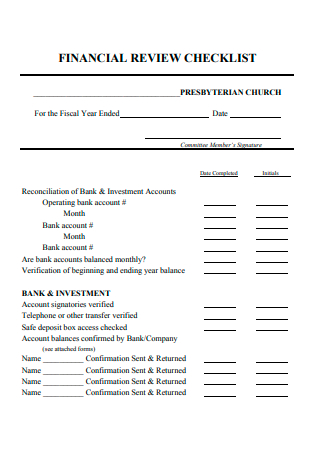

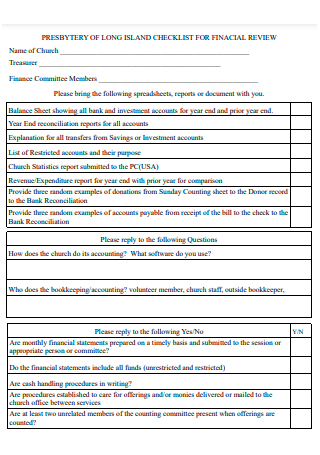

18+ Sample Financial Review Checklist

-

Financial Statement Review Checklist Template

download now -

Basic Financial Review Checklist

download now -

Monthly Financial Review Checklist

download now -

On-Site Financial Review Checklist

download now -

Financial Review Checklist Example

download now -

Standard Financial Review Checklist

download now -

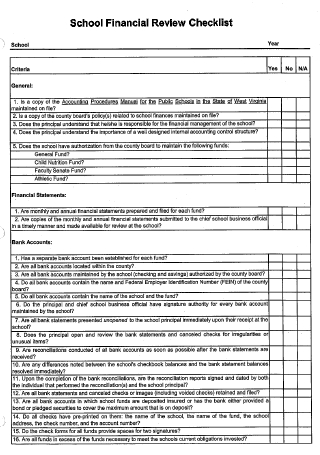

School Financial Review Checklist Template

download now -

Financial Review Checklist in PDF

download now -

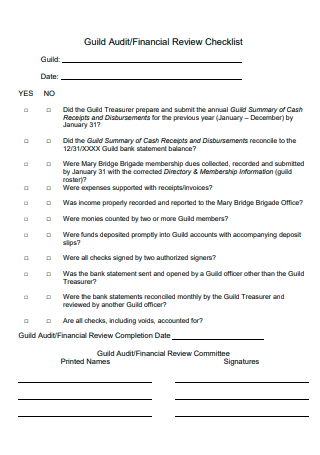

Extension Group Financial Review Checklist

download now -

Annual Financial Review Checklist

download now -

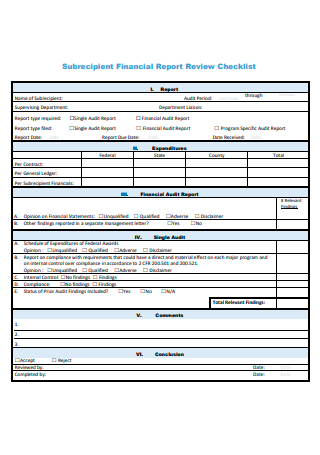

Financial Report Review Checklist

download now -

Formal Financial Review Checklist

download now -

Annual Financial Report Internal Review Checklist

download now -

Printable Financial Review Checklist

download now -

Sample Financial Review Checklist Template

download now -

Financial Review Checklist Format

download now -

Simple Financial Review Checklist

download now -

Draft Financial Review Checklist

download now -

Financial Assurance Review Checklist

download now

FREE Financial Review Checklist s to Download

18+ Sample Financial Review Checklist

a Financial Review?

Benefits of Having a Business Financial Advisor

Tips To Conduct Annual Financial Review

How To Create a Quarterly Financial Review Checklist

FAQs

What should a financial evaluation include?

How is a financial report formatted?

What is the proper sequence in which financial statements should be presented?

What Is a Financial Review?

If you want to understand whether or not a company’s financial statements are factual, you need to look at their financial records. The goal of an independent auditor’s financial “review” is to look at the nonprofit’s financial statements and see if they are in line with standard accounting practices. People in the financial industry say that getting professional financial advice can add 1.5% and 4% to a portfolio’s long-term returns, depending on the time and how returns are calculated.

