50+ SAMPLE Startup Checklist

-

Start-up Checklist

download now -

Small Business Startup Checklist

download now -

Sample Startup Checklist

download now -

Business Start-up Checklist

download now -

The Startup Checklist

download now -

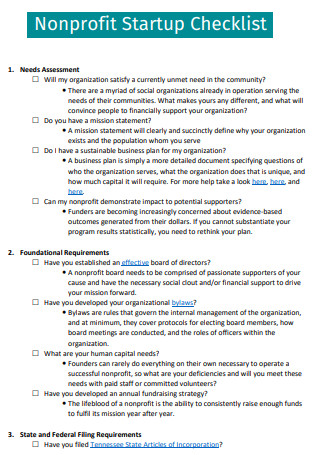

Nonprofit Start-up Checklist

download now -

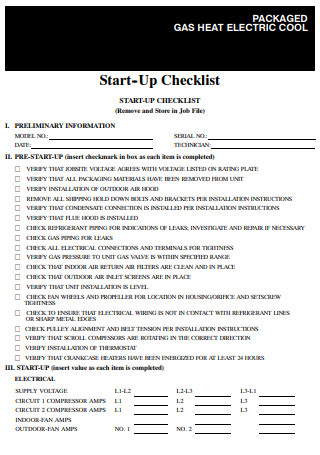

Gas Electric Startup Checklist

download now -

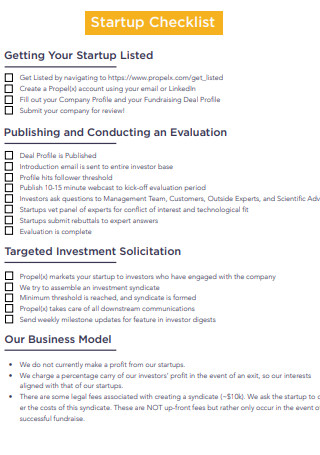

Startup Funding Checklist

download now -

Startup Legal Checklist

download now -

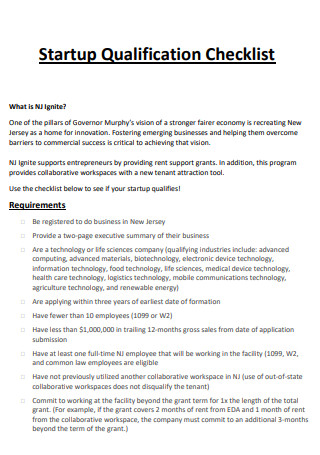

Start-up Qualification Checklist

download now -

Pre Startup Checklist

download now -

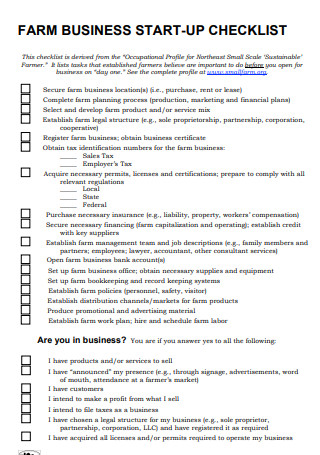

Farm Business Startup Checklist

download now -

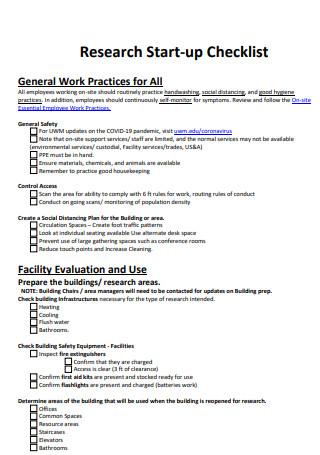

Research Start up Safety Checklist

download now -

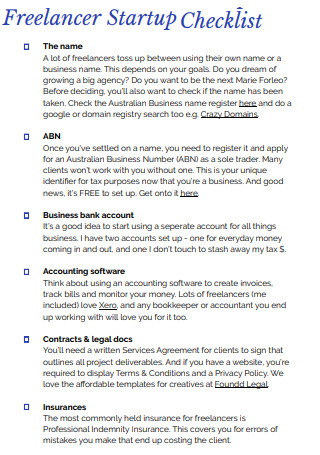

Freelancer Start-up Checklist

download now -

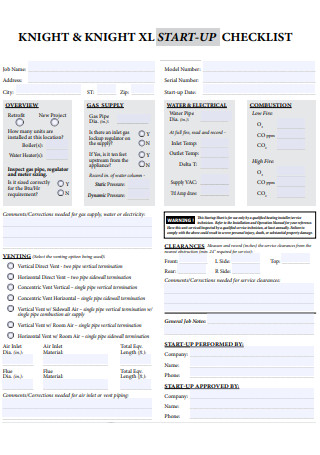

Knight Startup Checklist

download now -

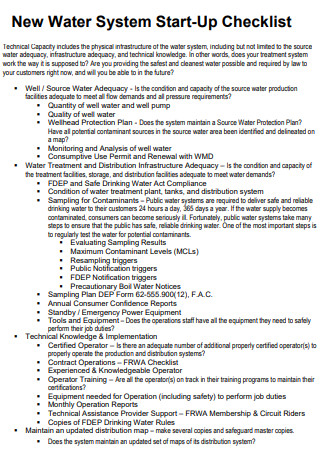

New Water System Startup Checklist

download now -

Simple Start-up Checklist

download now -

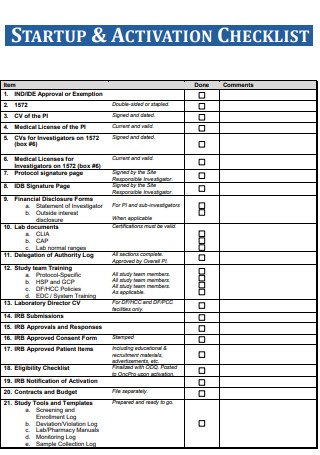

Start-up and Activation Checklist

download now -

Telehealth Startup Checklist

download now -

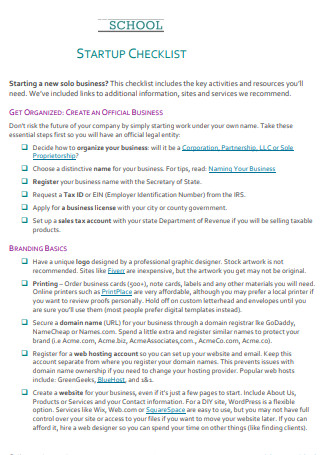

School Startup Checklist

download now -

Fund Startup Checklist

download now -

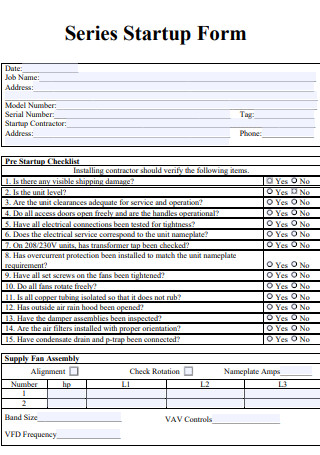

Series Startup Checklist

download now -

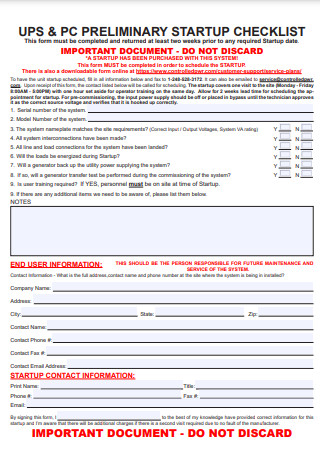

Preliminary Startup Checklist

download now -

Start-up Competition Submission Checklist

download now -

Seasonal Start-up Checklist

