41+ Sample Payment Plan Agreement Templates

-

Sample Payment Plan Agreement Template

download now -

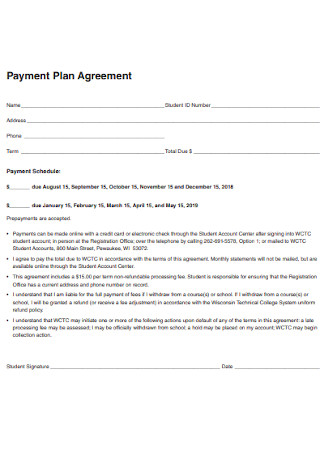

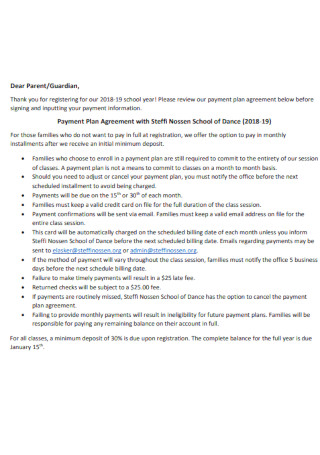

School Payment Plan Agreement

download now -

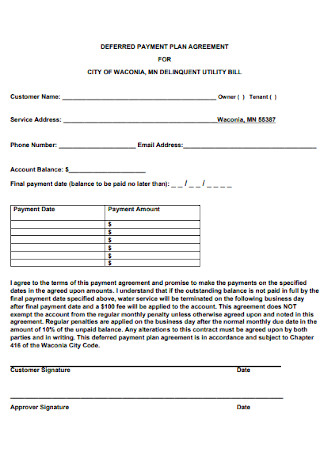

Deferred Payment Plan Agreement

download now -

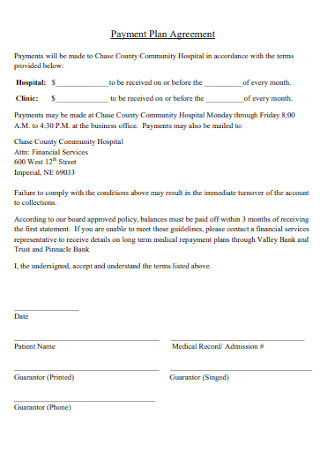

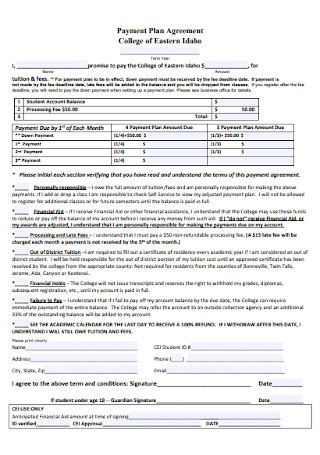

College Payment Plan Agreement

download now -

Basic Payment Plan Agreement Template

download now -

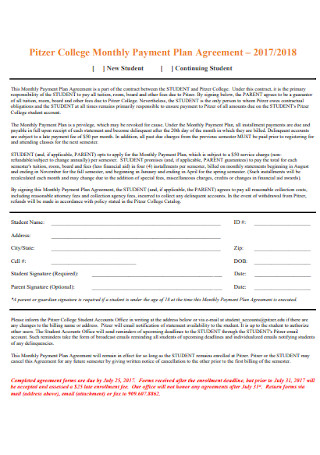

College Monthly Payment Plan Agreement

download now -

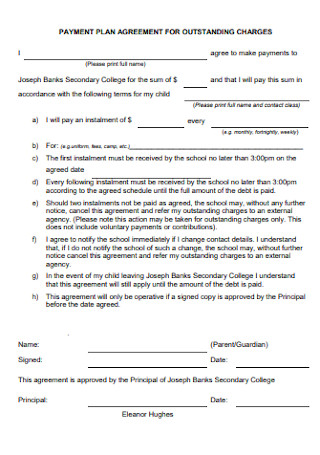

Payment Plan Agreement for Outstanding Charges

download now -

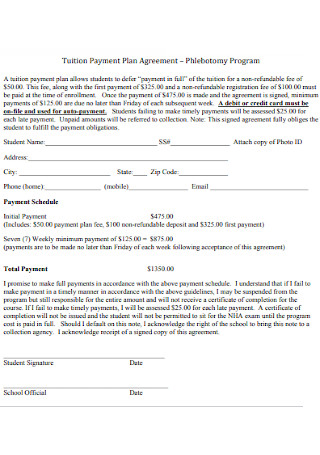

Tuition Payment Plan Agreement

download now -

Payment Plan Application And Agreement

download now -

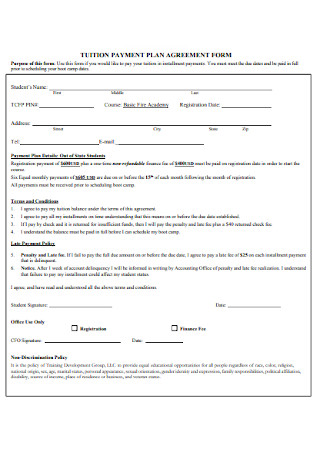

Tution Payment Plan Agreement Form

download now -

Payment Service Plan Agreement

download now -

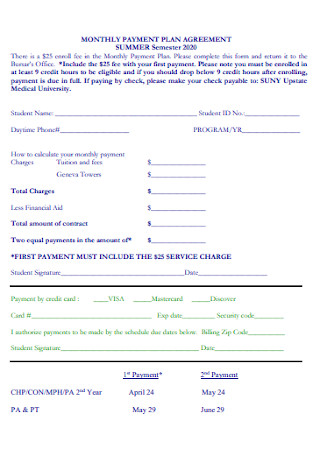

Monthly Payment Plan Agreement

download now -

Comptroller Payment Plan Agreement

download now -

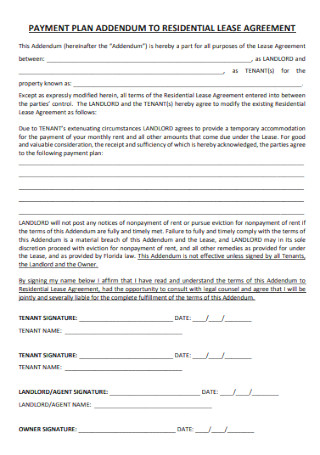

Lease Payment Plan Agreement

download now -

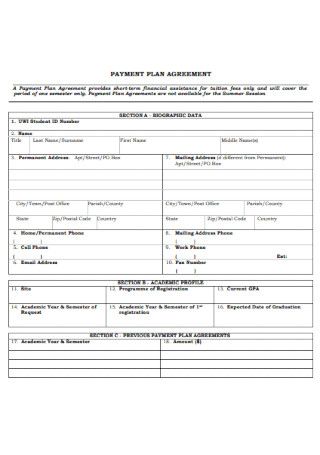

Student Payment Plan Agreement

download now -

Payment Plan Agreement for Unpaid Meals

download now -

Payment Plan Authorization Agreement

download now -

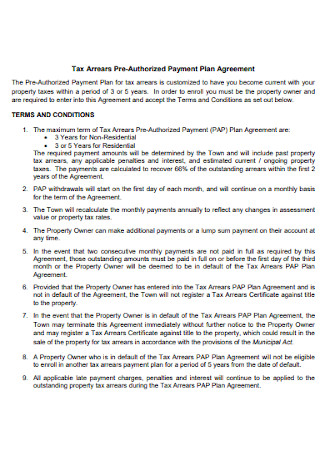

Tax Payment Plan Agreement

download now -

Payment Installment Plan Agreement

download now -

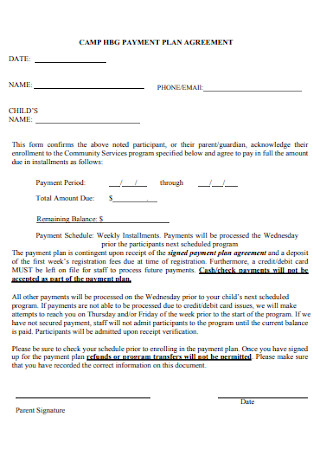

