An Internship Letter of Recommendation is a formal document written by a supervisor, mentor, or professor to endorse an intern’s skills, work ethic, and potential. This formal letter highlights…

continue reading

Rating :

Everyone needs a place to live and raise a family. This shelter is our home. Even though it is one of the fundamental requirements of humans, it isn’t easy to purchase one you can name. Currently, the housing market is booming, and many developers are rushing to sign as many land sale contracts as possible. As a result, the prices of these residences have reached an all-time high. You would likely question your ability to finance a property.

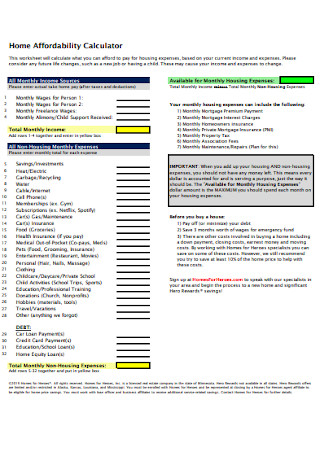

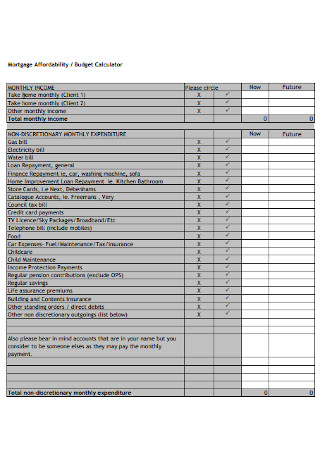

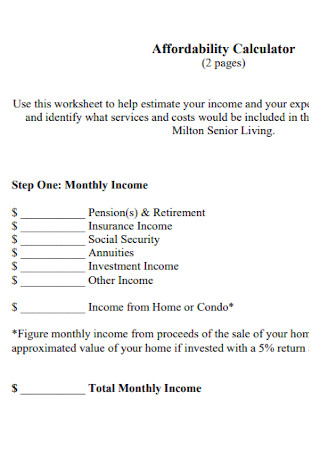

How will you determine if you can purchase a home? There are three ways to achieve this task. Consult a real estate professional for assistance finding a home within your budget. Depending on your salary, you can also inquire with your bank about their home loan offerings, how to qualify, and whether you can afford a mortgage. Alternatively, one might utilize a home affordability calculator. It is the most straightforward and convenient approach for anyone to assess whether or not they can purchase a home. A home affordability calculator can be a spreadsheet or an online calculator that does the intricate calculations required to determine if a person can afford a home, depending on their income. This tool is highly user-friendly; you only need to copy, paste and enter the required data into the appropriate fields. In 2021, the homeownership rate in the United States reached 65.5%. The homeownership rate is the percentage of occupied homes that are owned. Before the 2007-2009 crisis that destroyed the housing market, this peaked in 2004.

There are a lot of obvious benefits to owning a home, but there are also some less obvious ones. Before purchasing a home, one thing to do is decide if it’s right for you. When making a choice, it’s essential to think carefully about the pros and cons of that choice. If you currently live with family or friends or rent a place and are thinking about buying a home, here are some of the best things about it. Knowing the benefits of owning a home can make it easy to decide whether or not to buy one.

Once you begin to evaluate when and how to purchase a home, you will certainly receive a variety of advice – some beneficial, some not. And while the process might be lengthy, buying a home is exciting, fulfilling, and a significant investment. Use this checklist as a guide to ensure you’re prepared for the various parts of the home-buying process before taking the plunge.

How much money is required to purchase a home? Especially if you are a first-time homebuyer, this is the first question you will want to ask yourself. Before you begin your house search, you must identify your budget. Consider your current monthly income and spending. Several online mortgage calculators can assist you in determining what you may be able to afford. Remember that you will also need to budget for new expenses associated with house ownership, such as insurance, probable homeowner association (HOA) fees, taxes, landscaping and yardwork charges, utilities, repair costs, etc.