download now -

Remote Desktop Manager Startup Checklist

download now -

Installation Start-up Checklist

download now -

Small Food Business Startup Checklist

download now -

Boiler Pre Startup Checklist

download now -

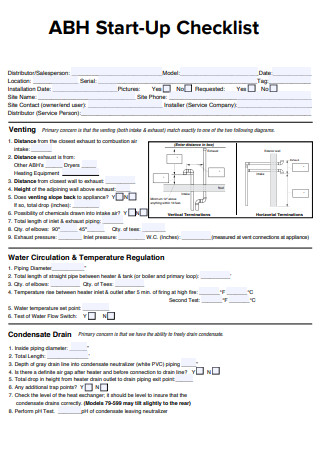

ABH Startup Checklist

download now -

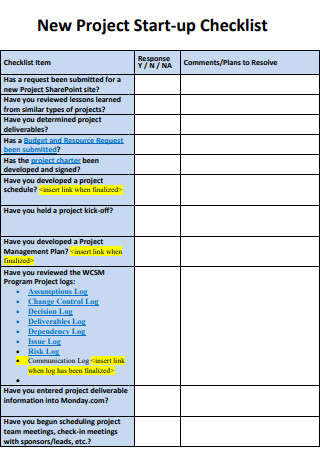

New Project Start-up Checklist

download now -

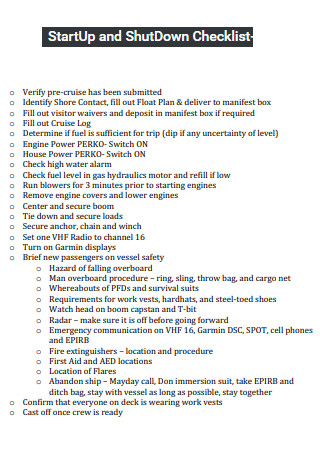

StartUp and ShutDown Checklist

download now -

Creative Start-up Checklist

download now -

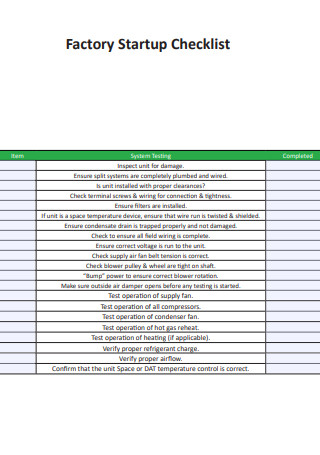

Factory Start-up Checklist

download now -

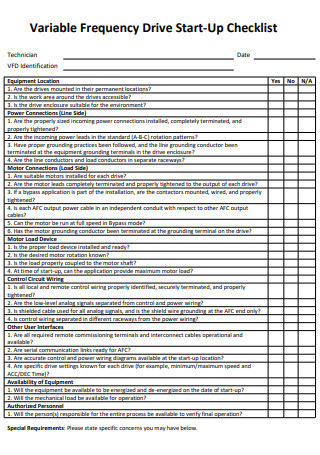

Variable Frequency Drive Startup Checklist

download now -

New Faculty Startup Checklist

download now -

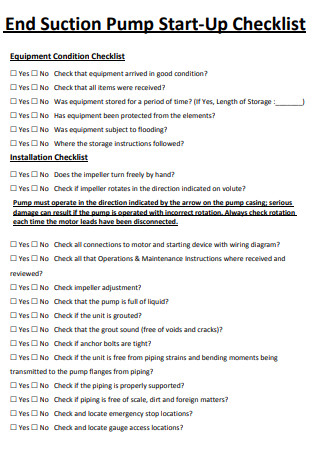

End Suction Pump Start-up Checklist

download now -

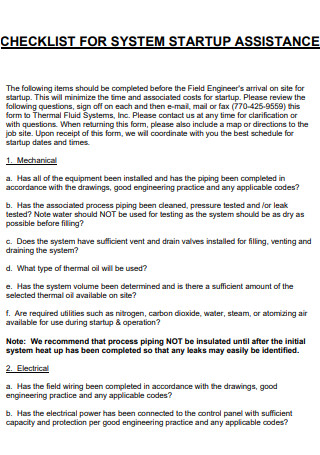

System Startup Assistance Checklist

download now -

Jobsite Start-Up Checklist

download now -

Troop Start-Up Checklist

download now -

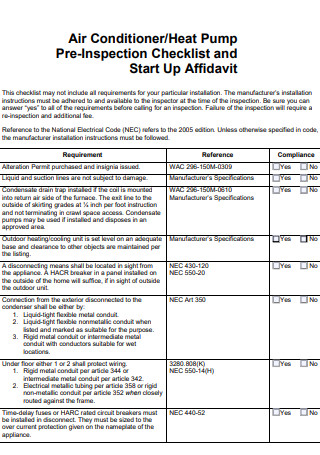

Start-Up Pre-Inspection Checklist

download now -

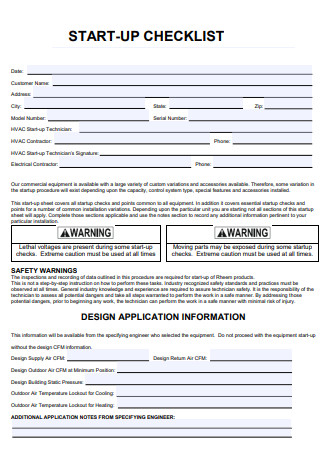

Start-Up Checklist Example

download now -

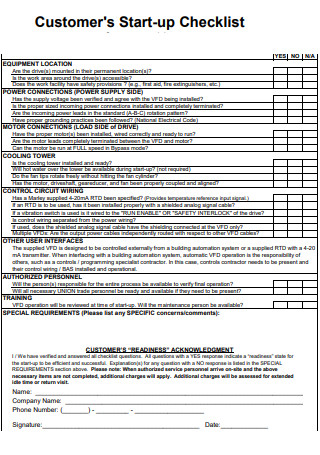

Customers Start-Up Checklist

download now -

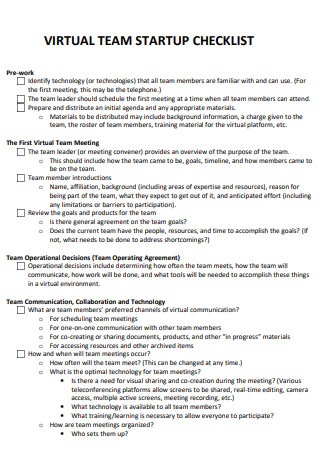

Virtual Team Start-Up Checklist

download now -

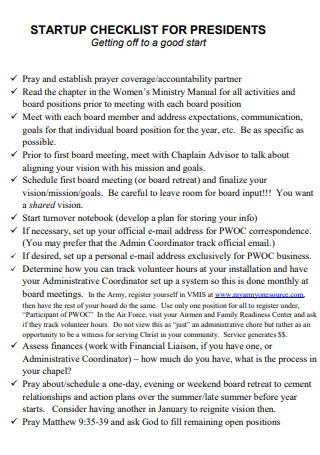

Start-Up Checklist for Presidents

download now -

Foundation Start-Up Checklist

download now -

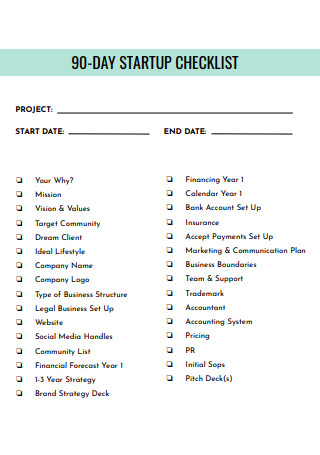

90-Day Start Up Checklist

download now -

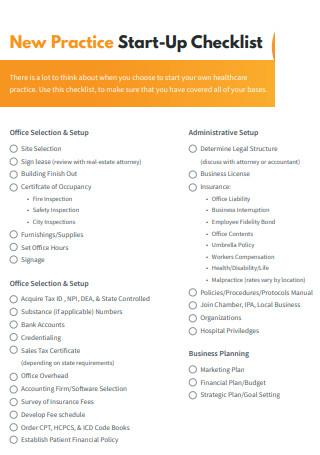

