66+ Sample Repayment Agreements

-

Loan Repayment Agreement Template

download now -

Car Loan Repayment Agreement Template

download now -

Debt Repayment Agreement Template

download now -

Simple Repayment Agreement Template

download now -

Repayment Agreement Template

download now -

Sample Repayment Agreement Template

download now -

Employee Repayment Agreement Template

download now -

Training Repayment Agreement Template

download now -

Payroll Repayment Agreement Template

download now -

Personal Loan Repayment Agreement Template

download now -

Sign-On Bonus Repayment Agreement Template

download now -

Letter Agreement on Repayment Schedule Template

download now -

Repayment Arrangement Agreement

download now -

Employee Personal Loan Repayment Agreement

download now -

Tenant Promissory Note Repayment Agreement

download now -

Sample Debt Repayment Agreement

download now -

Simple Loan Training Repayment Agreement

download now -

Financial Money Repayment Agreement

download now -

Repayment Private Loan Agreement

download now -

Salary Advance and Repayment Contract Agreement

download now -

Tuition Payroll Repayment Agreement

download now -

Transition Settlement Agreement debt Repayment Agreement

download now -

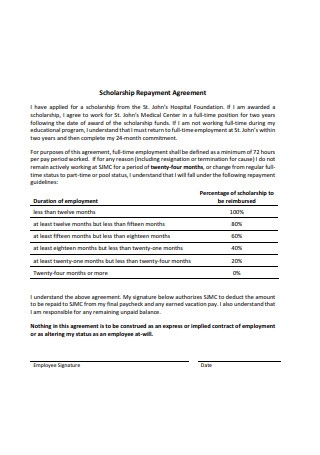

Scholarship Installment Payment Repayment Agreement

download now -

Relocation Expense Monthly Payment Repayment Agreement

download now -

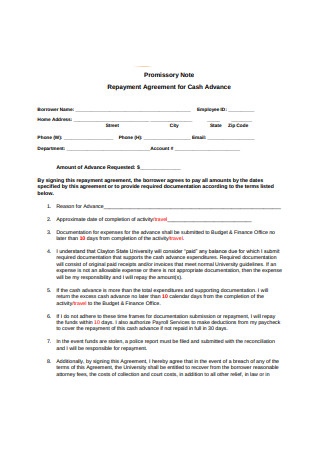

Repayment Agreement for Borrowing Money Cash Advance

download now -

Relocation Staff Loan Repayment Agreement

download now -

Sample Repayment Agreement Payment Plan Format

download now -

Basic Bonus Repayment Agreement

download now -

Student Loan Repayment Agreement Form

download now -

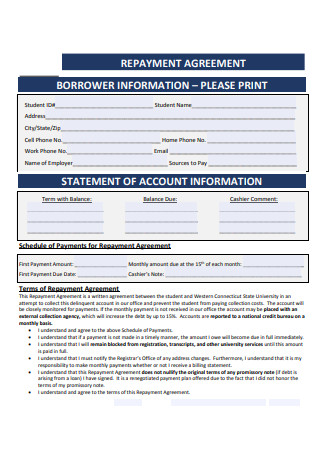

Repayment Schedule Agreement

download now -

Simple Repayment Agreement

download now -

Benefit Repayment Agreement

download now -

