Power of Attorney Samples

-

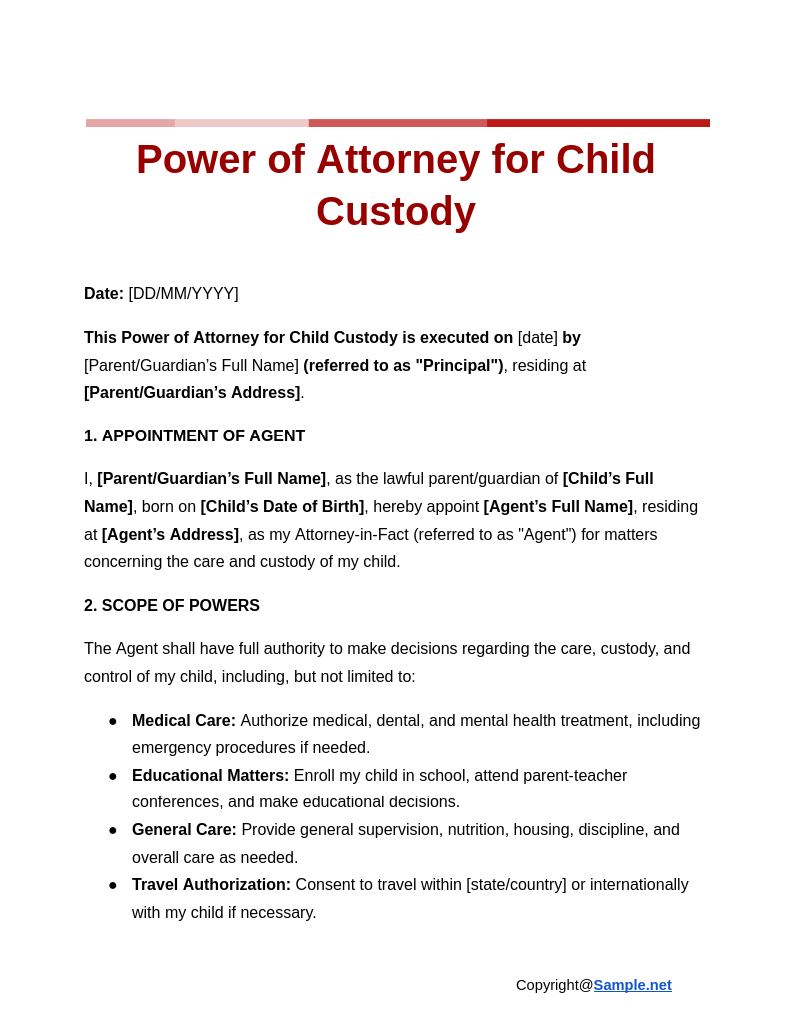

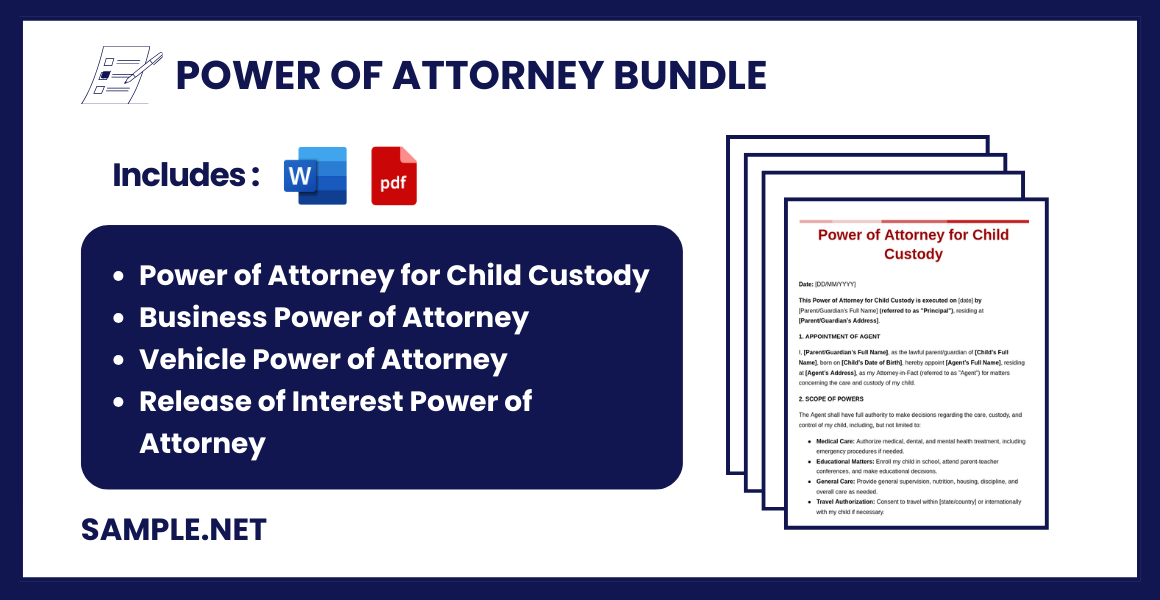

Power of Attorney for Child Custody

download now -

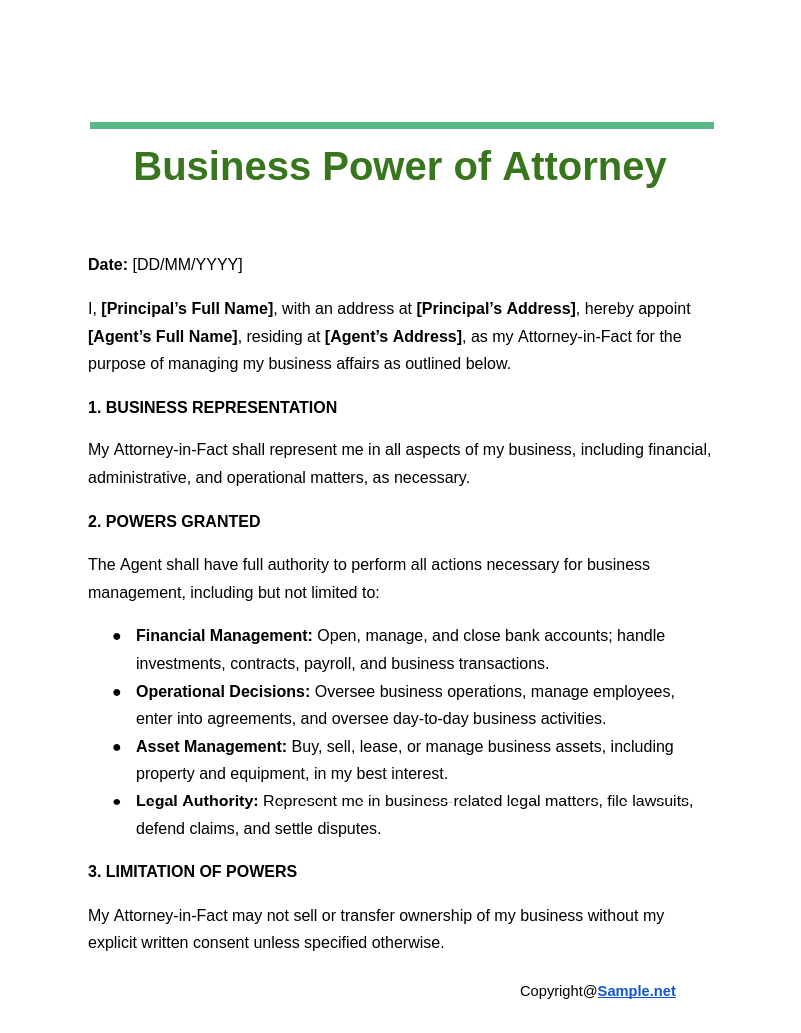

Business Power of Attorney

download now -

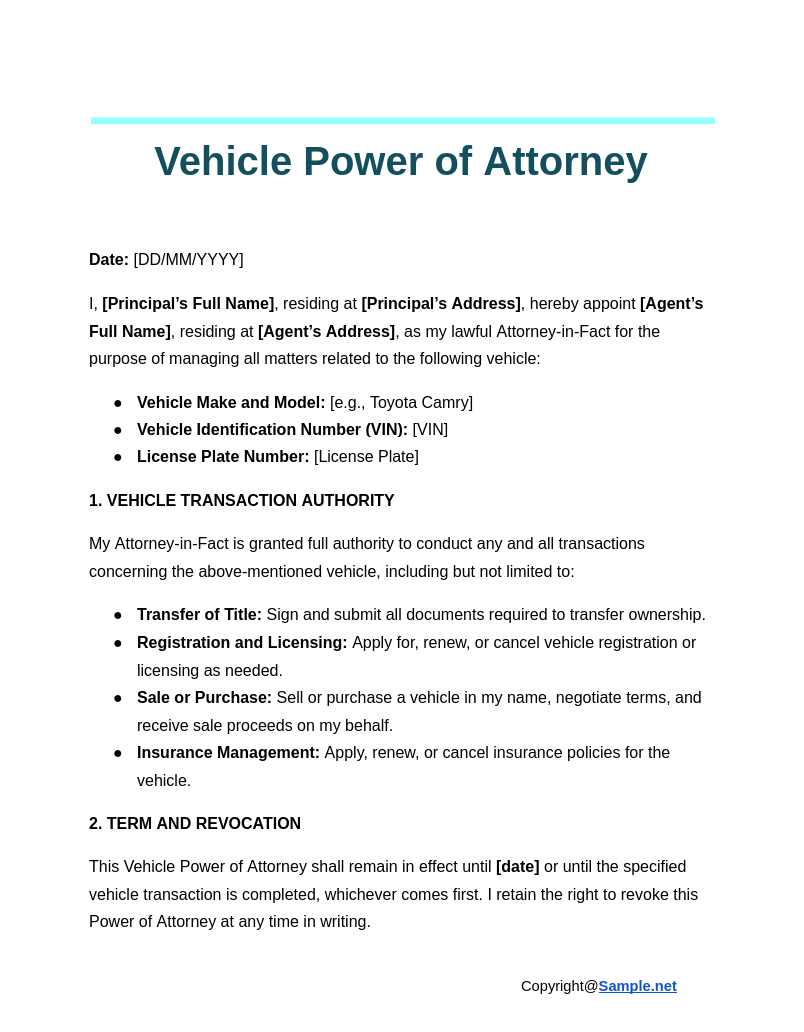

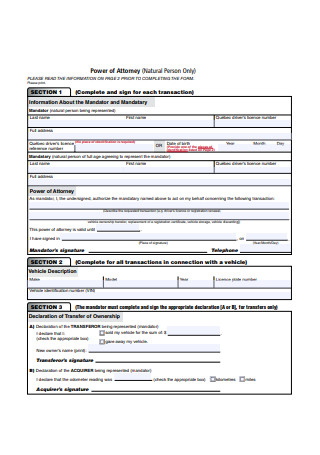

Vehicle Power of Attorney

download now -

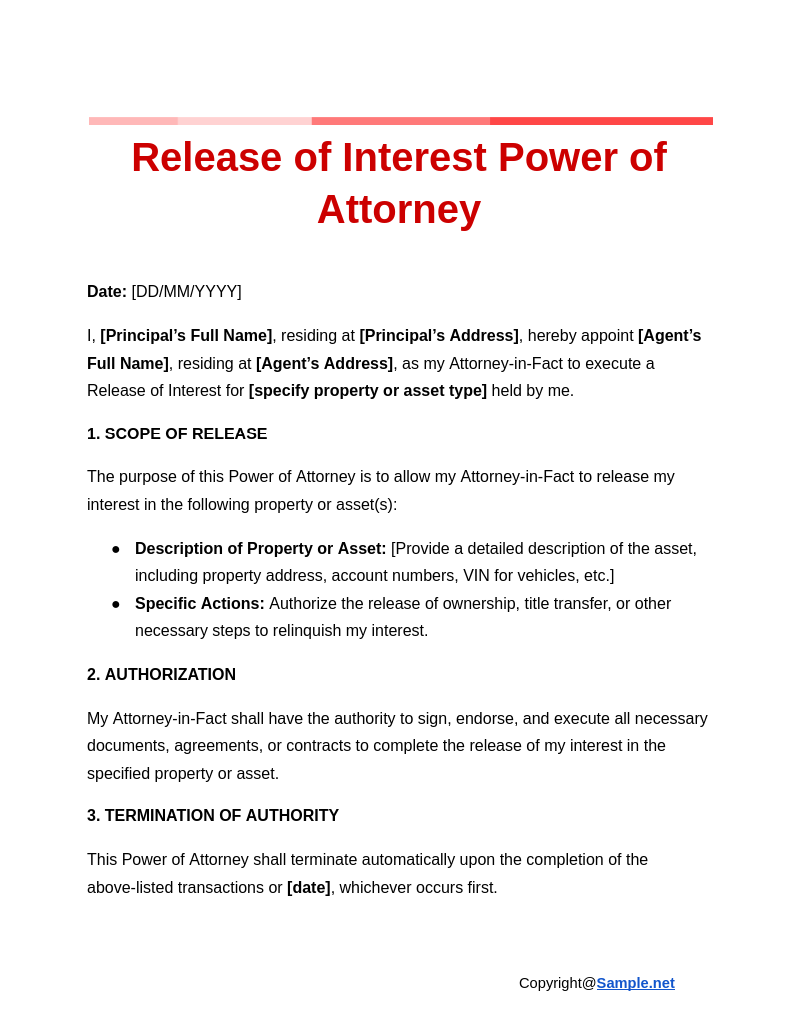

Release of Interest Power of Attorney

download now -

Power of Attorney Form

download now -

