21+ Sample Mortgage Statement Templates

-

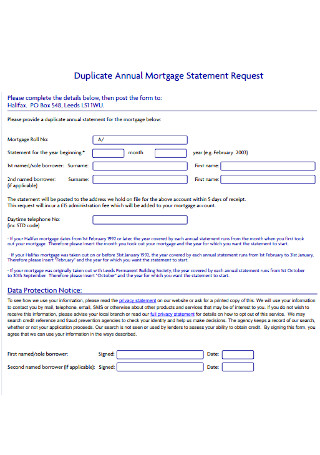

Duplicate Annual Mortgage Statement

download now -

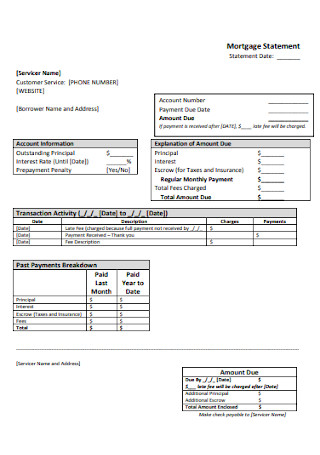

Standard Mortgage Statement Template

download now -

Basic Mortgage Statement Template

download now -

Mortgage Interest Statement

download now -

Annual Mortgage Statement

download now -

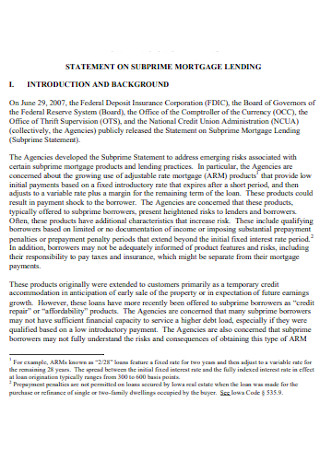

Statement on Subprime Mortgage

download now -

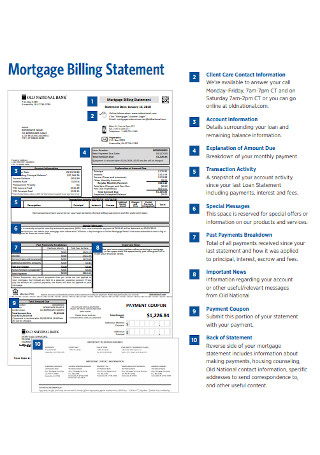

Mortgage Billing Statement

download now -

Mortgage Statement Format

download now -

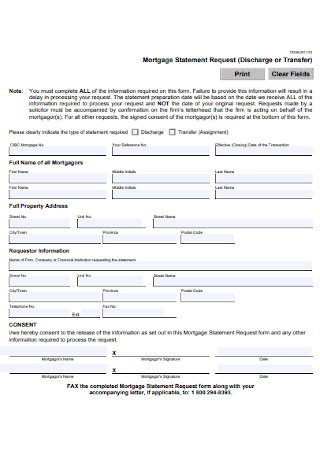

Mortgage Statement Request Template

download now -

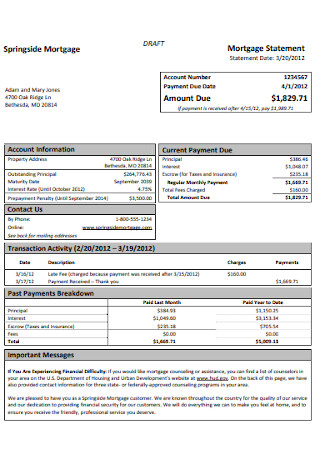

Springside Mortgage Statement

download now -

Simple Mortage Statement Template

download now -

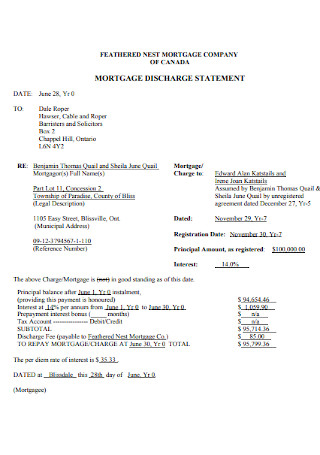

Mortage Discharge Statement

download now -

Mortgage Statement of Claim

download now -

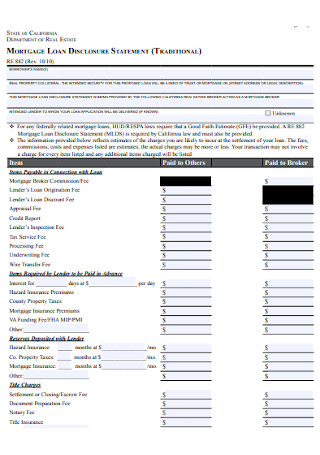

Moorage Loan Disclosure Statement

download now -

Mortgage Payoff Statements

download now -

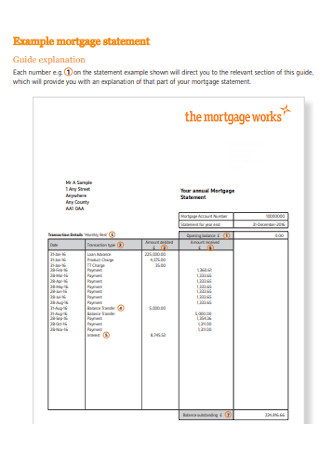

Mortgage Statement Example

download now -

Financial Statement for Mortgage

download now -

Company Mortgage Statement

download now -

Sample Mortgage Statement Template

download now -

Monthly Mortgage Statement Template

download now -

Mortgage Discharge Statement

download now -

Mortgage Verification Statement

download now

FREE Mortgage Statement s to Download

21+ Sample Mortgage Statement Templates

What Is a Mortgage Statement?

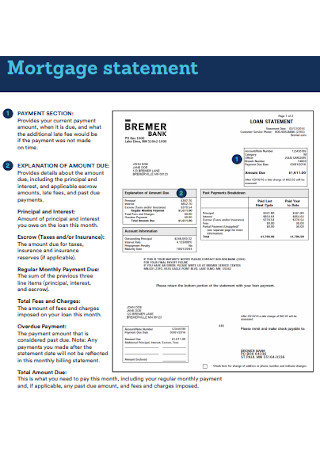

The Important Elements of a Mortgage Statement

How to Create a Proper Mortgage Statement

FAQs

What is a mortgage payoff statement?

What is another name of the annual mortgage statement?

Are mortgage statements only provided by your lender?

What Is a Mortgage Statement?

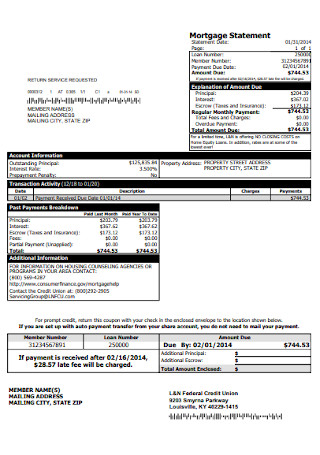

