46+ Sample Income Statements

-

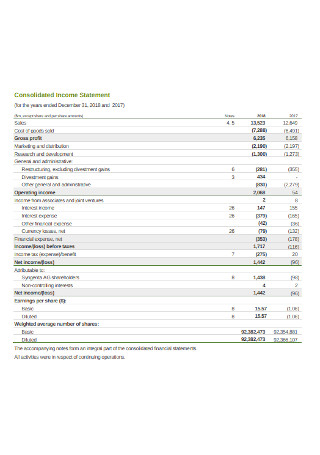

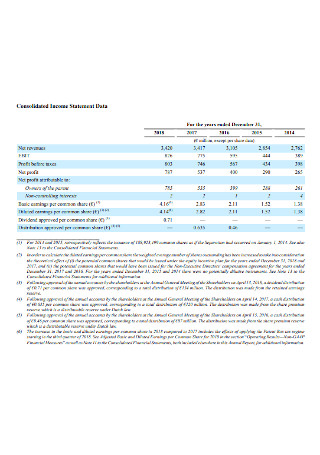

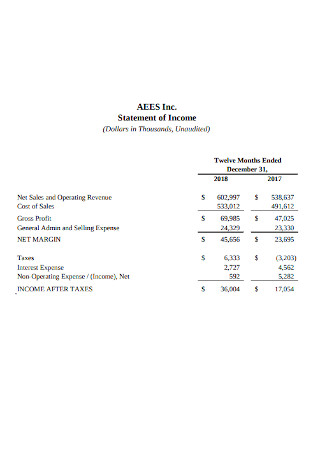

Consolidated Income Statement

download now -

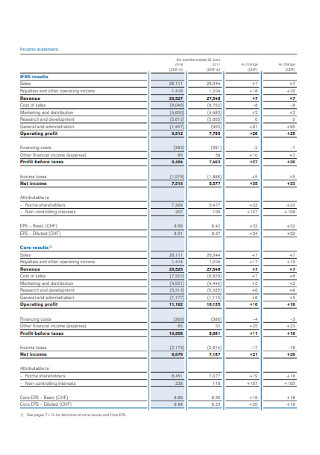

Financial Group Consolidated Income Statement

download now -

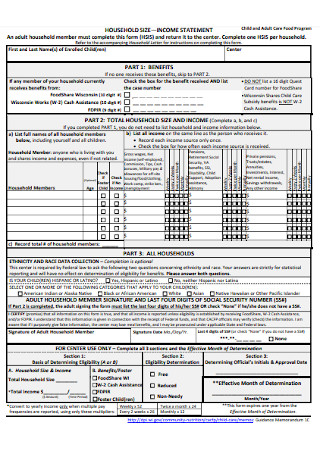

Household Size Income Statement

download now -

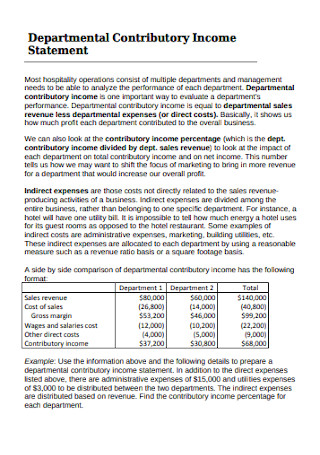

Departmental Contributory Income Statement

download now -

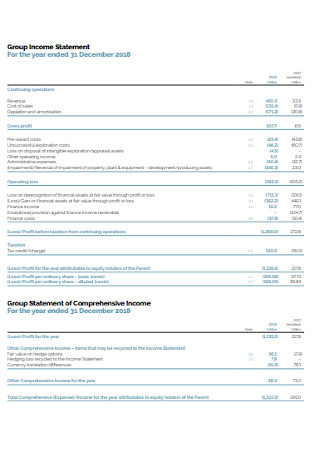

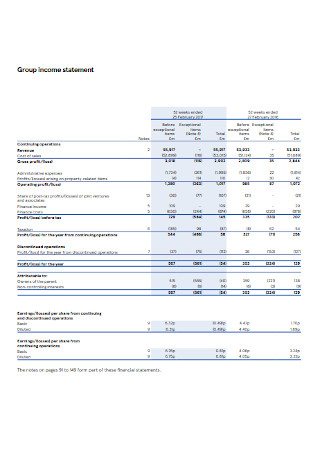

Group Income Statement

download now -

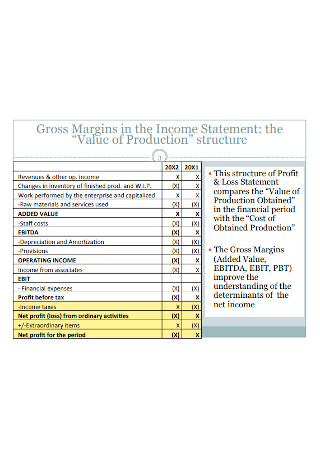

Income Statement Gross Margins

download now -

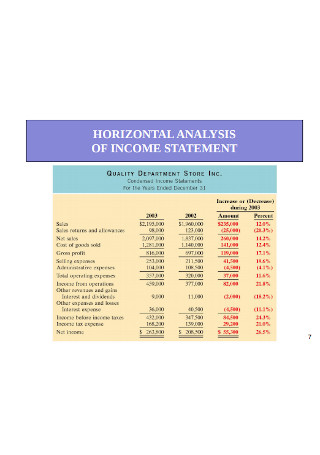

Income Statement Horizontal Analysis

download now -

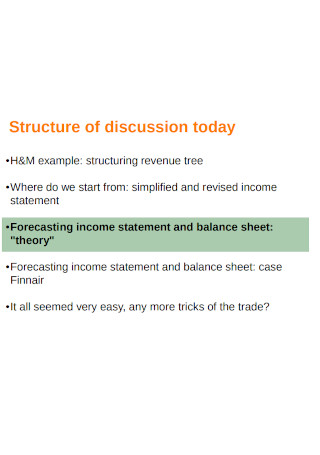

Forecasting Income Statement

download now -

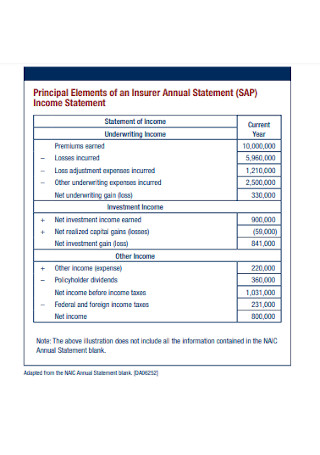

Annual Income Statement Elements

download now -

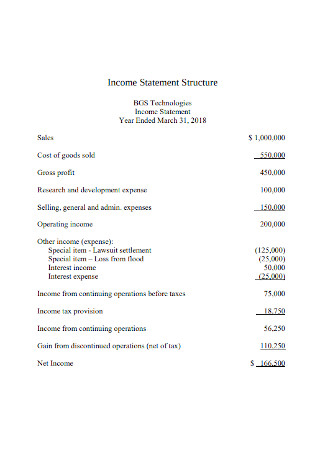

Income Statement Structure

download now -

Annual Family Income Statement

download now -

Income Statement Framework

download now -

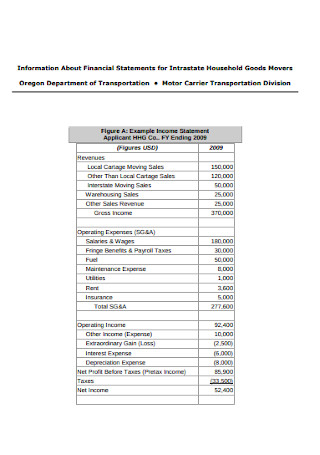

Department of Transportation Income Statement

download now -

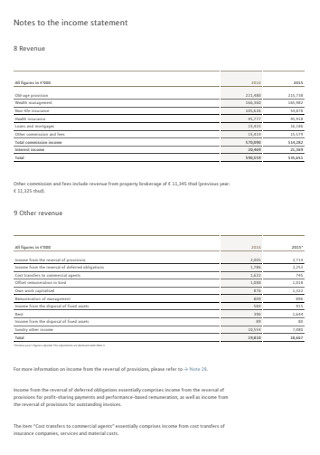

Income Statement Notes

download now -

Income Statement Fraud Indicators

download now -

Income Statement Example

download now -

Company Income Statement

download now -

Year End Income Statement

download now -

Office Income Statement

download now -

Comprehensive Income Statement

download now -

Basic Income Statement

download now -

Source of Income Statement