New Practice Start-Up Checklist

download now -

Job Start-Up Checklist

download now -

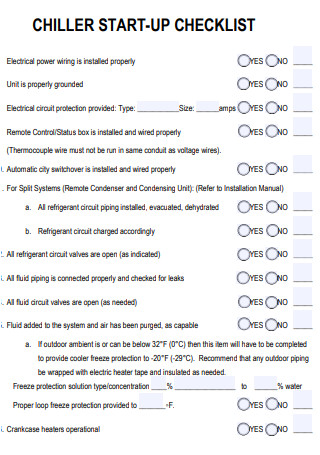

Chiller Start-Up Checklist

download now -

Laboratory Start Up Checklist

download now

FREE Startup Checklist s to Download

50+ SAMPLE Startup Checklist

a Start Up Checklist?

Benefits of Having a Business

Tips In Starting A Business To Help You Succeed

How to Effectively Establish and Launch Your Business

FAQs

Why do startups fail?

Why are companies so difficult to launch?

How difficult is it to run a startup?

What Is a Start Up Checklist?

If you want to create a business, you must be accountable for everything you do. A single error in the procedures you will follow can have a detrimental effect on other business processes. For instance, failing to develop a cost estimate for the supplies required for operations can cause delays in dealing with suppliers and, potentially, starting the establishment. According to statistics, just 25% of new enterprises survive for 15 years or more.

Benefits of Having a Business

Choosing to establish your own business requires a significant leap of faith. It entails stepping outside one’s comfort zone and attempting something new. Why wait if that concept fascinates you? You’re prepared to take the plunge and establish your own company. It requires considerable effort and involves some danger, but the potential returns are enormous. If you’re still not persuaded, here are five compelling reasons to start your own business.

Tips In Starting A Business To Help You Succeed

