34+ Sample Personal Financial Statement Templates & Forms

-

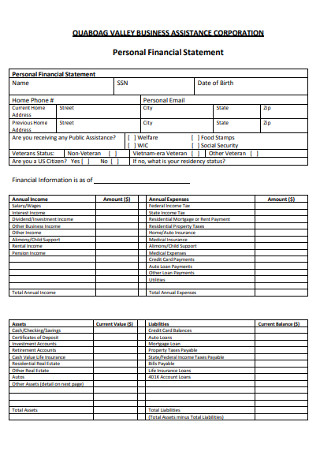

Personal Small Business Financial Statement

download now -

Confidental Personal Financial Statement

download now -

Personal Real Estate Financial Statement

download now -

Personal Company Financial Statement

download now -

Personal Bank Financial Statement

download now -

Personal Business Administration Financial Statement

download now -

Personal Private Banking Financial Statement

download now -

Personal Trust Financial Statement

download now -

Verified Personal Financial Statement

download now -

Personal Financial Statement Worksheet

download now -

Personal Credit Financial Statement

download now -

Personal Financial Department of Banking Statement

download now -

Sample Confidential Personal Financial Statement

download now -

Nominee Personal Financial Statement

download now -

Guarantor Personal Financial Statement

download now -

Personal Department of Financial Institutions Statement

download now -

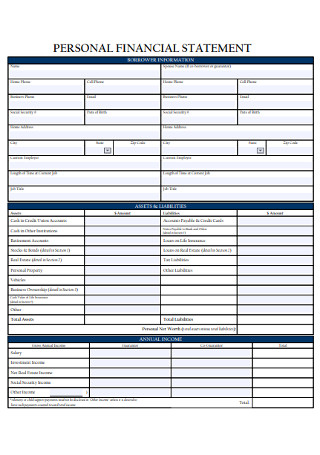

Personal Borrower Financial Statement

download now -

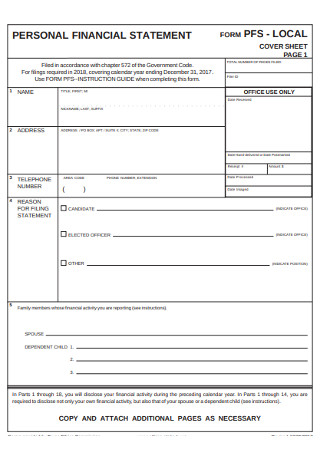

Personal Financial Statement Cover Sheet

download now -

Personal Corporation Financial Statement

download now -

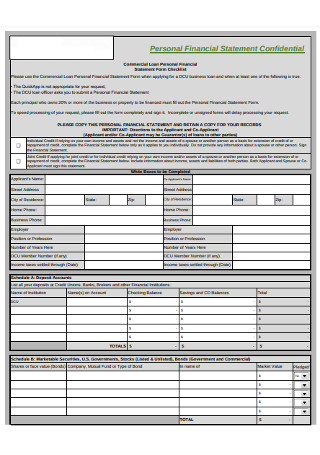

Commercial Loan Personal Financial Statement Form Checklist

download now -

Individual Personal Financial Statement

download now -

Personal Investors Financial Statement

download now -

Standard Personal Financial Statements

download now -

Consumer Personal Financial Statement

download now -

Sample Completed Personal Financial Statement

download now -

Personal Financial Statement Addendum

download now -

Confidential Personal Financial Statement

download now -

Personal Foundation Financial Statement

download now -

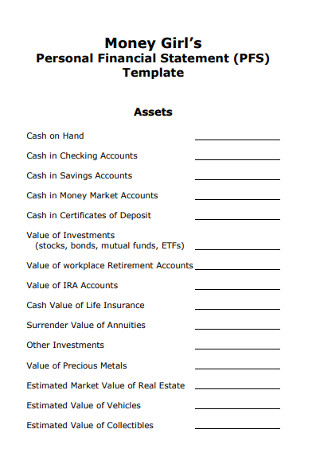

Personal Money Financial Statement

download now -

Basic Personal Financial Statement

download now -

Simple Personal Financial Statement

download now -

Personal Financial Statement in DOC

download now -

Evaluating Personal Financial Statements

download now -

Personal Loan Financial Statement

download now -

Personal Bank Financial Statement Template

download now

What Is a Personal Financial Statement?