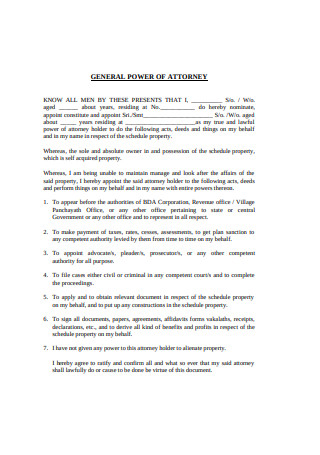

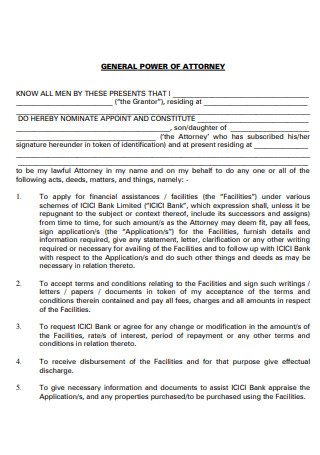

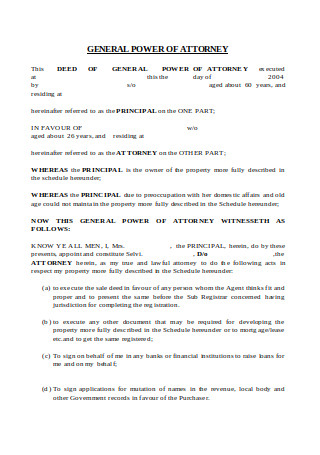

General Power of Attorney

download now -

Power of Attorney Sample

download now -

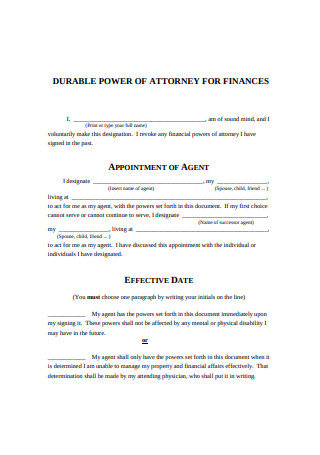

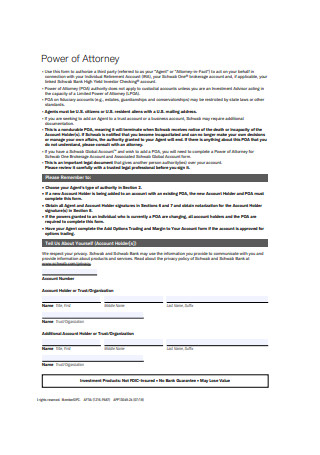

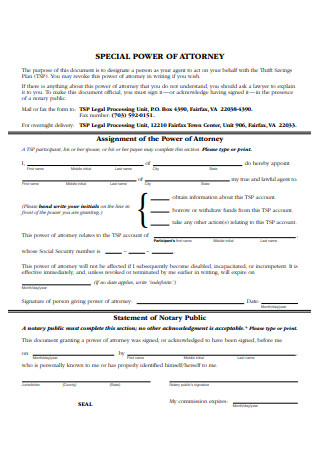

Power of Attorney for finances

download now -

Basic Power of Attorney Form

download now -

Real Estate Power of Attorney

download now -

Power of Attorney Format

download now -

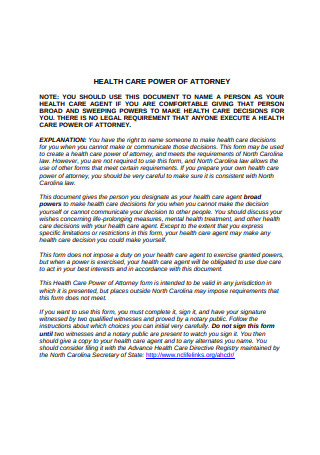