To be prosperous in business today, you must be adaptable and possess vital planning and organizing abilities. Many people start a business with the anticipation of turning on their computers or opening their doors and immediately earning money, only to discover that making money in a business is significantly more complex than anticipated. You may avoid this in your business operations by taking your time and carefully arranging all of the procedures necessary to succeed. Whatever type of business you desire to begin, the following six tips can assist you in being successful.

-

1. Idea Screening

You do not get an idea and instantly start building a product around it. While it is true that unique ideas are the bedrock of business success, it is insufficient for the brilliance to be limited to your imagination. As a result, it is critical to examine the feasibility of an idea before moving forward with specific action. As fascinating as your concept may be, it must solve real problems or meet existing market needs. If it falls short of both, you’re unlikely to succeed if you pursue it. Before you become obsessed with your concept, you’ll want to determine whether it’s realistic to follow. You must ask probing questions and provide candid responses. After some deliberation, you should provide concise answers to those questions. If you cannot do so, your idea is unlikely to be viable as a startup. Commit resources to your project only when demonstrated to be possible.

2. Market Research

According to research, 35% of firms fail due to a lack of market need. That is the type of error you want to avoid while launching your product. Before even beginning to construct the product, it is critical to guarantee optimal product/market fit. As a result, you’ll need to perform thorough market research to understand your target audience and competition. This knowledge enables you to mitigate risks associated with the product’s debut. Market research positions you strategically when it comes to selling the goods.

3. User Research

The success of your product is contingent upon its users. If people do not perceive value in your items, all of your efforts will be in vain. As a result, it’s critical to undertake user research during the product’s development to verify that it’s aligned with the user’s needs. By incorporating user research into the development strategy, you can ensure that you receive input early in the process. Any teething difficulties can be discovered and resolved inexpensively. By doing regular face-to-face meetings and conversations with users, you can determine whether the product is developing in the right direction. Before launching your product, you must demonstrate that it can resolve user concerns.

4. Team Recruitment

There is a limitation to how great you can take on as a startup founder. Eventually, you’re going to need a team if you want to avoid becoming overwhelmed by an ever-growing to-do list. Of course, building a team of experienced professionals from scratch is difficult, given that most founders operate on a shoestring budget. If you cannot hire a crew, consider outsourcing some jobs or bringing on a co-founder. Outsourcing enables you to manage expenses more effectively. Meanwhile, a co-founder alleviates a significant amount of burden from your shoulders, particularly if they possess complementary skill sets. When you’re ready to scale, hire the proper specialists to fill the gaps in your startup’s various departments.

