27+ SAMPLE Management Research Report

-

Environmental Management Independent Research Report

download now -

Water Resource Management Research Report

download now -

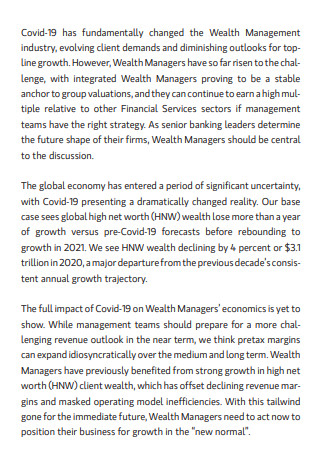

Wealth Management Research Report

download now -

Informative Management Research Report

download now -

Sample Management Research Report

download now -

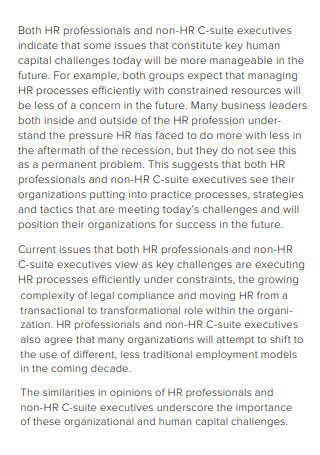

Human Resource Management Research Report

download now -

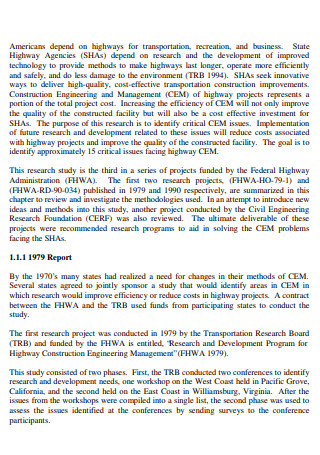

Construction Engineering and Management Research Report

download now -

Management Research Final Report

download now -

Management Reporting Research Report

download now -

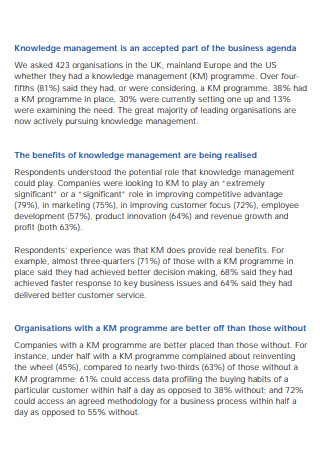

Knowledge Management Research Report

download now -

Global Data Management Research Report

download now -

Project Management Research Report

download now -

Qualitative Management Research Report

download now -

Management Research Summary Report

download now -

Data Management Research Report

download now -

Management Review Research Report

download now -

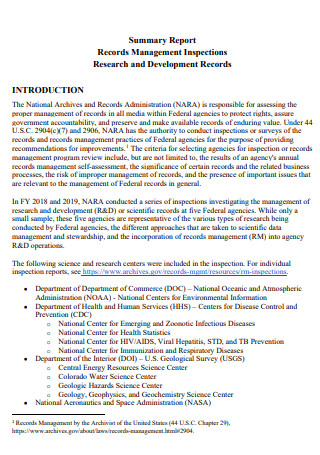

Management Inspections Research Summary Report

download now -

Strategic Management Research Report

download now -

Investment Management Research Report

download now -

Facilities Management Research Report

download now -

Innovation Management Association Research Report

download now -

Project Management Training Research Report

download now -

Database Management Research Report

download now -

Health Management Research Report

download now -

Sales Management Research Report

download now -

Trends in Data Management Research Report

download now -

Active Risk Management Research Report

download now -

Business And Management Research Income Report

download now

FREE Management Research Report s to Download

27+ SAMPLE Management Research Report

a Management Research Report?

Benefits of Conducting Research

Elements of a Management Research Report

How To Manage a Research Report

FAQs

What is the definition of a management report?

What is a management report on a monthly basis?

What role does research have in corporate management?

What Is a Management Research Report?

A Management Research Report is a document that summarizes the findings of an organization-based human resources research project and includes suggestions for action and an implementation plan for a management audience. As seen in this article, MRRs are far lengthier than the majority of reports issued in organizations. This indicates that they are expected to be the result of extensive investigation. This is also a reflection that they should be backed up by scholarly research, which is not the case with standard organizational reports. In some ways, they are a hybrid document, not strictly academic like a dissertation, and not purely practical like most standard reports. According to statistics, the Market Research industry’s market size is predicted to grow by 4.7 percent in 2021. The market size of the Market Research industry in the United States increased by an average of 0.2 percent per year.

Benefits of Conducting Research

There is always more to learn whatever career field you are in or how high you are on the corporate ladder. The same holds for your private life. Regardless of how many experiences you’ve had or how wide your social circle is, there are still things you don’t know. The research elucidates the unknown, enables you to view the world from various angles, and fosters a greater understanding. In some fields, data analysis is critical to success. It may not be necessary for others, but it provides numerous benefits. The following are ten reasons why research is needed:

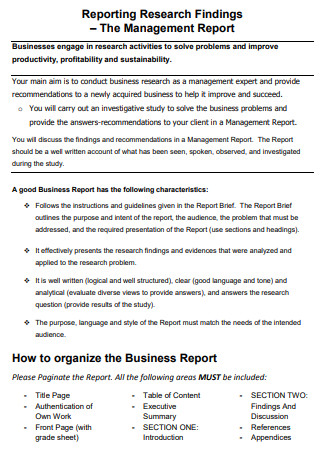

Elements of a Management Research Report

Technically, each project is unique, and you may write your report in your preferable way. However, several parts are consistent across all Management Research Reports, which I have listed below to assist you in structuring your report.