download now -

Income Statement Survey

download now -

Business Income Statement

download now -

Operating Income Statement

download now -

Consolidated Comprehensive Income Statement

download now -

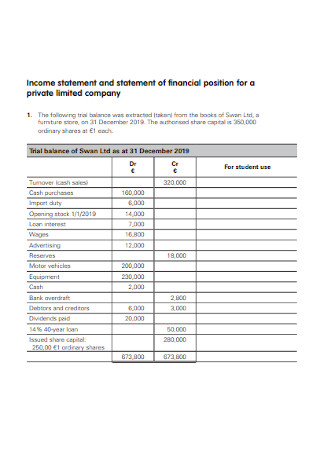

Consolidated Income Statement and Balance Sheet

download now -

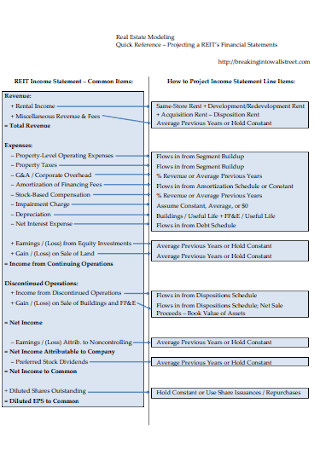

Real Estate Income Statement

download now -

Organisation Income Statement

download now -

Income Statement Validations

download now -

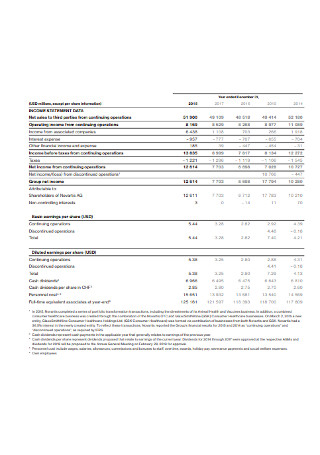

Income Statement Data

download now -

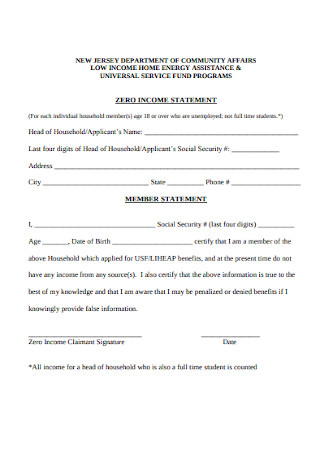

Zero Income Statement

download now -

Annual Income Statement

download now -

Half Yearly Income Statement

download now -

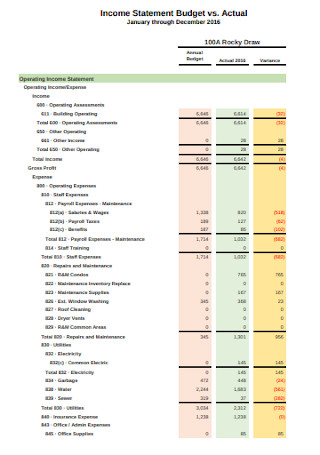

Income Statement Budget vs. Actual

download now -

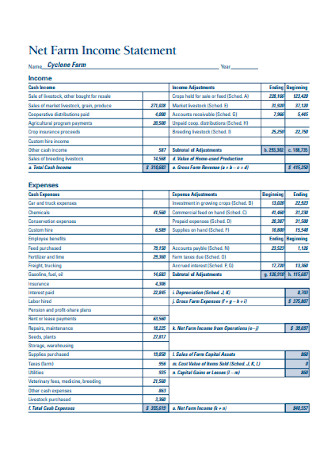

Net Farm Income Statement

download now -

Income Statement Schedule

download now -

Projects Income Statement

download now -

Self Employment Income Statement

download now -

Standard Income Statement

download now -

General Group Income Statement

download now -

Income Statement Report

download now -

Finanical Income Statement Analysis

download now -

Absorption Costing Income Statement

download now -

Hotel Income Statement

download now -

Income Statement Format

download now -

Company Income Statement Template

download now

What Is an Income Statement?

