7+ SAMPLE Finance Statement

-

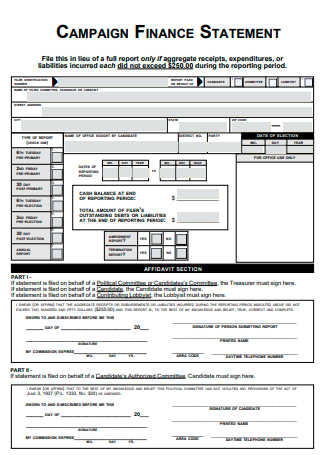

Campaign Finance Statement

download now -

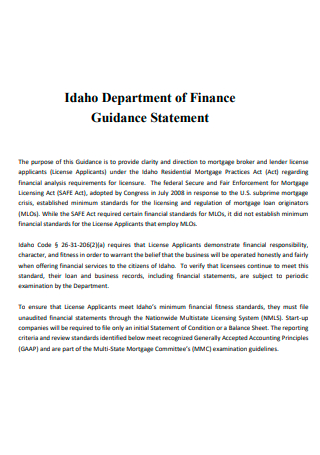

Department of Finance Guidance Statement

download now -

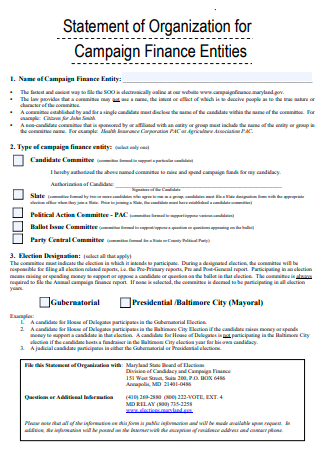

Campaign Finance Entities Statement of Organization

download now -

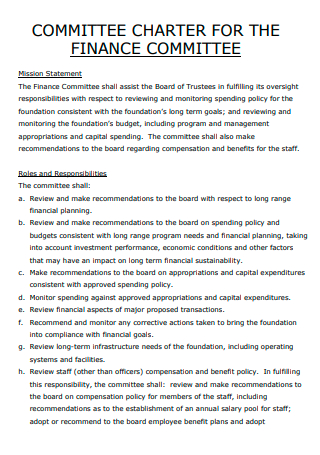

Finance Committee Mission Statement

download now -

Campaign Finance Registration Statement

download now -

Premium Finance Company Annual Statement

download now -

Declaration of Finance Statement

download now -

Finance Statement in DOC

download now

FREE Finance Statement s to Download

7+ SAMPLE Finance Statement

What Is a Finance Statement?

Types of a Finance Statements

How To Write a Finance Statement

FAQs

What are the five components of a financial statement?

What are the basic financial statements that businesses use?

What is the difference between a balance sheet and a trial balance?

What Is a Finance Statement?

A finance statement or a financial statement is a written record that demonstrates the different business activities and the financial performance, status, and reputation of an organization. Financial statements go through auditing from government agencies, accountants, accounting firms, and other financing institutions to ensure the accuracy of their content, including the tax, financing, and investing activities. Investors and financial analysts utilize and rely on the financial data from the financial statements to analyze the performance of an organization. They also produce predictions of the trends and future direction of a business, including its stock price. A business annual report, which is one the most vital resources of reliable and audited financial information, contains the financial statements and reports of the organization. Investors, financial analysts, market analysts, creditors, and credit agencies utilize financial statements to evaluate the financial health and earnings potential of a specific organization. A financial statement is a critical document that a company must create with accuracy to gain the support of government agencies, creditors, and other stakeholders to invest in the company.

According to information coming from the United States Census Bureau and their financial report that targets the manufacturing, mining, wholesale trade, and selected service industries in the United States during the fourth quarter of 2021, these corporations’ after-tax profits result in an estimated amount of up to 271.2 billion US dollars. It means that these industries continue to thrive and that individuals, organizations, and other industries can invest in them and guarantee that their investments will not go to waste.