Repayment Agreement Example

download now -

Basic Repayment Agreement Format

download now -

Scholarship Repayment Agreement Format

download now -

Repayment Agreement Processing Plan

download now -

Loan Repayment Service Agreement

download now -

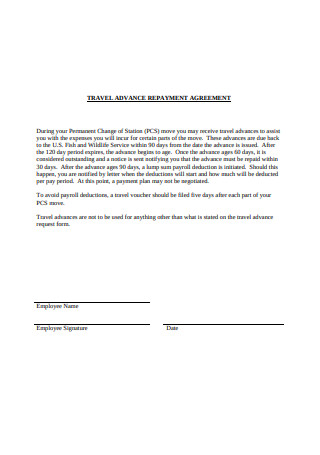

Travel Advance Repayment Agreement

download now -

Standard Repayment Agreement

download now -

Repayment Agreement Sample

download now -

Relocation Repayment Agreement Format

download now -

Basic Repayment Agreement Example

download now -

Repayment Agreement Policy

download now -

Printable Repayment Agreement

download now -

Subsidy Repayment Agreement

download now -

Sample Repayment Agreement Example

download now -

Loan Repayment Agreement

download now -

Tuition Repayment Agreement Format

download now -

Resident Repayment Agreement

download now -

Service Repayment Agreement

download now -

Loan Repayment Agreement Format

download now -

Repayment Agreement Cover Letter

download now -

Simple Repayment Agreement Format

download now -

Repayment Agreement Policy Format

download now -

Repayment Agreement Policy Example

download now -

Employee Repayment Agreement Format

download now -

Standard Repayment Agreement Format

download now

FREE Repayment Agreement s to Download

66+ Sample Repayment Agreements

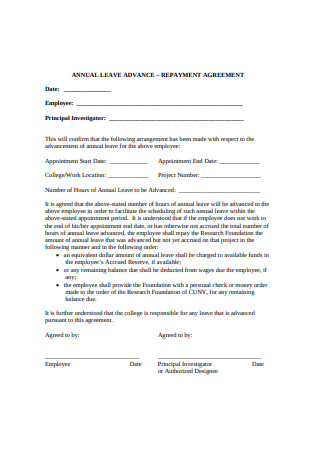

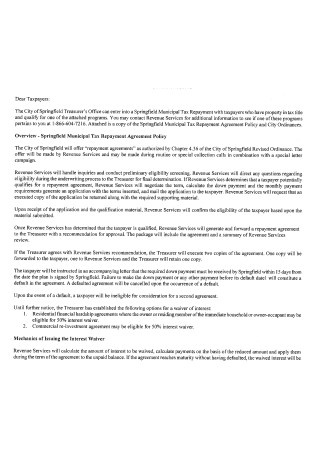

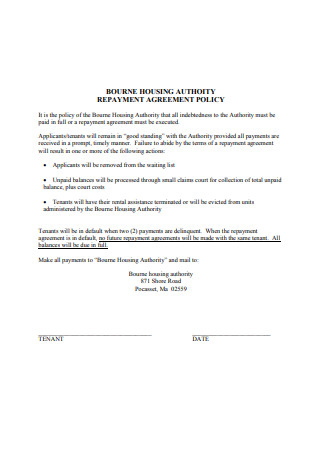

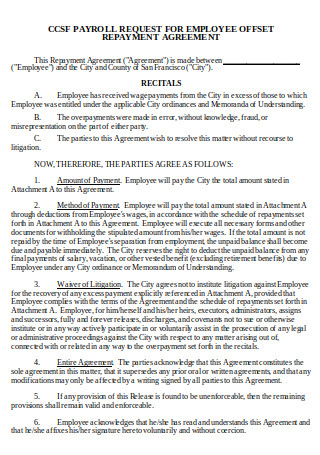

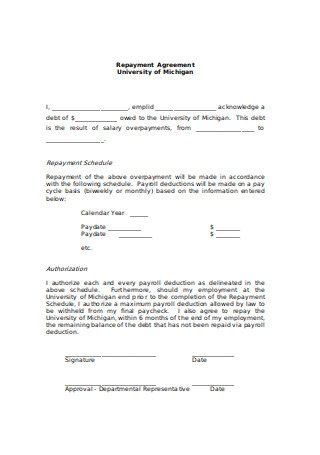

What Is a Repayment Agreement?

Loans that People Usually Apply for

How to Draft a Secure Repayment Agreement

FAQs

How do you compute the cost for a loan payment?

Is it okay to close a personal loan earlier than the deadline?

What happens if you don’t pay your loan?

What do you mean by “Debtor’s Prisons?”

What is an acceptable credit score?

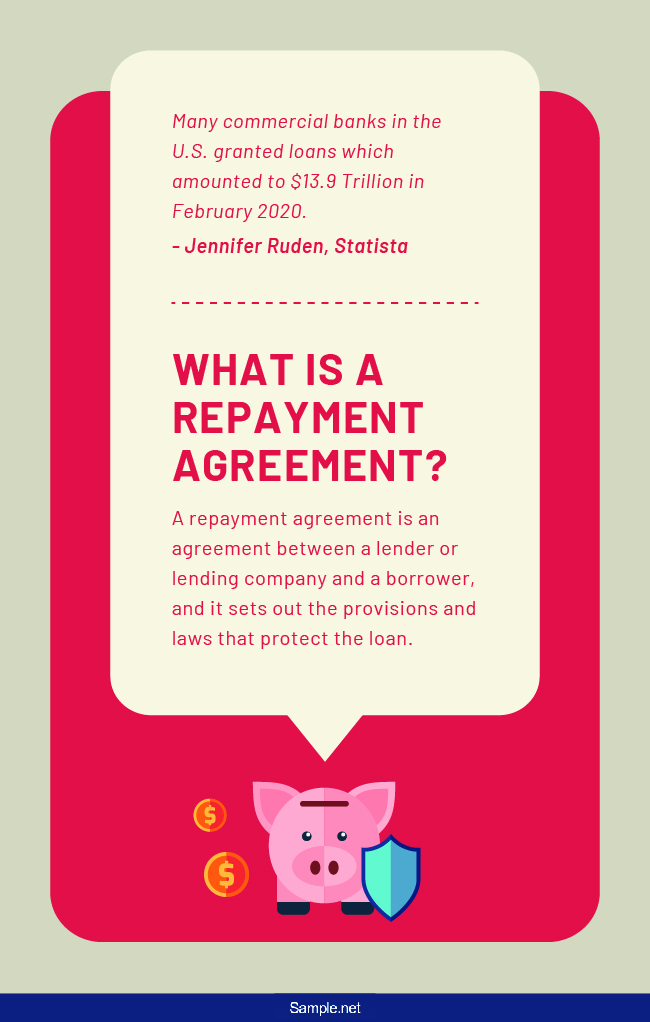

What Is a Repayment Agreement?