Writing financial statements is a crucial process in every company. In the United States, the Generally Accepted Accounting Principles (GAAP) requires corporate entities to issue four types of financial statements—balance sheet, income statement, cash flow statement, and statement of stockholder’ s/owner’s equity. Aside from laws that mandate business people to create financial reports, these documents bear a great significance in any company. It helps entrepreneurs keep tabs of their business’ financial health. In this guide, we will focus on the fundamentals of an income statement.

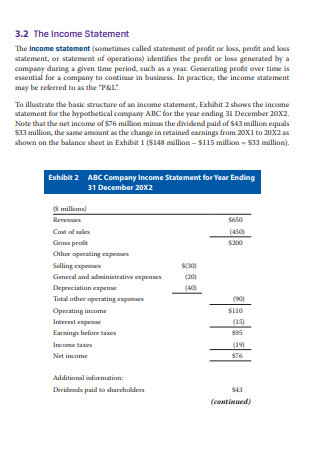

An income statement is a significant financial statement a company issues on consistent and regular intervals. This document provides a summary of a business’s financial activities during a particular accounting period. Moreover, note that a company’s revenues and expenditures are the core focus of an income statement. Although it shows a company’s historical financial status, the data reflected in this document can be a great tool for business owners to make calculated decisions for their company’s future development. An income statement is also referred to as a profit and loss statement, statement of operations, or statement of earnings.

Key Components of an Income Statement

Bear in mind that creating an income statement entails calculating complex numerical data. For this reason, one should make sure that their computations are correct and accurate. Failure to do so would defeat the purpose of the document. Moreover, an income statement would be of no use if it is not complete with the following numerical information:

Why Should You Create an Income Statement?