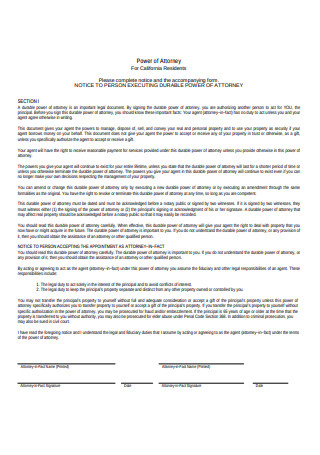

Health Care Power of Attorney

download now -

Sample Power of Attorney

download now -

General Power of Attorney Sample

download now -

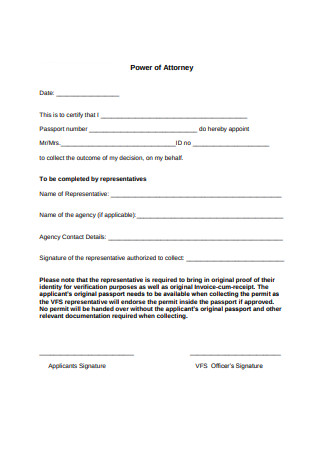

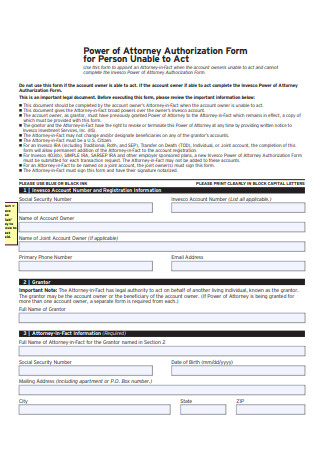

Power of Attorney Authorization Form

download now -

Power of Attorney Example

download now -

Basic Power of Attorney Format

download now -

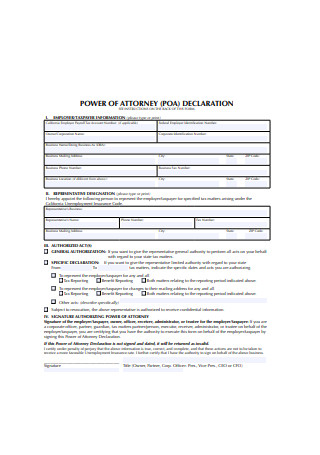

Power of Attorney Declaration

download now -

