20+ SAMPLE Budget Report

-

Budget Report Template

download now -

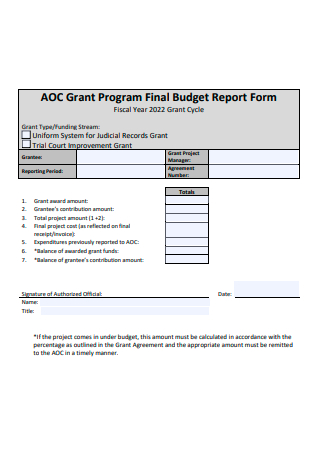

Grant Program Final Budget Report Form

download now -

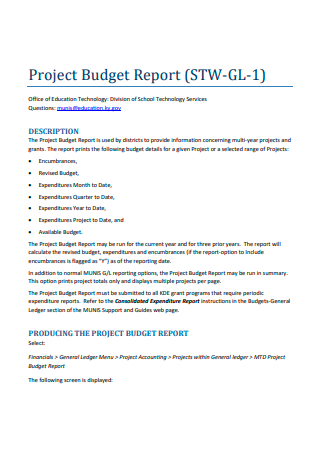

Project Budget Report

download now -

Community College Certified Budget Report

download now -

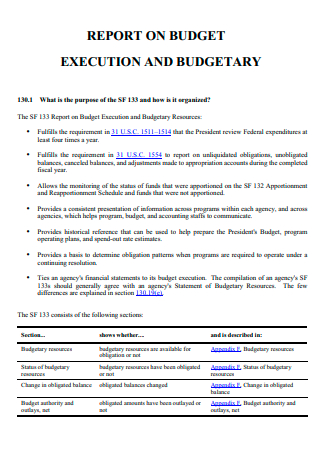

Budget Execution and Budgetary Report

download now -

Six Month Budget Status Report

download now -

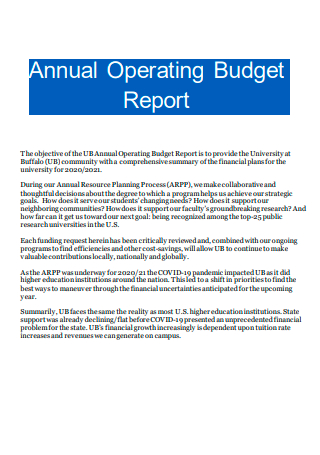

Annual Operating Budget Report

download now -

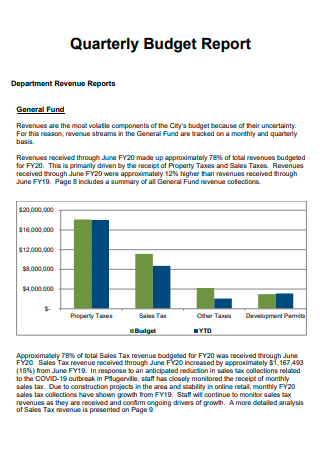

Quarterly Budget Report

download now -

Basic Budget Report

download now -

Contract Expense and Budget Report

download now -

Revenue Budget Progress Report

download now -

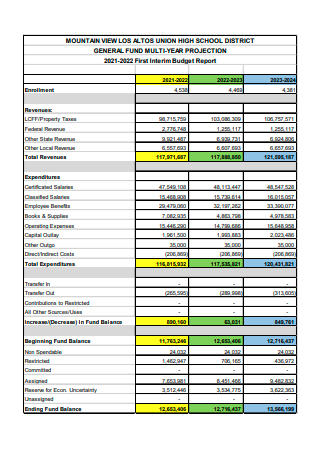

First Interim Budget Report

download now -

Budget Execution Report

download now -

Midyear Budget Report

download now -

Printable Budget Report

download now -

Budget Report Summary

download now -

Budget and Finance Report

download now -

Working Budget Report

download now -

Planning and Budget Report

download now -

Annual Budget Report

download now -

Gold Award Final Budget Report

download now

What Is a Budget Report?

Managers use a budget report to summarize previously projected budget estimates for a specified time. It is frequently used to compare budget estimates to the actual results obtained by the business within the specified time. Budget reports are primarily used to communicate the financial goals established by leadership based on accurate financial estimates. Because these budget reports are usually always estimates, they almost always differ significantly from the actual financial results. According to statistics, 61% of small firms do not have a formal budget.