Camp Payment Plan Agreement

download now -

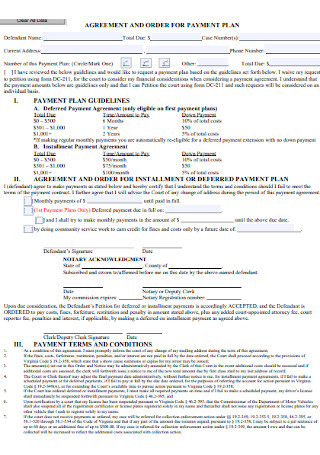

Payment Order Plan Agreement

download now -

Sample College Payment Plan Agreement

download now -

Association Dues Payment Plan Agreement

download now -

Student Housing Payment Plan Agreement

download now -

Budget Payment Plan Agreement

download now -

Auto Debit Payment Plan Agreement

download now -

Dental Payment Plan Agreement

download now -

School Payment Plan Agreement Template

download now -

Administrative Payment Plan Agreement

download now -

Payment Plan Lease Agreement

download now -

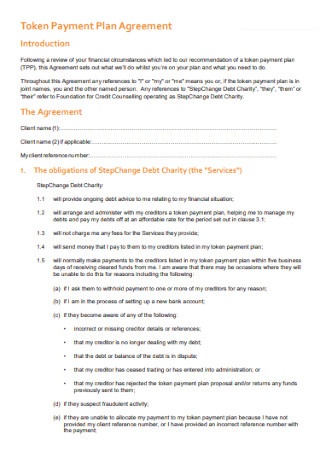

Token Payment Plan Agreement

download now -

University Payment Plan Agreement

download now -

Subscription Fee Payment Plan Agreement

download now -

Primary School Payment Plan Agreement

download now -

Post-Tenancy Payment Plan Agreement

download now -

Standard Payment Plan Agreement Template

download now -

Automatic Payment Plan Agreement

download now -

Prescription Payment Plan Agreement

download now -

Ambulance Billing Payment Plan Agreement

download now -

Certification Services Payment Plan Agreement

download now -

Payment Plan Agreement Format

download now -

Sample Student Payment Plan Agreement

download now

FREE Payment Plan Agreement s to Download

41+ Sample Payment Plan Agreement Templates

What Is a Payment Plan Agreement?

Financially Unstable No More: Budget Planning Tips

How to Craft a Payment Plan Agreement

FAQs

How does a payment plan work?

What is a flexible payment plan?