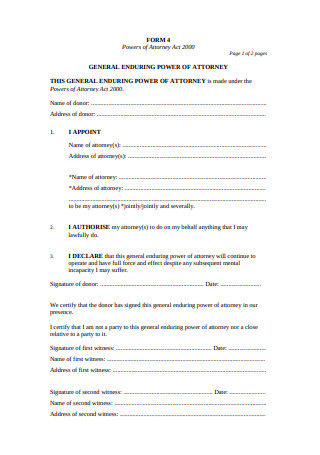

Standard Power of Attorney

download now -

Power of Attorney Registration

download now -

Sample Power of Attorney Format

download now -

Power of Attorney for Property Management

download now -

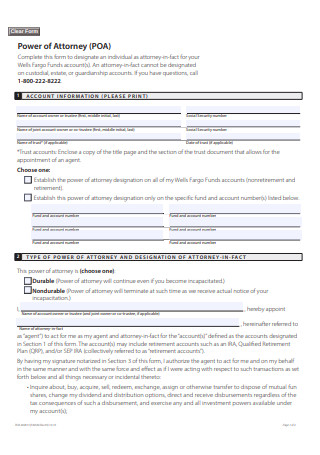

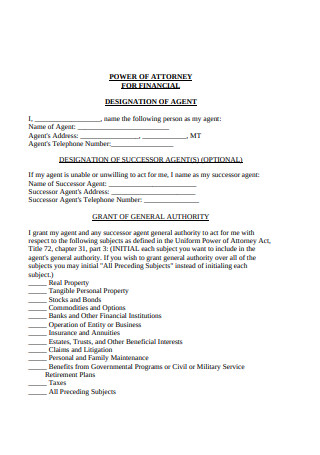

Power of Attorney for Financial

download now -

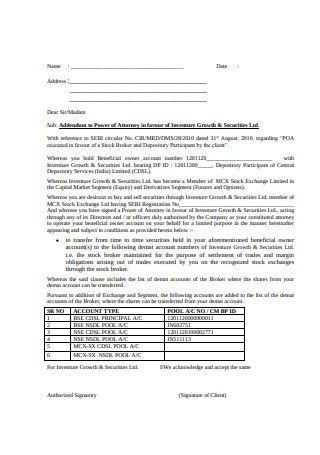

Adendum to Power of Attorney

download now -

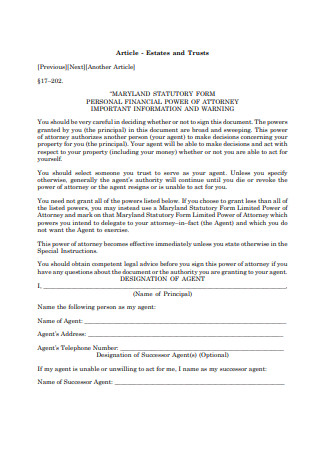

Personal Financial Power of Attorney