Benefits of Budget Reports

Budgeting reports determine how closely the predicted budget corresponded to the actual financial data for a specified accounting period, a month, quarter, or year. Accounting workers will compare the financial report’s findings to the budget report they created before the commencement of the accounting quarter. Typically, budget reports serve as the company’s financial goals. If a financial statement falls short of the targets set in the budget report, staff can quickly see which issues are preventing them from meeting these targets by comparing the two reports. Additionally, employees compare budget and financial records to analyze the accuracy or reasonableness of their prior period’s financial estimates. Examining this data enables them to adjust to the upcoming budget report and produce more accurate future projections. If you’re still interested, here are some reasons budgeting is critical.

Types of Budgets

Historically, most firms have viewed budgeting to maintain the status quo. Typically, the current fiscal year’s budget and year-to-date actuals serve as the beginning point for the following fiscal year’s budget. While this is a perfectly legal strategy, it is only one of five primary budgeting processes available to business leaders. This part will look at each of the five ways of creating a budget and the specific advantages and downsides. Additionally, we’ll address the role of technology in enabling today’s firms to have a more efficient and thorough budgeting process.

-

1. Incremental Budgeting

The above-mentioned traditional approach is sometimes referred to as incremental budgeting. It frequently begins with the previous year’s budget numbers as a baseline, often incorporating year-to-date actuals and remaining predictions. These do not necessarily become the budget; instead, they serve as the foundation for the final budget. The next stage is to modify individual line items with predictable figures or to contain evident foreseeable changes. Lease payments are frequently consistent over an extended time. In a few instances, managers may be aware of spending categories that will experience significant declines or even disappear entirely. Following these more predictable improvements, applying a percentage of the uplift to various accounts or departments is customary. Thus, while incremental budgeting is more convenient than the other four ways discussed in this article regarding imposing a highly disciplined approach to spending, it may be the least effective in enforcing a highly disciplined approach.

2. Activity-Based Budgeting

Budgeting by activity (ABB) is a top-down strategy that focuses on the primary objectives. It begins with the end in mind and then delves into the question, “What must we do as an organization to accomplish our major objectives?” ABB then determines the resources and effort levels required to accomplish those goals. Consider an organization that has created a novel piece of technology. They are unknown in the market, and their product necessitates a highly consultative sales procedure. ABB prioritizes strategic objectives and pays far less attention to expenses that are not directly related to high-level aims. Business executives must exercise caution in applying ABB’s concepts too broadly. You may disregard or overlook departments that fail to generate precise, measurable results that contribute to achieving the company’s strategic objectives. Nonetheless, ABB has a more robust strategic focus than the other techniques on this list.

3. Value Proposition Budgeting

The third way is value proposition budgeting, which reviews each line item or budget category to determine why the money is spent. and “How much weight does it add to the lives of our customers, staff, and other stakeholders?” This approach strikes a balance between incremental budgeting and zero-based budgeting. Unlike activity-based budgeting, value proposition budgeting aims to justify costs based on the value they produce without requiring a direct connection to strategic goals.

4. Zero-Based Budgeting

Zero-based budgeting (ZBB) begins with a clean sheet of paper. Managers must use this strategy to set their financial requirements for the coming year and justify each line item independently of previous years’ data. Simply because a business has spent money on something in the past does not indicate it should resume doing so in the future. Budget owners must justify practically every planned spending under the zero-based approach. ZBB is a fantastic tool for reducing wasted expenditure in this regard. It enables business executives to aggressively trim bloated budgets and get expenses under control while avoiding adverse operational impacts. In effect, ZBB compels businesses to prioritize and take a more deliberate approach to cost management, focusing on the spaces that add the most value to the organization. Because it causes managers to analyze their expenditures and value thoroughly, ZBB frequently results in new inventions that help businesses function more effectively.