What is an acceptable credit score?

What Is a Payment Plan Agreement?

Have you experienced buying something too expensive that paying in full is hard for your current budget? Perhaps, an installment scheme that divides the payment over a specific timeframe makes the setup bearable. A payment plan is similar to that. For example, a borrower of a mortgage loan agreed to repay the debt with a lesser amount, but the collection happens in corresponding months. When the outstanding debt is fully paid in the end, the debtor gets released. Creditors and debtors form a binding contract about such a payment arrangement through a payment plan agreement. This official document outlines the plan to repay at a given timeline.

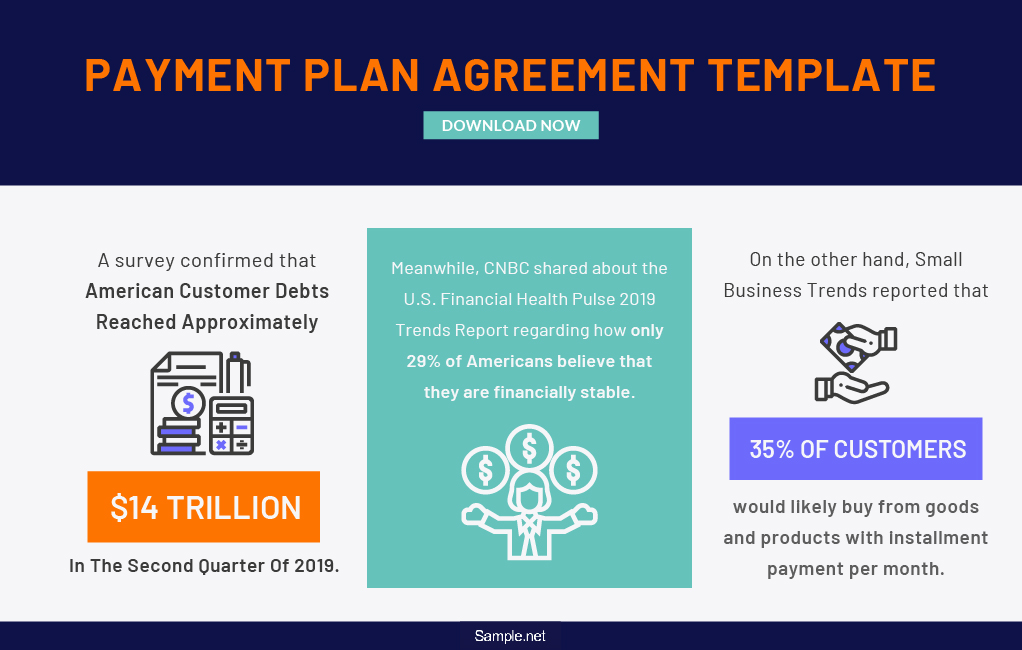

A survey confirmed that American customer debts reached approximately $14 trillion in the second quarter of 2019.

Meanwhile, CNBC shared about the U.S. Financial Health Pulse 2019 Trends Report regarding how only 29% of Americans believe that they are financially stable.

On the other hand, Small Business Trends reported that 35% of customers would likely buy from goods and products with installment payment per month.

Why Are Payment Plans Important?

Remember that purchases under a payment plan undergo an installment scheme, meaning a divided payment schedule commences. And since its agreement contains an outline of the payment amount, collection date, and related details, it sets the terms between parties. Not having a payment agreement often leads to conflicts because parties may have different ideas and applications towards such plans.