download now -

General Power of Attorney Form

download now -

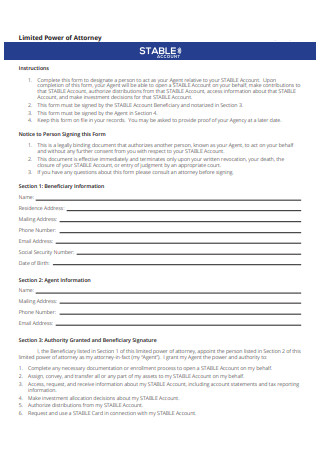

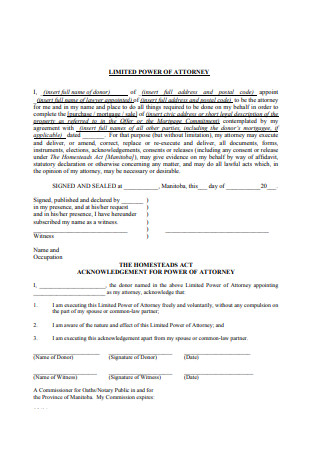

Limited Power of Attorney

download now -

Formal Power of Attorney

download now -

Simple Power of Attorney Form

download now -

Standard Power of Attorney Format

download now -

Limited Power of Attorney Sample

download now -

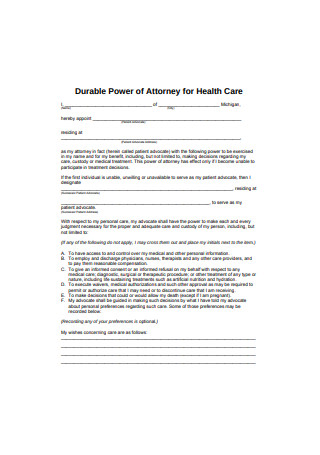

Durable Power of Attorney for Health Care Form

download now -

Simple Power of Attorney Format

download now -

Standard Power of Attorney Example

download now -

Medical Power of Attorney

download now -

Sample Medical Power of Attorney

download now -

Printable Power of Attorney

download now -

Durable Power of Attorney for Health Care

download now -

Durable Power of Attorney Sample

download now -

Standard Power of Attorney Sample

download now -

Durable Special Power of Attorney

download now -

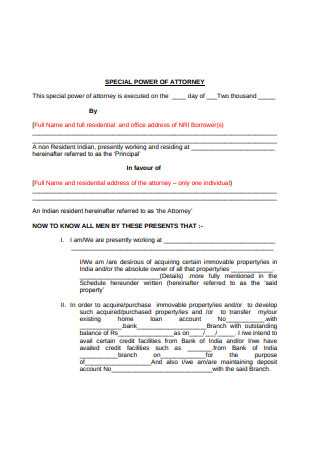

Special Power of Attorney

download now -

Power of Attorney Application Form.