Benefits of Having a Business Financial Advisor

As a business owner, you have a bunch going on. You have to do many things and costs when you run a business, and you don’t need another bill to pay. It’s essential to think carefully about how well any service you get will pay off for you and your business. Running a company is a lot of work. There are always things that go wrong, but you want to ensure that the consequences aren’t too dire. Mismanaging money, having problems with cash flow, late payments, tax problems, and other financial problems can be bad enough to close down a business. That’s why it’s so important to keep an eye on your business’s money. Hiring a good financial advisor can help your business stay afloat. There are many ways that a qualified financial advisor can help you and your business grow together.

Tips To Conduct Annual Financial Review

If you were on a lengthy road journey, you would pause periodically to check the map to ensure you were heading correctly. An annual financial checkup accomplishes the same thing. It’s an opportunity to reflect on your financial performance over the previous twelve months and ensure you’re still on track with your money management. While it’s best to review your finances before the end of the year to take advantage of any tax-saving techniques, if you’re unable to do so during the busy holiday season, aim to do so as soon as possible. The following are the necessary steps to take when organizing a financial checkup:

-

1. Determine Your Objectives

The first step in performing a financial health check is determining your financial objectives. Have you made any progress on completing them this year? If not, how did you come up short? Are you able to deduce why? Have your objectives shifted throughout the year? If so, rewrite and record them. Establish clear goals and divide them into monthly, quarterly, and annual action steps.

2. Evaluate Personal Situational Changes

Have your circumstances changed significantly in the recent year, or do you foresee any significant changes shortly? A job change, divorce, adding a child to your family, retiring, purchasing a home, marrying, or moving can substantially impact your income and lifestyle. You may need to adjust your budget, expenditures, savings, and assets. Having time to plan for these adjustments in advance will significantly ease the transition.

3. Guard Your Assets

The next item on your annual financial checkup checklist should be an examination of your asset protection. Begin by checking your homeowner’s or renter’s insurance policies and your health and auto insurance policies. Don’t forget to watch your most valuable asset – your capacity to earn an income – with long-term disability insurance. While you’re at it, examine your insurance coverage and premiums. Consider whether you may save money by changing carriers or bundling your multiple insurance policies with the same provider.

4. Prepare for the Unexpected

Examine your will and, if necessary, your estate strategy. Have any changes occurred that necessitate updating? If this is the case, you may desire to revise your will. Additionally, examine your life insurance coverage to ensure you have an excellent policy to safeguard your dependents in the event of your death financially. And if you don’t already have life insurance, you should consider getting it sooner rather than later. Your premiums are likely to be inferior if you are younger and healthier. Consult a life insurance agent to determine whether a term or permanent life insurance coverage is the better option for you.

5. Assess the Performance of Your Investments

Calculate the annualized rate of return on each of your stocks, bonds, and mutual funds. Are you happy with their performance in comparison to the competition? If you suspect the investment will not make a profit, it may be time to sell the dogs. The end of the year is ideal for taking advantage of tax losses. Harvesting losses enables you to offset capital gains on investments with losses on underperformers.

6. Assess Your Debts

Consider your debt management skills as part of your annual financial review. Assess your debt-to-income ratio in particular. Have you seen a decrease in your credit card debt this year? If not, it’s time to determine the source of the leaks and attempt to stop them. It’s tough to go ahead and invest when a large portion of your income is spent on credit card interest payments. What is your mortgage interest rate? Is it time to consider refinancing? Even a minor rate decrease can significantly impact the life of your mortgage, but you must consider closing fees to determine whether the savings are reasonable.

How To Create a Quarterly Financial Review Checklist

Regularly reviewing your accounts is crucial to the success of your financial strategy. However, how do you know what to look for and how frequently you should conduct a financial review? While it’s prudent to conduct a financial review at least once a year, regularly working one might help you keep more in tune with your money and goals. If you’re unsure what to prioritize, utilize this handy checklist as a reference.

