34+ Sample Budget Calculators

-

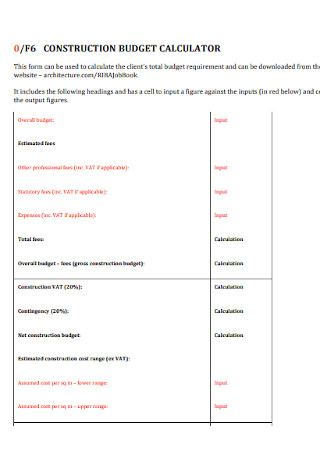

Construction Budget Calculator

download now -

Travel Budget Calculator

download now -

Recruiting Budget Calculator

download now -

Wage Budget Calculator

download now -

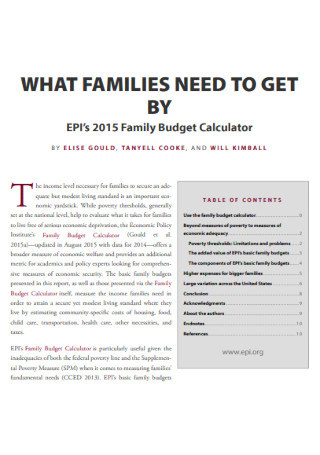

Family Budget Calculator

download now -

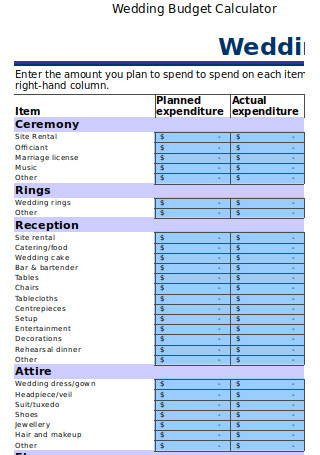

Wedding Budget Calculator

download now -

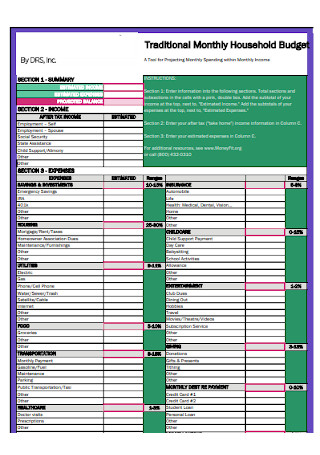

Monthly Household Budget Calculator

download now -

Sediment Budget Calculator

download now -

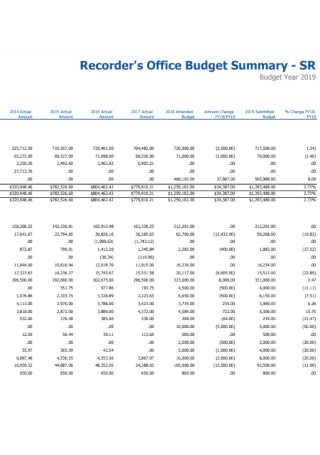

Office Budget Calculator

download now -

Budget Calculator Format

download now -

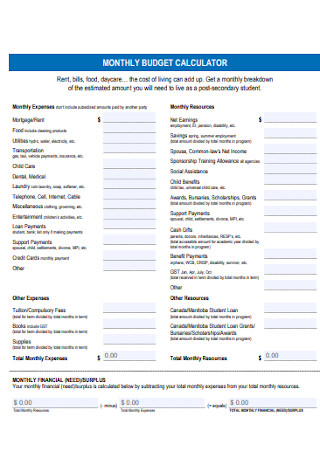

Monthly Budget Calculator

download now -

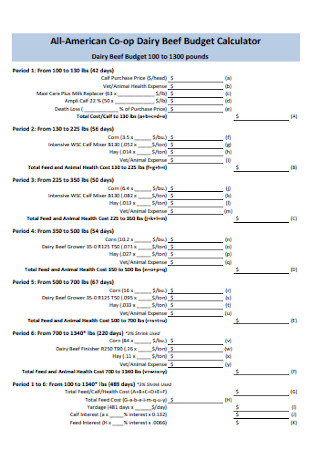

Dairy Beef Budget Calculator

download now -

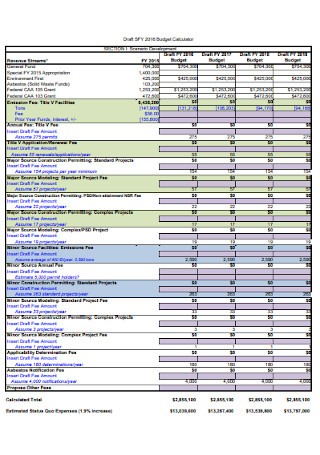

Budget Development Calculator

download now -

Board Office Budget Calculator

download now -

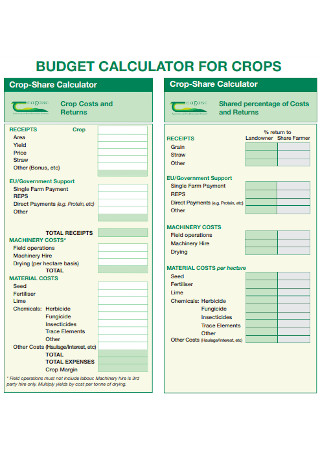

Budget Calculator for Crops

download now -

Program Budget Calculator

download now -

Landscape Water Budget Calculation

download now -

Nitrogen Budget Calculator

download now -

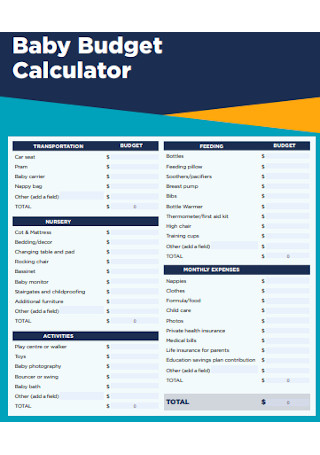

Baby Budget Calculator

download now -

Basic Budget Calculator

download now -

Outdoor Water Budget Calculation

download now -

Clinic Budget Calculator

download now -

Program Budget Calculator Form

download now -

Client Budget Calculator

download now -

Enterprise Budget Calculator

download now -

Borehole Heat Budget Calculator

download now -

Simple Budget Calculator

download now -

Commercial Power Budget Calculator

download now -

Family Budget Calculator

download now -

Town Construction Budget Calculator

download now -

Standard Budget calculator

download now -

Project Budget Calculator

download now -

Project Budget Calculator

download now -

Library Budget Calculator

download now

FREE Budget Calculators s to Download

34+ Sample Budget Calculators

What is a Budget Calculator?

Benefits of Using Budget Calculator

Key Components of a Budget Calculation

How to Create a Budget Plan

FAQs

What is the definition of a high-level budget?

How is level money defined?

Why is banking such a bad profession?

What are your financial objectives?

What is a Budget Calculator?

For generations, the federal poverty line has been used to determine whether a family’s income is sufficient to meet its basic needs. Despite this, most experts now agree that an income below the “poverty line” is insufficient to support most working families. “Basic family budgets,” which are customized for specific communities and family types, provide an accurate estimate of the funds required to maintain a safe and