your finances on a monthly basis isn’t just feasible because we do not have the attention span for it. That’s why we are all better off with a weekly budget plan instead of a monthly budget considering that a month is just too long to keep all of our financial impulses in check. Here are some of the challenges that make weekly money management a better choice than monthly household budget:

How to Create a Weekly Budget

Now that you understand what a weekly budget is, its purpose, and how it can benefit you, it’s time that you learn how to create your budget for a single week for your various expenses. Make no mistake, there are readily downloadable and printable simple weekly budget templates available for beginners online. But developing a weekly budget your own template will greatly help you in organizing your personal finances and keep you stay on track with your monthly dues.

Step 1. Know-How Much You Earn

Where to begin is not even a challenge—all you need to know is how much you earn each week after taxes and other deductions. So, it’s important that you understand that your gross salary is not the same as your net salary and it may vary depending on whether or not you will be taxed and deducted during that pay period. Other factors you need to consider aside from deductions are other additional income from overtime work, side hustles, and odd jobs. Having an idea of how much you earn every week is crucial in getting started with your weekly budget.

Step 2: Determine How Much You Are Spending

The next step is to list down all of your outgoing finances. Add up all your expenses and ensure that you factor in everything that you pay for each month. These will be your fixed expenses such as bills, mortgage payments, car repayments, payment for loans, etc. After that, take a look at your variable expenses such as your electricity bills, transportation costs, gas or petrol, food, and groceries, among others.

Step 3: Classify Your Outgoings into Mandatory and Lifestyle

Once you have identified your fixed and variable expenses, then it’s time to identify the difference between mandatory outgoings (e.g., your rent, phone, and internet bills) and your general lifestyle expenses. Your lifestyle expenses may include clothes that you buy, your daily morning coffee, or even the once-a-month movie-and-dinner-date-night. Add all these up (make sure to round up and err on the side of caution) so that you get a good idea of your spending habits in a week or a month. Review all your transactions in your spending account to see if where you’re spending your money and if you’re spending them as allocated. This will also refresh your memory of the forgotten direct debits that you made.

Step 4: Separate Outgoings from Income and Find Ways where to Cut Spending

So you can understand how much you will be able to budget, you should subtract your total outgoing from your net income. Ideally, your outgoing should be less than 75% of your earnings so you will have a room where you can set aside for your savings or sharing.

However, if you find that your outgoings are more than 75% of your total earnings, then it’s time for you to cut back from your general lifestyle. Since you already have all of your costs spending right in front of you, you can take a closer look at it and see which activities you can do without. This should give you an idea of how much room you have left to play around with. Doing this will help you save a little healthier.

Step 5: Think About Your Future

Now that you have an idea about your spending habits and where you can make cutbacks, it’s now time to look at the bigger picture and think about your broader financial goals. Whether you want to start saving for big-ticket purchases such as your own home, getting a brand-new car, or going on a trip of a lifetime, these goals are what will help drive your desire to set aside your hard-earned money. To help you commit to saving and make you feel that your goals are tangible, write them down. It would also help you reach your savings goals if you treat it like a mandatory expense. Set aside a dedicated amount to save as you would for your rent or electricity.

Step 6: Set a Reward System for Short-Term, Achievable Goals

The goal of saving is to help you prepare for the future and live comfortably. There is no use in saving up all of your money if you’re not allowing yourself to enjoy small things in life. You can look for smaller goals that you can achieve with the extra money that is not accounted for in your fixed or variable outgoings. This extra money can be saved over the course of few weeks to help you purchase a nice jacket in time for winter or attend the concert of your favorite band. The goal here is to reward yourself with things that you will enjoy so you don’t feel deprived and enslaved to your savings.

Checking-In with Yourself

Sometimes, saving can feel like a chore and pointless, especially if it takes too long to achieve your bigger goals. Here’s a tip—schedule check-ins with yourself. The best way to keep yourself on track is with your savings goals. You have to ensure that you set up a little check-in to see where you are, monitor the progress you’ve made, and how near or far you are from your goals. These small check-ins will help you see objectively and assess how much you still need to do to succeed.

Weekly Spend, Save, and Share

If you are familiar with 70-20-10 or 50-30-20, chances are, you’ve stumbled upon them in your journey to budgeting. While most people have their own system of budgeting, many follow either of the percentage breakdowns while budgeting and adhere to the idea that money can only be spent, saved, and shared. Understanding this concept gives you the opportunity to understand real budgeting and be on your way to becoming financially stable.

Spending. It’s so easy to spend money and it’s even the easiest to do among the three. It can be as simple as buying your favorite drink at the convenience store to taking out a twenty-year mortgage for your first home. Paying for your student loans or purchasing your groceries are also considered as spending.

Saving. It can be as elaborate as a certificate of deposit laddering, a mix of investing and traditional banks, or your 401k, but these are all still considered as saving money. As long as you set aside a portion of your funds for the future, that shows that you are saving.

Sharing. Your money can be shared in a fundraiser like putting some change in firefighter’s boots during their fundraising activity, tithing to your religious organization, or pledging to give a small amount to a charitable organization. It can come directly out of pocket like the street fundraising or it can be automatically deducted from your checking account to honor your commitment—either way, you are sharing your money.

FAQs

What should a weekly budget include?

Your weekly budget should include a list of fixed expenses such as rent, mortgage, insurance, and loan payments. Variable expenses like electric bills, groceries, food, and transportation must be included as well. To make your budget more effective, you should also set aside a fixed amount for your savings goals.

How much savings should be saved each month?

The most popular rule in saving is to save 20% of your income. It should be set aside for mandatory savings. the other percentages are set aside for fixed and variable expenses.

What is the difference between 50-30-20 and 70-20-10 budget rules?

For starters, these are not set in stone—these are merely budget systems that you may follow. The 50-30-20 rule means that 50% of your income is allocated to your fixed expenses, 30% of it is for discretionary spending, and the remaining 20% is for your savings. The 70-20-10 rule indicates that 70% of your income goes to fixed and variable expenses, 20% is allocated for savings, and the remaining 10% is for tithing or sharing.

A weekly budget plan is a tracker for every dollar that you have. In theory, it is easy to do but its practice is not a walk in the park. However, it represents your road towards financial independence and a quality life with significantly lesser stress. Having a weekly budget is an important factor in taking control of and mastering your personal finances. It makes more sense for either a single person or for a family to create a budget that can help them manage their money well.