When an individual applies for a loan, it is only normal for a lender to expect repayment. Interest rates are what gives life to a loan, and this is where a lender profits. The schedules for repayment will depend on the lender who supplies money to a borrower. Still, before a lender lends, he/she gets into an agreement with the borrower—a repayment agreement. A repayment agreement is an agreement between a lender or lending company and a borrower, and it sets out the provisions and laws that protect the loan. Note that keeping loan documents is very important because they serve as security for the money being handed over to a borrower.

Loans that People Usually Apply for

Loans can be used for different purposes. People usually use it for personal reasons or for business plans. The lender doesn’t care much about where borrowers use the money they have. What matters most for them is the ability of borrowers to repay their debts. According to Jennifer Ruden, commercial banks in the U.S. granted loans amounting to $13.9 trillion in February 2020. Loans come in different types, and the following are loans that people usually apply for:

How to Draft a Secure Repayment Agreement

A person can repay loan agreements in two ways—fixed or on-demand. Fixed repayments apply to purchases that require a large sum of money. The payment schedule is set on a specific time and begins the moment a borrower signs an agreement. On the other hand, payments on demand happen when a person borrows from someone they know. It is different from a fixed payment since it doesn’t set a specific time for payment since that comes on demand. A repayment agreement should specify the conditions for payment and the obligations of the parties involved towards each other. Here are the steps in making a sample repayment agreement:

Step 1: Define Legal Terms

One should clearly define all legal terms written in the agreement. This can include terms concerning the payment plan, interest rate, collateral, etc. According to debt.org, there are also important terms that the parties involved should understand before signing a repayment agreement. This includes the terms—involved parties, choice of law, severability provision, and entire agreement provision. For example, the severability provision is a statement that expresses the independence of every condition written in the contract.

Step 2: Determine the Interest Rate

Bear in mind that interest rates rest on the loan type you are applying for. There are cases where a lender will stipulate collateral, but this demand should not go beyond the value of your loan. In fact, there are state and federal laws that protect a borrower from tying a high-value asset to a low-value loan. Additionally, an interest rate can be floating or fixed. A fixed-rate remains constant all throughout your repayment period while a floating rate changes over time.

Step 3: Include Terms for Pre-Payment and Breach

Lenders have the right to impose prepayment penalties to a borrower who pre-closes an agreement. For example, if a borrower pays ahead a 10-year loan in five years, the lender wouldn’t get any profit from the interest rates he/she expects to receive within the 10 years. In terms of contract default, a borrower who delays on repaying his debts will automatically be considered as a violator of the contract. The violated lender can take action and bring the issue to court to hold the borrower liable for any damages caused. Moreover, this will affect the credit score of the borrower.

Step 4: Assert Laws for Protection

The 1968 Consumer Credit Protection Act seeks to protect borrowers from usury and abuse. Specifically the Home Owners Protection Act, Real Estate Settlement Act, and the Truth in Lending Act are federal laws that prevent lenders from being unfair to borrowers. For example, the Truth in Lending Act is a law that requires the lenders to disclose information to a borrower before increasing any credit. Therefore, including these laws in the contract is essential.

FAQs

How do you compute the cost for a loan payment?

Loan computations vary and depend on the loan type. To easily compute for loan payments, you can download special calculators which are available online for your convenience. You can use a credit card calculator, interest calculator, or amortization calculator. By simply using one, you will be able to determine the amount you need to pay for your loan.

Is it okay to close a personal loan earlier than the deadline?

Repaying your loan earlier than the set timeline is okay, but some lenders may demand a fee for pre-closing the agreement. Nevertheless, this will also free you from the burdens of your debt. It is wise to take a look at the penalty provision in your contract and do a computation. If the result of your calculation benefits you, then it is wise to pre-close your loan.

What happens if you don’t pay your loan?

If you’re worried about getting into jail, don’t be, since the debtors’ prisons have been eliminated by the law years ago. Instead of getting into prison, you will be charged with more interest and fees on your credit account. Once that happens, it may be very hard for you to recover. Even if that is true, there are still many ways you can address the issue by borrowing again.

What do you mean by “Debtor’s Prisons?”

Before and during the mid-1800s, lenders imprisoned poor people who couldn’t pay their debts in a place called debtors’ prisons. Years after that, the U.S. government terminated this concept. For that reason, a person in debt cannot be forced to go into prison unless he refuses to pay his/her taxes or offer child support.

What is an acceptable credit score?

According to Experian, a credit score that is more than 700 is good if we base it on a score range of 300-850. Moreover, a score that is greater than 800 is even better. The majority of borrowers generally have a credit score ranging from 600-750. Know that good and high credit scores will keep creditors confident of letting borrowers borrow money.

Getting into debt can indeed be scary, especially when you are not sure about your business idea yet. You know that you don’t want to gamble with what you have left. Nevertheless, for some, debt is still a manageable option. Remember our example earlier? Kevin Plank started his company by getting into debt. Just make sure you plan to repay your debts, so everything will be fine for you in the end.