-

1. Begin with a review of your credit report and score.

Your credit report and score are critical pieces of the puzzle of your financial wellness. A high credit score and an extended credit record might make it easier to get loans when you need them and pay lower interest rates on the loans you take out. Take time to evaluate your credit report as part of your quarterly financial review. You should check your credit statements from all three leading credit agencies. You may acquire your credit reports for free from some websites. Alternatively, a free credit monitoring service can provide you with your credit report and score. If you discover an error or inaccuracy, dispute it with the credit bureau that reported the information.

2. Continue to Your Budget

A budget is highly beneficial for controlling spending and working toward your savings goals. Conduct a line-by-line examination of your monthly expenditures during your quarterly financial review. Consider whether spending has increased or decreased or new expenses have been added since the previous quarter. Following that, have a look at your income. Are you earning more, less, or the same amount of money? If your payment has increased and your costs have decreased, you now have additional funds to spend toward debt repayment or savings. If your income has remained constant, but your expenses have increased, you may need to analyze your spending to decide if there are any areas where you can cut back or eliminate. If you are in debt, review your existing debt repayment strategy. Consider whether you’re still on schedule to pay off your debt by the date you’ve set. If your expenses have been reduced or your income has increased, consider increasing your monthly debt payments to pay off your balance faster.

3. Consider Your Investments a Second Time

The stock market is volatile, and your investments may see more dramatic ups and downs than others. By including a portfolio review in your quarterly financial assessment, you can ensure that you’re still keeping a suitable asset allocation based on your risk tolerance. Additionally, you should review the fees associated with your investments quarterly. Increased costs can dramatically reduce returns, which is amplified during market downturns. If you’re performing your financial assessment in the fourth quarter, you may also want to consider harvesting failures in your portfolio to offset any year-end gains. Tax-loss harvesting can assist you in minimizing the tax consequences of reporting capital gains on your more profitable investments.

4. Verify Your Insurance Protection

It would benefit if you had insurance to cover your home, automobile, life, and health, but it does not imply you should pay more than necessary. Review your coverage quantities, premiums, and deductibles every quarter. Consider whether you are eligible for any discounts on coverage that you are not utilizing or whether you may lower your costs by increasing your deductible. Additionally, check for any gaps in your insurance policy. For instance, if you recently married or received your first child, it may be time to consider purchasing life insurance if you do not already have it. If you die, life insurance can provide a financial benefit to your surviving spouse by helping to pay off debts, cover monthly costs, and assist with the cost of child-rearing.

5. Examine Your Contributions to Your Retirement Plan

It’s better to start planning for retirement as soon as possible, and your employer’s plan can be an excellent way to start. In a tax-advantage plan at work, look at how much you’re saving on figuring out how much you need to keep. If you aren’t on track to reach the annual contribution limit, you might want to change your donation rate to get closer to the limit each year. You can still save money with a traditional or Roth IRA when your job doesn’t have one. This is another way to keep in addition to your job’s savings plan or place of one if your job doesn’t have one. Make sure you look over your options and budget to figure out how much money you can save in an IRA each year.

6. Refresh Your Objectives

Setting objectives can be a powerful motivator to save and spend more efficiently. The third component of your financial assessment is tracking your progress toward your goals each quarter. If you can check a plan off your list, consider adding additional goals as you continue to construct your financial strategy.

FAQs

What should a financial evaluation include?

Financial reports frequently include a section titled “Notes to the Financial Statements,” containing critical firm information. Consider what additional information regarding the organization’s finances would be most valuable in your report’s “Notes” section and then incorporate it.

How is a financial report formatted?

Revenues are listed first on an income statement, followed by expenses. The expenses are removed from the payment to arrive at the business’s net income.

What is the proper sequence in which financial statements should be presented?

Financial statements are arranged in a particular order because data from one account is carried over to the next. The procedure begins with the trial balance, followed by the modified trial balance, the income statement, the balance sheet, and the account of the owner’s equity.

Before submitting your financial review, thoroughly read it and any additional reports to ensure they are consistent. If there are inconsistencies or extraneous information, ensure that you review and resolve the issue immediately with your audit team to determine the best course of action in these circumstances. To assist you in creating your financial review checklist, feel free to utilize the free sample templates offered above as a guide!