Types of a Finance Statements

Finance statements or financial statements are a collection of summary-level reports regarding an organization’s financial status, results, positions, and cash flows. Financial statements have three main components, namely, a balance sheet, an income statement, and a cash flow statement. These elements ensure that the persons reading the financial statements, especially stakeholders, have an idea and understanding of how money and any financial assets move around the organization for it to acquire revenue. The section below covers the different types of financial statements with accompanying descriptions for readers to have a better knowledge of them and their relevance to business operations.

How To Write a Finance Statement

At the present age, a specific software can prepare the necessary elements the organization needs in a financial statement that reduces human error while saving time. Using a specific program keeps track of the pending transactions of the business. It includes business spending and profits to automate the process of creating financial statements. Whether the project manager or supervisor opts to use software, it is still necessary to understand how to create and read the document to ensure that readers can draw out conclusions from its contents. The section below provides a helpful guide on how to write a finance statement.

-

1. Determine the Necessary Information that the Financial Statement Must Contain

The first step to creating the financial statement is to think about the information you wish to include in the document and what you want to communicate with your audience. For example, you want your audience to have a visual representation of the amount of money flowing in and out of the organization for a specific period. In this case, you need to provide a cash flow statement to fit your needs and the requirements. Consider the information that you want the document to have in the financial statement to help identify and select the best format for writing the document suitable to your needs.

-

2. Select the Type of Financial Statement the Company Needs

As stated above, there are different types of financial statements that an organization can utilize. Each one provides various perspectives on the financial health and status of the business. Balance sheets detail the assets and liabilities of an organization to gauge equity and profitability. The income statement or the profit and loss statement presents information about the revenues and expenses of the business. An income statement consists of gross profit, operating expenses, non-operating expenses, and net profit. A cash flow statement represents the money that comes in and goes out of the company. The cash flow demonstrates the difference between cash values. It is the best document to represent the changes in the cash flow over a specific period. The cash flow statement must contain the revenue, spending, and total amount for a reporting period. A shareholder’s equity statement comes from a balance sheet to represent the shareholder stock sales and purchases. The values that must be available in the shareholder’s equity statement include common stock, treasury stock, preferred stock, and retained earnings.

-

3. Format the Financial Statement Accordingly

Financial statements are easy to read and understand, presenting all the information clearly and accurately. Computer software incorporates and considers the proper formatting standards into the financial statement to achieve a clear and concise document. Make sure that the font size is large enough for easy reading and small enough to not overwhelm the reader. Incorporating some color into a financial statement makes it more attractive to readers and allows it to emphasize significant information while keeping in mind to be conservative with the colors you use. Make sure to denote each section of the financial statement for readability.

FAQs

What are the five components of a financial statement?

To have a deeper understanding of a financial statement, it is necessary to identify and understand its five components. It includes assets, liabilities, equity, revenue, and expenses.

What are the basic financial statements that businesses use?

The four financial statements that businesses often use for their financing needs include income statements, balance sheets, cash flow statements, and statements of retained earnings.

What is the difference between a balance sheet and a trial balance?

The principal difference between the two is that the trial balance contains the ending balance for each account, while the balance sheet summarizes the amount balances for each item line. There is also a standard format for writing a balance sheet compared to a trial balance. Balance sheets serve external purposes, while trial balances are mostly internal, used by the accounting department and organization auditors.

Financial statements are vital documents that businesses use when interacting, communicating, and collaborating within and outside the organization. Since there are various types of financial statements, the accounting and project management teams must know the most appropriate document for given situations. Make sure that the information that you provide in the financial statement you choose is appropriate to the requirements of clients and stakeholders. The content of the finance statement must be easy to understand and interpret. Construct a comprehensive finance statement by downloading a template from the 7+ SAMPLE Finance Statement in PDF | MS Word, only from Sample.net.