download now -

Simple Power of Attorney Example

download now -

General Power of Attorney Example

download now -

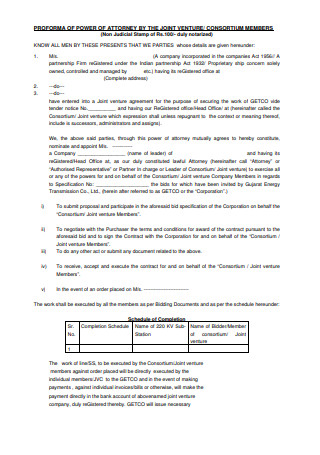

Power of Attorney for Sale

download now -

Sample Power of Attorney Form

download now -

Elctronic Power of Attorney Template

download now

FREE Power of Attorney s to Download

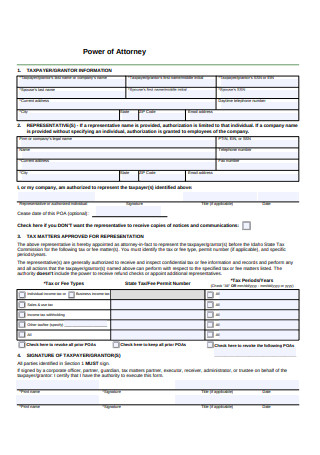

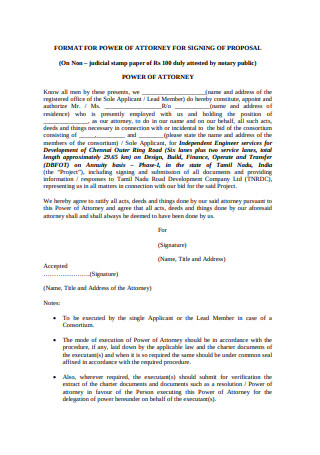

Power of Attorney Format

Power of Attorney Samples

What is a Power of Attorney?

The Types of Power of Attorney

How to Write a Power of Attorney

FAQS

Who can be an agent in a POA?

Does a POA remain effective after death?

How does a Power of Attorney differ from a guardianship?

What limitations can be included in a POA?

How can I ensure my POA is legally binding in multiple states?

What happens if a POA is misused?

Download Power of Attorney Bundle

Power of Attorney Format

Date: [DD/MM/YYYY]

This Power of Attorney is made on [date] by [Full Name of Principal], residing at [Address of Principal].

1. APPOINTMENT OF AGENT

I, [Principal’s Full Name], hereby appoint [Agent’s Full Name], residing at [Agent’s Address], as my lawful attorney-in-fact (referred to as “Agent”) to act on my behalf in connection with the matters set forth below.

2. POWERS GRANTED

My Agent shall have full power and authority to undertake and perform the following acts on my behalf:

- Financial Transactions: Managing bank accounts, investments, real estate, and other assets.

- Real Estate Transactions: Buying, selling, leasing, and managing property.

- Legal Representation: Representing me in legal matters, including filing lawsuits and defending claims.

- Healthcare Decisions: Making healthcare-related decisions if I am unable to do so.

This list of powers is not exhaustive, and the Agent has the authority to act in all necessary matters in my best interest.

3. DURATION

This Power of Attorney shall become effective on [effective date] and shall remain in effect until [termination date], unless revoked earlier by me in writing.

4. REVOCATION

I reserve the right to revoke this Power of Attorney at any time by providing written notice to my Agent.

5. INDEMNIFICATION OF AGENT

I agree to indemnify and hold harmless my Agent from all claims, losses, expenses, or damages arising out of actions taken in good faith while acting within the scope of this Power of Attorney.

6. SIGNATURE AND ACKNOWLEDGEMENT

In Witness Whereof, I have executed this Power of Attorney on the date set forth above.

Principal’s Signature: __________________________

Date: [DD/MM/YYYY]

Agent’s Signature: __________________________

Date: [DD/MM/YYYY]

Witness 1 Name: __________________________

Signature: __________________________

Date: [DD/MM/YYYY]

Witness 2 Name: __________________________

Signature: __________________________

Date: [DD/MM/YYYY]

[Notarization (if required by law in your area)]

What is a Power of Attorney?

A Power of Attorney (POA) is a formal, legally binding authorization that grants an appointed agent the power to act on behalf of the principal in various matters, typically including financial, medical, and legal responsibilities. This delegation can be either general or specific, depending on the principal’s requirements and wishes. You can also see more on Limited Power of Attorney Forms.