In simple terms, a mortgage statement is an official document to prepare by the mortgage holder until it will be shared with the borrower. The statement contains the current mortgage balance, payment history, and other essential parts of a mortgage. And whether you have an annual or monthly mortgage, the standard procedure is to provide the debtor or borrower with the mortgage statement per month. So basically, it is similar to a monthly billing statement except its content is related to the loan balance and other mortgage-related information.

Did you know that the mortgage balances in the US totaled $9.86 trillion in the third quarter of 2020?

Meanwhile, Section 1420 of the Dodd-Frank Act amends the Truth in Lending Act, which details how every creditor, assignee, or servicer is required to provide serial billing statements to the borrower.

On another note, Investopedia said that an annual mortgage statement has many names—a year-end statement, Form 1098, or the mortgage interest statement.

Why Are Mortgage Statements Needed?

A mortgage statement is consequential for many reasons. Let us start with how it keeps every borrower up to date about his or her mortgage balance, interest rate, loan amortization schedule, and so much more—making it easier to remember and keep up with every mortgage payment. Avoid being past due since the statement tells you about the mortgage term schedule. Also, the mortgage statement is a reliable document for proof, especially when you need to show a receipt for errors. Notify the mortgage holder right away with this statement.

Moreover, mortgage statements are needed legally. In fact, Section 1420 of the Dodd-Frank Act amended the Truth in Lending Act. It stated how every assignee, creditor, or servicer is required to give serial billing statements to borrowers. So it is not only important but also required for compliance. And finally, mortgage statements are considered as notice documents in case borrowers need to renew their mortgage or if they should stick with their creditors but with a new interest rate.