As featured in an article from Investopedia, data from the Small Business Administration (SBA) revealed that a whopping 80% of small businesses survive during the first year of their operations. When this sounds already good enough, the numbers drastically fell after a five-year mark—noting that only about 45.4% of small businesses continue to operate after a five-year mark. During the 10th year, only one out of three businesses prosper in the industry. This data indicates that,over time, the number of small businesses that fail continually increases. However, this is not true for all businesses. You can avoid this tragic fate by keeping a close eye on your finances so you can come up with a strategic financial plan. Here are other reasons why you should prepare an income statement on a regular basis:

Indicates a Business’ Financial Success

The net income reflected at the end of the income statement will reveal whether or not the business is profitable enough for it to withstand the test of time. A consistent positive net income means that a business is making a profit, which makes it a great avenue for investments. Therefore, the business will become captivating on the eyes of the investors—knowing that there is more guarantee of a return on investment instead of a loss.

Separates Revenues and Expenses

An income statement gives managers and investors a definite picture of the revenues and expenses of a particular company. As a result, they get to compare both figures and measure if the business can make the most out of their financial resources. In addition, the revenues and expenses can be classified based on the different financial resources as well as the company’s various departments. This way, business owners can monitor on which particular aspects they need to improve on so they can minimize expenses and boost sales.