According to Nerd Wallet, among the duties that you can expect agents to contend with include: banking duties, business management, asset distribution, the filing of taxes, contributions to charity, and the handling of any form of government benefits, among others. When considering people to serve as agents, be sure that you pick those who are reliable and unlikely to abuse their power and position. It was AARP that reported that approximately 55% of financial abuse done to the elderly are by untrustworthy power of attorney agents. MarketWatch takes this even further with its report that elderly Americans are known to lose up to $2.9 billion on a yearly basis because of said financial abuse.

The Types of Power of Attorney

A power of attorney is not a singular type of document as you already know. Different intentions necessitate different types. The list compiled below already includes a brief description for each type to enlighten those who wish to know more about them. You can also see more on Revocation of Power of Attorney.

How to Write a Power of Attorney

Once you have determined that you are in need of a POA, the next step is to acquire one. It is worth noting that you are fully capable of creating one on your own, provided you have the right set of instructions to guide you. Pay close attention to the ones detailed below to experience a much easier and faster creation process. You can also see more on Company Affidavit.

Step 1: Determine the Agent

Your first act as a would-be grantor would be to decide on who gets to serve as your agent. This is a highly significant decision to make and should not be made lightly in the least. It can be any kind of person, as long as you’ve got enough confidence in their ability to execute your vision for you. You may turn to family, friends, spouses, and even business associates. Before picking any of them, be sure to weigh in the pros and cons of each person.

Step 2: Decide When the Agent is to Act on Your Behalf

After you have finally chosen the person whom you think is best suited for the role of an agent, the next decision you must face is when he or she is to act on your behalf. This step will also be influenced by your reasons for acquiring a power of attorney in the first place. You can also see more on Legal Letters.

Step 3: Determine the Specific Details

In addition to the specific time that your agent gets the authority to act on your behalf, there are also specific details to consider including in your power of attorney. This may include what the required acts and duties are, how long he or she is to perform said duties, what the limits of his or her authority are, and more. Decide on each one before committing them to the actual document.

Step 4: Write the Caption of Your Power of Attorney

In writing the document proper, the thing you need to get out of the way as soon as possible would be the writing of the caption. Place it at the top of the document so that any reader won’t miss it in the least.

Step 5: Write All the Things Your Agent has the Authority to Do

Look back at step three and you should be able to perform this particular step with ease. Having determined the specifics, this is the part where you list down all of the things that your appointed agent is going to do. Nothing more, nothing less. Be as detailed as possible to ensure that there won’t be any kind of confusion in regards to the duties. You can also see more on Affidavit of Payment.

Step 6: Specify the Date or Circumstance When this Becomes Effective

This is yet another step that dates back to the third step and even the second one, this last thing you need to do is write down the specific date in which your authorization of power to your agent becomes official. If there is no specific date singled out by you, or if the authorization is more circumstantial, then be sure to specify what circumstances will need to come to pass.

The Power of Attorney is a crucial legal tool for ensuring that your affairs are managed according to your wishes, even when you cannot act yourself. By granting this authority to a trusted individual, you gain peace of mind, knowing your interests are safeguarded and your responsibilities efficiently handled. You can also see more on Sample Affidavit.

FAQS

Who can be an agent in a POA?

An agent can be anyone the principal trusts, often a family member, friend, or legal professional willing to act in the principal’s best interest.

Does a POA remain effective after death?

No, a Power of Attorney ceases upon the principal’s death, and an executor or estate manager then takes over.

How does a Power of Attorney differ from a guardianship?

A Power of Attorney is granted voluntarily by a mentally competent individual, giving someone the authority to act on their behalf. Guardianship, on the other hand, is court-appointed, typically when an individual is incapacitated and unable to make decisions themselves. POA offers more personal control than guardianship, which requires legal proceedings. You can also see more on Advance Directives.

What limitations can be included in a POA?

A Power of Attorney can be tailored to limit the agent’s powers to specific tasks, timeframes, or decisions, such as only handling property transactions. Limiting powers provides control while still granting essential authority for defined tasks.

How can I ensure my POA is legally binding in multiple states?

To be effective in various states, consult a lawyer to draft a POA that complies with state laws where you may need it enforced. Some states may require re-execution or additional notarization to recognize the POA’s validity. You can also see more on Affidavit of Transfer.

What happens if a POA is misused?

Misuse of a POA, such as unauthorized financial actions, can lead to legal consequences for the agent. The principal or their family can seek court intervention, and, if necessary, the agent can be held liable for damages or face criminal charges. Properly selecting a trustworthy agent and setting specific limits can reduce this risk.