5. Driver-Based Budgeting

Driver-based budgeting (DBB) focuses on the critical variables that have the most significant impact on business performance and associates budget numbers with the substantial resources required to meet the company’s targets for each of those variables. External elements may also include overall market size, commodity prices, or weather conditions. DBB develops budgets by analyzing essential business objectives, making baseline assumptions about external drivers, and applying a results-driven approach to internal business drivers. If any of those input factors changes, you can quickly alter the budget to reflect the new circumstances. Consider a ski resort business, where early- and late-season revenue depends on weather conditions. A premature introduction of cold weather, mainly if there is an abnormally significant amount of snow early in the season, will surely harm income as skiers swarm to the slopes following a lengthy off-season. This affects personnel requirements for ski slope operations and housing, restaurants, and other auxiliary companies that benefit from favorable weather. In this case, weather conditions serve as a critical business driver, affecting practically every other aspect of the company’s operations.

How To Prepare a Budget Report

The budget of an organization determines how it uses capital to accomplish goals. As a result, budget preparation is a critical skill for any business leader—whether an established or aspiring entrepreneur, executive, functional lead, or manager. Before generating your organization’s first budget, it’s critical to understand what goes into one and the essential processes involved in creating one. The procedures outlined below can be used to develop budgets for individual projects, initiatives, departments, or the entire business.

-

1. Recognize Your Organization’s Objectives

Before preparing your budget, it’s critical to grasp the objectives your organization is pursuing during the period covered by it. By identifying those objectives, you can create a consistent budget and support them. Consider a business with a year-over-year revenue increase offset by rising expenses. That organization may benefit from concentrating its efforts on improving spending control during the budgeting process. Consider an organization that is launching a new product or service. The company may make additional investments in the fledgling business line to grow it. The business may need to cut spending or scale down growth ambitions elsewhere in the budget to accomplish this aim.

2. Calculate Your Income for the Budget Period

To allocate funds for business expenses, you must first accurately forecast your income and cash flow for the period. This might be a straightforward or complex process, depending on the type of your organization. For instance, a business that sells products or services to established clients who are contractually obligated to pay will likely have an easier time forecasting income than one that relies on active sales activity. In the second situation, it’s critical to consult previous sales and marketing data to see whether the industry is evolving so that you’re missing or exceeding prior trends. Apart from revenue generated by sales activity, you should include income from other sources such as investment returns, asset sales, and bond or share offers.

3. Determine Your Expenses

After determining your anticipated revenue for the time, you must estimate your expenses. This procedure divides expenses into three categories: fixed costs, variable costs, and one-time charges. Any expenses that remain consistent throughout time and do not vary significantly from week to week or month to month are considered fixed costs. Often, those expenses are fixed by contract, making them easy to forecast and account for. This category usually covers overhead expenses such as rent and electricity. Subscriptions for phone, data, and software are also included in this category, as are debt payments. Any expense that is consistent and predictable should be included.

4. Calculate Your Fiscal Surplus or Deficit

After you’ve computed all of your income and expenses, you may incorporate them into your budget. This is the section where you decide whether your predicted income is sufficient to meet all of your costs. If your revenue surpasses your expenses, you have a budget surplus. With this information, you can choose how to allocate additional dollars best. You may, for instance, invest the funds in a rainy day fund that you can access if your actual income falls short of your estimates. Alternatively, you might use the money to expand your firm. If your spending surpasses your revenue, you have a budget deficit on the other side. You must determine the best course of action for closing the gap at this stage. Can you increase your revenue by selling more aggressively? Are you able to reduce either your fixed or variable expenses? Would you consider selling bonds or shares of company stock to raise more funding for the business?

FAQs

What is a summary report of the budget?

The budget summary contains budgeted amounts, encumbrances, transaction totals, and budget balances and serves as the online counterpart to the printed BSR. Open credits are now included in the budget summary report.

What is a worksheet for budgeting?

The budget spreadsheet is your tool for identifying, listing, quantifying, and costing all the resources required to carry out the project’s activities. It’s a fantastic tool for assisting you in creating accurate and comprehensive activity-based budgets.

What is revenue from the budget?

The revenue budget balances the government’s revenue receipts (taxes and others) with expenditures. Revenues are classified as tax and non-tax. Tax revenues are derived from the government’s imposition of income tax, corporate tax, excise, customs, and other duties.

One reason budgeting might be challenging is the variety of ways in which teams pay for things. Credit cards, bills, and expense claim all affect your budget. However, team leaders may quickly lose track of how much money has been spent because they are managed differently. And when the time comes to create your following budgeting report, you’ll have all the data you need already structured and ready to go on the platform. What was once a difficult task is now a matter of a few clicks.