Introduction

This section should present the project’s motivation, organizational background, and academic context (a concise overview of the ‘problem’ and what is and is not known about it). Additionally, it should introduce the report’s structure.

Literature Review

This should be a comprehensive, annual evaluation of the pertinent literature in the topic of study (and relevant related literature, if appropriate). It should be based on contemporary academic research and scholarly articles rather than textbook chapters and practitioner publications.

Methodology

This section should detail the research you conducted on your issue (for example, research plan, sample size, methodology, and data analysis) and provide reasons for the actions you took or did not take in these areas.

Conclusion

This section should summarize and explain your findings from your results analysis. It should be a reasonably lengthy part that clarifies the research findings for the reader. It should do so by drawing on current literature and reflecting any constraints considered when interpreting the results, but it should also be focused and accessible to a management audience.

Recommendations

The recommendations part should have its subheading and should not be incorporated into the conclusions section. This section can be relatively brief, as the recommendations should flow naturally from the conclusions, so avoid repeating yourself. The trick is to make accurate advice understandably and straightforwardly.

Implementation Plan

This could be included in the recommendations section or as a stand-alone piece. Having a separate area works best for me because it makes it more evident for the management audience who prefer certain sections to pop off the page. It should specify what has to be done to implement each recommendation and determine who is responsible, the timeline for action, and the associated costs and benefits. Often, it is ideal for providing this information in a table format to make it more readable and concise.

Appendices and References

These should contain the necessary information to support the report but is too large to put in the main body. Additionally, a complete bibliography should be included by the company’s standard referencing system.

How To Manage a Research Report

After successfully applying for and obtaining money for your research project, it is time to set it up. You may be conducting a project for the first time and find yourself unprepared to deal with the difficulties. Establishing a project necessitates the consideration of numerous factors. This part will present five recommendations for developing a road map for the success of your research project.

Step 1: Establish a collaborative workspace.

Whether you operate in a private lab or are managing a diverse virtual project, having a central location is critical for team cohesion. The primary site for information sharing may be a bulletin board on a lab wall or a shared network drive accessible exclusively to team members actively contributing to the project. The area will serve as the primary point of contact for team updates and knowledge management. Also, the site should house the team charter, which details how you will collaborate to fulfill the project’s objectives. The team charter describes the mission, vision, and goals of the team. It can establish ground rules for communication modalities, group planning, satisfying individual and team expectations, the reporting structure, and handling deadlines.

Step 2: Develop a project management strategy.

Your grant application most likely requires you to provide a project plan. However, the assumptions upon which your initial project plan was built may no longer be valid. For instance, available resources may have changed, critical staff may have been reallocated to other projects, or the known research around your topic may have shifted. These modifications may need revisions to your initial strategy. The project plan-you submitted should be examined, and the associated resources and assumptions should be amended as necessary. The project plan outlines your objectives. The next step you should practice with the team is to map out the project’s execution. Include the tasks that must be accomplished and the time and effort required to complete them.

Step 3: Prepare to manage a budget.

Knowing when you will get financial disbursements and make expenditures will assist you in planning the project’s timeframe. Please make a list of the materials you’ll need to buy, together with a timeline for getting them and the estimated cost of each purchase. Create a list of vendors to be hired and a payment plan and budget for the contract. Be aware of any grant funding schedule contingencies, mainly if disbursements will be made according to milestones. Check the schedule of installment payments alongside your schedule of expenditures to reduce the risk of the project being delayed due to insufficient funding to complete the next task.

Step 4: Risks should be anticipated.

When developing your project management proposal, collaborate with your team to determine the potential difficulties associated with each project’s milestones. Create a plan for mitigating and avoiding each risk. During risk planning, keep in mind project accomplishments. For instance, will the team be prepared to begin the plan’s subsequent activities if a milestone is met ahead of time? Consult with other stakeholders to obtain a second opinion.

Step 5: Develop a communication strategy.

Establish expectations with stakeholders regarding the frequency with which you will communicate project updates. Concentrate the communication plan on decision-makers and those who the project’s actions and outcomes will impact. Determine how frequently you will share progress, the intervals at which you will release updates, and your communication format. Maintain a balanced presentation of information by emphasizing success hurdles and facilitators, a summary of project failures, and notable accomplishments.

FAQs

What is the definition of a management report?

Management reporting can be roughly defined as reports used by management to administer the organization, make business decisions, and track progress. Management reports assist managers in keeping an eye on the more delicate elements of their department.

What is a management report on a monthly basis?

Monthly management reports summarize and evaluate your business’s financial and operational performance on a month-to-month basis. These reports help your management team monitor your company’s historical and current performance and aid them in making sound business decisions.

What role does research have in corporate management?

Business research aids in the identification of potential possibilities and risks because it assists in identifying issues and, with this information, prudent decisions can be taken regarding how to address the problem effectively. It enables a deeper understanding of customers and hence allows more effective communication with customers or stakeholders.

Thus, I have provided you with some recommendations that I hope you will find beneficial and refer to if required to produce a management research report for your organization. However, why wait to be questioned? If you believe that a change is necessary, but no one has proposed a solution, prepare your management research report and bring it to the board. You’re almost certain to receive a promotion as a result!