5. Strategy Development

Once you’ve defined the product clearly, you’ll need plans for developing, delivering, and marketing it to the intended audience. Without good methods, you’ll be vulnerable to a variety of issues that could jeopardize your startup ambitions. For startups, a critical component of success in developing effective sales and marketing strategies. It will help if you plan how you will communicate with your audience. Is social media marketing the most effective strategy? Or should you pursue a long-term SEO strategy? By planning your steps, you can recognize opportunities and threats.

6. Secure Funding

Cash is the lifeblood of any business, and according to CB Insights, it is the leading cause of startup failure. As a result, one of your primary responsibilities as a founder is to get sufficient finance and maintain a proper cash flow for the firm. Even if you believe you are self-sufficient, you should always look for financial opportunities. Having a substantial war chest increases your chances of surviving when times get tough.

How to Effectively Establish and Launch Your Business

We’ve designed a comprehensive company startup checklist to save you time and effort. Check it out to ensure you understand what you need to do to efficiently build and launch your business.

-

1. Enhance Your Business Concept

After you’ve developed a business concept, it’s essential to sit down and conduct market research. Attempt to understand what your competitors are doing and what works for them. Additionally, it will help determine what differentiates you from your competition in your niche. This activity is critical in determining your true competitive edge. Additionally, it will help to comprehend why you are starting a firm. This could meet a personal need or address a commercial gap. Whatever it is, it is critical to be crystal clear about your objective. Consider your target market in light of your concept. Who are these individuals? Make as many notes on them as possible, including their age, gender, and location.

2. Evaluate Your Economic Situation

Whatever type of business you choose to establish, you will require good business financing to get it off the ground. Make a quick calculation of the entire amount of money you now have and the amount you need. Determine your alternatives based on this calculation. Where will you obtain all of the necessary funds? Will you take out a loan, or will you cover all of your costs on your own? Also, it’s worth thinking about whether you’ll need to quit your employment to focus exclusively on your business. If so, do you have the funds to sustain yourself till you begin earning profits? Bear in mind that it can take several years to generate revenue. Financial decisions affecting your company have the potential to make or break it. That is why you must develop a more sustainable business plan.

3. Formalize Your Business Plan

This item on the business startup checklist is critical to entrepreneurs seeking investor finance. Before pitching your business concept, you should prepare a comprehensive business plan. Additionally, it should have a detailed section on money, the most critical investor component. Further, your strategy should include information about your target market, products, and services, as well as an overview of your firm and significant milestones.

4. Purchase Commercial Insurance

Ideally, you should purchase insurance for your firm before its starts. Even if you may not require it immediately, it’s a good idea to buy it right away. In the event of a robbery, blaze, or even lawsuit, an insurance policy can assist you in remaining financially secure. To improve your risk protection, you can purchase various types of insurance.

FAQs

Why do startups fail?

A common cause of startup failure is an ineffective management team. Weak management teams make numerous errors: they frequently lack strategy, creating a product that no one wants to buy because they did not conduct sufficient pre-and post-development work to validate the concepts.

Why are companies so difficult to launch?

Apart from demanding a certain amount of “stickiness” and commitment, startups are also tricky in unanticipated ways. This includes ambiguity tolerance, co-founder stress, managing diverse people, sleep deprivation, pressure from multiple angles, and loneliness.

How difficult is it to run a startup?

Starting a business is difficult, involves determination and education, and pays dividends only in the long run. Before leaping, take an honest look at yourself. Are there clients experiencing genuine agony and losing money? While customers may “enjoy” a product, they will typically pay for something they “need,” either physically or emotionally.

Do not be afraid to do so if you believe you already possess the necessary knowledge, skills, and capabilities to create your startup checklist. However, employing examples is an excellent way to write a page without efficiently expending excessive work. Make your start-up checklist now.