More so, a payment plan usually has little to no interest when payments come gradually. Besides the benefit of being capable of purchasing pricey products and services, most creditors use the no interest rate incentive, so a debtor gets interested in the financial plan. If ever the common interest is present, don’t worry because it will not exceed the state’s usury rate.

Financially Unstable No More: Budget Planning Tips

Shockingly, only 29% of US citizens agree that they are financially strong. Moreover, 54% are still coping, and 17% are struggling in terms of their finances. These statistics show how poor financial planning in action. Before making a payment plan agreement, be sure to master being financially stable first. This approach will save you from endless debts in the long run. Here are some budget planning tips to consider:

How to Craft a Payment Plan Agreement

Now for the main dish, how do you make a payment plan agreement? By knowing its definition, importance, and details, it will be much easier to form the deal. In fact, many people are already using these financial plans in the medical field, vehicle sale, e-commerce, or any other business. Wherever you apply this, make sure not to forget these essential steps:

Step 1: Introduce the Parties

Identify the creditor and the debtor first. Whoever is part of the agreement needs identification from their name, address, contact detail, and any ID or account number. At least this part confirms who the official parties are, in case liabilities and proof require such information. Check the spelling or any possible mistake since the wrong details may affect the form’s credibility. Also, indicate when the contract starts taking effect since it shall be followed accordingly.

Step 2: Define the Statement of Agreement

Aside from inputting the date of when to take effect, anyone who checks the document must at least recognize that it is a payment plan agreement. Write this statement as if you are writing a detailed letter. Otherwise, the form’s function may be questionable. Point out that there is a mutual agreement in the payment plan since it proves the document’s validity once signed by all parties. Furthermore, identify what the debt is or what needs to get paid. Is the debtor paying for a limited edition toy or action figure? Or maybe for serious matters like a patient paying for hospital services? Add that in the sheet.

Step 3: Specify the Payment Amount and Options

Are you done with the agreement statement and the balance’s purpose? Good, proceed with the payment method and amount. Everyone has a different preference when it comes to their payment option. Does the debtor want to pay in cash, check, credit card, digital wallet, or insurance? Do not assume that everyone chooses cash because, according to Small Business Trends, 35% of clients even prefer purchasing goods through monthly installments. Clarifying the method is essential, so creditors are aware of where to gather payments. Next, note the amount owed. How much is the total cost? And how much will be paid per month as an installment? Jot it down.

Step 4: Explain the Terms and Conditions

Not incorporating the rules, terms, and conditions shall make an agreement messy. It is nice to set what is allowed and prohibited from the deal, so parties know what to do and prevent. Adding regulations acceptable to state laws will be encouraged. Moreover, keep things fair in these rules wherein not only one side receives the advantage. While a creditor expects payment for satisfaction, he or she should also be considerate of the debtor. Maybe debtors get required to pay a substantial amount weekly, which is infeasible in their part. Thus, they might not sign the document.

Step 5: Input the Termination and Dispute Clause

Next, include what consequences will happen if debtors cannot meet their obligations? Thus, an official segment for termination, dispute, and the like is necessary. If one party fails to complete the payments, then how to handle that is worth discussing. An example is to add interest when fees are given late. Nobody wants a contract breach all of a sudden. But to prepare for such matters, expound that in the sheet.

Step 6: Require a Signature

Signatures complete the entire contract or agreement. Such marks prove that every party has read and agreed to the whole stipulations under the form. Therefore, give enough room to affix a signature for all parties. In case the payer is a minor, having the parent or guardian to sign along with them is a must. Sometimes, a representative who acts as the officer-in-charge of a particular business is crucial. With all signs complete and legible, everything is confirmed.

FAQs

How does a payment plan work?

Assume that you bought the latest iPhone model. With its high price, you could not make a one-time purchase. Hence, you choose a monthly installment option. In 24 months, for example, you pay less per month. Spreading the cost sounds advantageous, but be sure you are all right with a long period for the payment.

What is a flexible payment plan?

Payment plans considered flexible are those that work similarly to on-the-spot loans. With this, goods and services are received quickly, but you need to fulfill monthly installments. Also, flexibility is based on how terms are changeable. While most agreements are strict, others allow changes if necessary.

What is an acceptable credit score?

Generally, credit scores below 500 are poor. 580-739 scores are good. Meanwhile, those that reach 740 and up are already very good. However, the credit scoring model differs in specific applications, so there can be changes considered acceptable or bad.

A known German proverb states, “He who is quick to borrow is slow to pay.” Do not fall into that trap of having endless debts. Be financially responsible. Whether you are the creditor or the debtor, make sure you are protected by proposing a well-thought-out payment plan agreement.