adequate but basic standard of living. The Family Budget Calculator can assist you in determining the amount of money needed to make ends meet in various types of households. However, it’s critical to remember that a total family budget is just that fundamental. It does not include the costs of feeding, sheltering, and clothing for a family, nor does it have the cost of transportation to and from work and school. As a result, no savings, no restaurant meals, no emergency cash, and even no renters’ insurance to protect against fire, flood, or theft are available.

Benefits of Using Budget Calculator

It all comes down to thoughtful planning when it comes to money management. If you don’t know how much of your money is ‘disposable income,’ it’s easy to let your spending spiral out of control. The main advantage of using a budget calculator is that you will realize the benefits of saving more and spending less if you use it regularly. Alternatively, you can use a budget calculator to evaluate how extravagant your spending habits are and how ineffective your personal savings campaign is to get a sense of the shock value. Then, you can begin the steps to rebalance your home budget and save more money in the long run at that low point. Creating a budget to help you save on your finances has a slew of benefits. Here are a few examples:

1. Provides you with financial control.

Knowing you have a solid monthly budget to fall back on will offer you the confidence and peace of mind that you’re in charge of your finances. It’s preferable to the spend and hope’ strategy, in which you ignore your bank balance and hope there’s money left in your account when it’s time to pay.

2. Assists you in focusing on your financial objectives.

Planning for the future and working toward a goal allows you to make large purchases, such as houses and cars, without fear of falling short. In addition, following your budget and setting away money will help you get closer to your financial goals. According to statistics, 95% of millennials save more than the suggested amount, 69% of households have less than $1,000 in emergency savings, and 34% of all Americans have no emergency savings at all.

3. Maintains awareness of your spending.

You’ll be thrilled at how much money you spend on necessities such as bills, rent/mortgage, and food. However, by disregarding how much we spend on other products like TV licenses and commuting, most of us will have significantly underestimated our monthly or weekly spending. Laying out all of your expenses will assist you in better planning and identifying areas where you may be able to save money. For example, you can save money by changing your mobile phone contract or switching to a more affordable electricity tariff with a new energy provider.