Obtaining professional assistance may seem like an optional step on your home-buying to-do list, but it can make the home-buying process much more manageable. A real estate agent can answer any questions, point out features to look for in properties, assist you in making an offer, and negotiate a price with the sellers. In addition, real estate agents are frequently more knowledgeable about the market value of other homes in the neighborhood and may be aware of properties that are not advertised publicly. If a bank or financial institution lists a new home, real estate agents are frequently the first to know, which can give you an advantage when searching for a home before other buyers discover it’s available.

No home is just right. Pay attention to the most important things, and don’t worry about the small stuff. Try to see yourself living in the house for a long time. When you start examining for a home to live in, the furniture, artwork, and clean towels can make you fall in love with the site’s style or the people who live there. Try to look past this and pay attention to what’s most important: the home itself. Try to picture the rooms without furniture to see how big they are. Check the countertops, floors, and walls for flaws that may have been hidden by staging.

Your mortgage payment is just the first step. If you are a first-time homebuyer, there’s a variety of incentives and programs available to assist you in locating the appropriate money to buy a home. Each state offers unique programs and incentives for first-time homebuyers to facilitate purchasing. Incentives may include decreased loan rates if income and property limits are met, aid with down payment and closing costs, and a potential federal income tax burden reduction.

Do not become disheartened if you miss out on the first or second home or if the seller refuses to negotiate the price. Your credit score will determine whether you are approved for a mortgage and how much interest you will pay. This step in the home-buying process can save you hundreds of dollars over the years. How do you increase your credit score and manage poor credit? Reduce your debt and maintain credit card balances below 20% of the available balance. Avoid shutting any of your accounts, as this will shorten your credit history and lower your credibility as a borrower. Paying your obligations on time is the most straightforward strategy to increase your credit score.

If you’ve fallen in love with a home, do not reveal your hand to the seller’s agent. Reserve your position and prepare to negotiate. One of the numerous errors homebuyers make is failing to get pre-approved for a mortgage before shopping around. This can make it easy to fall in love with an expensive property. Most sellers are hesitant to accept an offer from an unapproved buyer. Also, they may want to immediately get the buyer’s loan approval, which can result in them accepting another offer. To avoid this, meet with a lender before you search for answers to your financial questions and the pre-approval paperwork. Your mortgage interest rate will significantly impact the overall cost of your home, so it is essential to shop around for the best mortgage lender. Loan terms, interest rates, and fees will vary depending on the lending institution. Before you begin your search for a home, you should consult multiple real estate agents to obtain the best deal.

A lender’s pre-qualification process considers your finances (such as income and debt) to decide the amount of money they are willing to give you. Once the lender has finished an initial evaluation, they will often provide a pre-qualification letter stating the maximum mortgage amount you qualify for. A lender will pre-qualify you to confirm that you can afford the loan.

Purchasing a home is an investment, but its profitability depends on several factors. Buying one is a wise investment if you need a place to live. There are substantial up-front and ongoing costs associated with your home. If you accumulate sufficient equity and market when the real estate market tends to sell, you will probably realize a favorable return on your investment due to appreciation. But if the market is weak, if you have little equity in the home, or if you must sell too soon, you may incur a loss.

Yes, you can sell your home without the deeds, but you must be able to prove your ownership of the property through other means. As the deeds are the collection of documents that typically prove ownership, proving it with them may be more accessible but not impossible.

Before deciding to purchase a home, you should consider the following. You may finally declare that you are prepared when you have evaluated everything. No longer must you rely on a single source. You may learn more about the affordability of homes and mortgages by researching related subjects.

An Internship Letter of Recommendation is a formal document written by a supervisor, mentor, or professor to endorse an intern’s skills, work ethic, and potential. This formal letter highlights…

continue reading

A Relationship Statement is a formal declaration that outlines the nature, history, and dynamics of a relationship between two or more parties. It serves as a vital document in…

continue reading