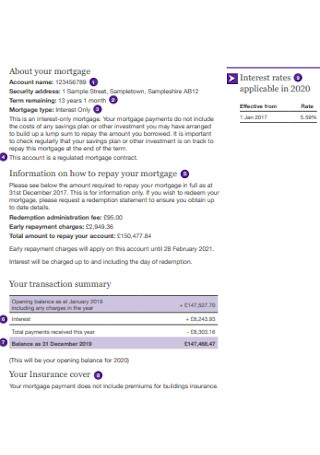

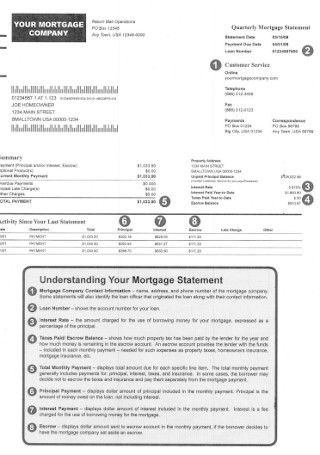

The Important Elements of a Mortgage Statement

Whether you end up paying for your first mortgage or provide a mortgage statement to a borrower for the first time, you must know what to specifically write in the mortgage statement. Expect different sections into that statement which you should fully understand. So in this section, we will introduce you to the different elements that make up a complete mortgage statement.

How to Create a Proper Mortgage Statement

Now that we have explained a mortgage statement’s definition, necessity, and corresponding elements, you are now prepared to make the statement itself. Don’t be overwhelmed because the process is quite manageable, especially when we laid out five easy steps for you to follow. And without further ado, here are the steps on how to make a mortgage statement properly:

Step 1: Use a Sample Template for Tweaking

In case you haven’t noticed, there is a full list of mortgage statement samples above that you can download and customize anytime. And each premade template is designed to ensure you can come up with the said statement effortlessly. Do not forget to make it obvious that the document used for the mortgage statement clearly represents that of a statement. You can achieve that by ensuring there is a visible title ‘Mortgage Statement’ in bold or capital letters right on top of the sheet. That way, people get the gist immediately regarding what the document’s purpose is.

Step 2: Lay Out the Mortgage Statement’s Elements

You already knew the elements of a mortgage statement from the account number, payment history, delinquency notice, and so forth. So make sure to insert each element into the template you are working with. But, you are not just to insert those elements drastically. Arrange their layout as well. Each element has its specific category and you can arrange the elements into their categories. In fact, formatting and designing the template is one of the important tasks you need to complete in making the statement anyway.

Step 3: Provide an Easy-to-Follow Structure

To arrange all the information really well, observe an easy-to-follow structure. That means you consider every element’s placement strategically, use simple words, and provide some instructions or detailed explanation. Aim to make sure the borrower or anyone who reads the mortgage statement will understand the whole message according to how you want them to perceive it. With this structure, rest assured, you can avoid any misleading information. Hence, don’t make the mortgage statement more complicated.

Step 4: Use Tables, Charts, and Visual Organizers

Speaking of an easy structure, you can do that through the use of tables, charts, and other visual organizers. A statement is not your average letter that is only written in sentences and paragraphs. You can use symbols in displaying how the mortgage was calculated, a chart that shows the full transaction history, and more. Another idea is to enumerate the instructions instead of writing complete sentences that are too long. And how you want to organize and design the whole statement is up to you.

Step 5: Send the Statements Timely

Finally, you can send your mortgage statement to the respected borrower when you are done. But, be timely in doing so because just like most bills, you have to be early in sending mortgage statements. Otherwise, it is bad when the borrower receives a statement that is already due how many months ago. Do not forget to decide how you will submit those mortgage statements as well. Others prefer sending an email to the debtor while some prefer printing the document. Also, you need to finalize if you prefer the statement in MS Word or PDF. So if ever you are the mortgage holder or the person assigned to create mortgage statements, take note of your responsibilities to submit them on time.

FAQs

What is a mortgage payoff statement?

A mortgage payoff statement is an official statement provided by the lender. It contains the payoff amount for a mortgage prepayment. Also, expect the mortgage payoff statement to display the payment balance to successfully close the loan.

What is another name of the annual mortgage statement?

According to Investopedia, an annual mortgage statement is also referred to as a year-end statement, Form 1098, or mortgage interest statement. And despite their different names, they all mean the same thing.

Are mortgage statements only provided by your lender?

Lenders often provide mortgage statements but it doesn’t mean that such statements should only be generated by them. There are loan servicers and other representatives who can manage it too. As much as possible, ask questions directly from who provides the statement.

From reviewing your current mortgage payment, renewing a mortgage, fixing mortgage errors, down to following the legal requirements of a mortgage, you will eventually come up with a mortgage statement. It becomes your official document to answer any important questions for such a loan that concerns both the borrowers and the creditors. So be sure you won’t get caught off guard with mortgages by checking out our sample mortgage statement templates above. Explore, design, edit, print, and download now!