4. It’s simpler to keep track of your savings and debts.

We’ve already established that the family budget planner assists you in keeping track of your expenditures, but what about the money you save or use to pay off debts? A healthy budget will keep you informed about when your bills will be paid off and when you will have extra money to put into savings or spend on a particular pleasure.

5. Assists you in putting money aside for unexpected expenses.

It’s always great to be ready for the unexpected. But, for example, if your boiler breaks down in the middle of the winter or your oven breaks down, make sure you have some money set aside to deal with the situation. Ensuring that you have a fund of funds to fall back on when you need it the most, careful planning can help take the sting out of unexpected costs.

Key Components of a Budget Calculation

The sections below provide an essential foundation for organizing your costs and determining what amounts are fair for you in each category. Everyone’s finances are unique, and this calculator is meant to assist you; thus, use it in the way that makes the most function for you.

How to Create a Budget Plan

Start with these six steps to make a personal budget spreadsheet or learn more about money management. Even if you don’t use a budget spreadsheet, you’ll need a way to keep track of where your money goes each month. Using a template to create a budget might help you gain control over your finances and save money for your goals. The key is to find a method of keeping track of your finances that works for you. Here are some steps on how to budget with the help of a budget calculator.

Step 1. Take note of your net income.

Developing a budget determines the amount of money you have coming in. Bear in mind that if you consider your total payment as the amount of money you have to spend, it’s easy to overestimate what you can afford. Your budget should be based on your net income, which is your ultimate take-home pay. We’ve compiled some recommendations for dealing with unpredictable income as a freelancer or part-time worker.

Step 2. Keep track of your spending.

It’s important to categorize your expenditures so you can see where you can cut back. This can help you figure out where you spend the most money and save the most money. To begin, make a list of all of your fixed expenses. These are monthly bills such as rent or mortgage payments, utility bills, or car payments. Although it’s unlikely that you’ll be able to eliminate these, knowing how much of your monthly money they consume can be helpful. Next, make a note of all your variable expenses, such as groceries, petrol, and entertainment, which can fluctuate from month to month. Again, this is an area where you might be able to save money. Credit cards and bank statements are fantastic places to start because they itemize and categorize your monthly expenses.

Step 3. Decide on your goals.

Make a list of all the financial goals you want to achieve in the short and long term before you start sorting through the data you’ve collected. Short-term goals should be completed in less than a year. Long-term goals, such as retirement savings or your child’s education, might take years to achieve. Remember that your objectives don’t have to be carved in stone, but determining your priorities before building a budget will assist you.

Step 4. Make a strategy.

Use the list of variable and fixed expenses to estimate how much you’ll spend in the following months. You can determine how much money you’ll need to budget based on your fixed payments. When attempting to forecast your variable expenses, use your previous spending habits as a guide. You could further divide your costs into necessities and desires.

Step 5. Make necessary adjustments to your habits.

After you’ve completed all of this, you’ll have everything you need to finish your budget. Adjust the numbers you’ve been tracking to discover how much money you can save. Next, evaluate your spending on necessities if you’ve previously altered your spending on desires. For example, you may require internet access at home, but do you need the quickest connection available? Finally, if the figures still don’t match up, consider altering your fixed expenses. Such selections entail significant trade-offs, so carefully consider your options.

Step 6. Continue to track your budget.

It’s crucial to examine your budget frequently to ensure that you’re on track. From time to time, track your budget by following the methods outlined above. You can also compare your monthly expenses to those of folks who have similar spending habits as you.

FAQs

What is the definition of a high-level budget?

The bottom line proposal for project finance in your pitch deck is your high-level project list budget. Following the approval of your financing request, you will assemble your project team and create a firm project cost sheet estimate.

How is level money defined?

Level members can analyze cash flow by automatically detecting revenue and fixed expenses rather than classifying transactions and checking bank balances from the related bank accounts.

Why is banking such a bad profession?

Working in a bank has several drawbacks, one of which is that serving the public may be quite stressful. Most individuals are sensitive about money, and if the transaction is not proper or handled perfectly to their satisfaction, consumers can be rather unpleasant and upset.

What are your financial objectives?

Financial goals are the long-term objectives you set for yourself in terms of how you’ll save and spend money. It can be goals you want to reach shortly or in the future. In either case, identifying your objectives ahead of time makes it much easier to achieve them.

Many people underestimate the benefits of having a budget because they fear it will constrain them excessively. Bear in mind that you are in control of your budget, not vice versa. It enables you to reclaim control of your financial situation and live a more fulfilled life. Isn’t it past time for you to demonstrate your commitment by putting your money where your mouth is? Your monthly household budget can assist you in determining the best course of action.