Provides Timely Updates

Unlike other financial reports that companies prepare on a yearly basis, an income statement can cover only a quarter or a month of business operations. A more frequent issuance of this financial statement means that managers and investors will have timely and relevant updates with regards to the profitability of a company. With this data at hand, they can evaluate whether the company has enough resources to cover the costs for the production of goods and rendering of services to the customers. If not, business owners can immediately strategize a concrete course of action to maintain their profitability.

Helps in Decision-Making

An income statement can be your basis for comparison of your company’s financial performance over the course of your business operations. It would be of great help if you compare your past income statements from the current one and see whether there is an upward or downward trend of your business’ profitability. On another note, keep in mind that there is a low probability of guesswork to work. You could never rely on it, especially when your decisions have a huge impact on your company. That is why it would be best to take a look at your income statement and make sound decisions based on the data it provides.

How Would You Prepare an Income Statement?

Oftentimes, dealing with numbers sounds like a lot of burden to individuals, especially when it involves finances. For companies, preparing financial reports such as an income statement can be a tedious task because of the calculations it entails. However, how would you know if your business still has enough financial resources for it to operate on an optimal condition? Would you risk not knowing the financial health of your company just to get away with this task? No, right? So let’s get started! Provided below is a step-by-step guide you can follow so you would not have to create an income statement blindfolded.

Step 1: Acquaint Yourself With the Terms

If it is your first time to create an income statement, it is essential that you have a full understanding of the accounting terms used in the document before you start doing your calculations. Although it seems confusing at first, the computation and analysis will be less of a burden if you are well-versed with the different accounting terms and their definitions. Note that there is a difference between gross profit and revenue as well as expenses and costs—even though they are quite synonymous. Also, there might be a need for you to incorporate acronyms in your income statement so you won’t have to spell out lengthy accounting terms in the document. These financial acronyms include the cost of goods sold (COGS), earnings before interest, taxes, depreciation, and amortization (EBITDA) and operating expenses (OPEX).

Step 2: Specify the Accounting Period

As previously mentioned, the more frequent you prepare an income statement, the more advantages it will bring to a company. However, it is up to you if you create this financial statement on a monthly, quarterly, or yearly basis. We suggest, though, that you avoid creating an income statement that covers more than a year of business operations to save you from the hassle of having to include lots of figures in your document. Aside from it lessens the complexity of your task, a monthly or quarterly income statement enables you to constantly keep tabs of the changes your business has in terms of its profitability.

Step 3: Compile Financial Records

After specifying the accounting period, your document will cover, start gathering the past financial records of your company. These records should provide proof of the sales generated and expenses incurred by the business during a specified period. Presuming that you already have the raw figures needed for computation, the next thing you will do is to transfer it on a software or a spreadsheet for it to be easily accessible.

Step 4: Make Calculations

Your calculation for an income statement starts with the total sales of your business and ends with the net profit. The first step of the process is to calculate the sum of sales of your business. These numbers include both operating revenue and non-operating revenue. Then, find out the total amount of expenses (cost of goods sold and operating expenses) incurred during the specific period your income statement covers. Lastly, deduct the overall expenses from the gross profit for you to come up with the net profit.

Refer to the section where we elaborate on the components of an income statement so you can accomplish the task more easily.

Step 5: Finalize

Aside from the technical aspect of your income statement, you should also see to it that it is presentable and easy to comprehend on the part of the readers. Make sure to label the figures accordingly. Provide headings for every type of revenue and expense in your document to easily classify the cash flow that is directly or indirectly related to the business’ core operations. Also, double-check the data you entered in the document and make sure that they correspond with the financial records you previously compiled.

Step 6: Analyze Results

After the completion of your income statement, take time to analyze the results, and decide whether or not your business needs a change of strategies or plans. You should also gather your historical financial statements so you can compare the results from your company’s prior financial statements.

We have said it once, and we will say it again—keeping track of your company’s financial performance is a vital process you should never neglect. Closely monitoring the financial status of your company, whether small or large scale, is what keeps your business afloat and running.