A personal financial statement should be able to help you determine the state of your financial health. Apart from the net worth, simplified personal financial statements should only contain the breakdown of your personal assets and liabilities that are not related to any business assets or liabilities. In getting the net worth, the formula is simply assets minus your liabilities. Assets, both personal and investment, include savings and checking account balances, and retirement account balances. Liabilities are what you owe from individuals and institutions such as credit card payments and loans. An ideal personal financial statement should also have a specific set of disclosures. Such disclosures include the methods used to get the values of assets and liabilities, the details of joint arrangements with other parties, the methods and assumptions to get the income tax, and the date when accounts receivable and debts payable are due.

Personal financial statements play a key role when you would want to apply for loan. This type of statement is a document that enumerates what you own and owe. Along with it are documents or records that your lender might find informative. Your lenders will surely grant your loan request if they will find out that you were not only able to provide an informative financial statement but you also have a positive and impressive financial situation.

Why Use a Personal Financial Statement?

If you find the need to set your finances straight, keeping a personal financial statement should be convenient for you. This type of financial statement can help you reach all of your financial goals. And if you are a young professional just starting in the corporate world, the most basic personal financial statement can help you put your finances to a good start. Other than that, here are other reasons why you should make use of a personal financial statement.

How to Prepare a Personal Financial Statement

Do you want to know your current financial standing? One of the most basic things you have to do is to prepare your own personal financial statement. If you want to run your own business soon, travel overseas, or just be financially free, it’s never too late to come up with your own personal financial statement to make all of your financial plans a reality. That said, start coming up with your own personal financial statement today by using these easy-to-follow steps below.

Step 1: List Your Personal Information.

Before you start listing down your assets and liabilities, see to it that you write down your personal information first at the topmost part of your personal financial statement. Such information includes your full name, address, contact number, social security number, birth date, and dependents. Also include details about your occupation, length of time working for the company you’re working for, name and address of the company, monthly payment, estimated yearly living expenses, and whether you own or rent. See to it that you also include the date when you have created your personal financial statement.

Step 2: Determine Details Regarding Your Assets and Liabilities

Without these elements, your personal financial statement can never materialize. Ideally, you need to determine the most recent balance details regarding your assets and liabilities. Your assets may include your stocks, the value of your properties, your checking or savings account balance, and retirement accounts. If you have no idea or still doubting about your assets’ value, just go with the most reasonable amount you can think of. Your liabilities may include the details regarding the outstanding mortgage balance, latest loan statement, and, of course, your contingent liabilities. As part of covering your liabilities, it is also essential to conduct a credit report to know your credit score.

Step 3: Create a Balance Sheet

Now that you have already gathered details of your assets and liabilities, you can soon come up with a balance sheet. The balance sheet of your personal financial statement should effectively present your assets and your liabilities for you and your lender’s convenience. Create three columns. The first column contains the list of your assets, your liabilities at the column right next to your list of assets, and lastly, your net worth.

Step 4: Calculate Your Net Worth

As mentioned, to get your net worth, the formula is as simple as getting the difference between your assets and liabilities. In the event that you get a negative result, this means that the number of your liabilities weigh more than your assets. You might get tempted to alter the details of your liabilities just so your personal financial statement will look like you own more than you owe people. Sure, your loan might possibly be granted, but then your financial reality will not be easy to change and in the end, your most recent loan will only add to your list of liabilities. Also, see to it that you have thoroughly calculated your actual net worth.

Stepp 5: Create an Income Statement

Your income statement is a crucial element in your personal financial statement since this shows your capability to acquire the assets you have written in your balance sheet as well as your capability to pay off any of your liabilities. An ideal income statement usually includes details of how much your income is. Other than that, your income statement also contains details of your expenses. Your expenses may include your rent, utilities, and other bills that you are obliged to pay within a certain period. Once you have already listed the details of your income and expenses, you can already get your total net income.

Step 5: Gather Supporting Records and Documents

Although this is not a part of your actual personal financial statement, it is still vital that you accomplish this step. Even if you have carefully and effectively organized the details regarding your assets and liabilities, it is also crucial to secure any proof that supports what you have indicated in your personal financial statement. That is why it is crucial to include already documents or records that you can readily show and share with your lender. It is in this way that you make it quick and convenient for you to get your loan request granted.

The Dos and Don’ts of Personal Finances

Managing your personal finances is the most straightforward step you can start with upon achieving financial literacy. And just like learning a new foreign language, there are some dos and don’ts that you need to be aware of to ensure your mastery. That said, take some notes from our list of dos and don’ts to be further guided and to come up with a favorable personal financial statement.

Dos

1. Do prioritize paying yourself.

By paying yourself, this means that you should allot something for your savings as this is your asset for your future. If you find it challenging to do so, consider your self as one of your bills or debts so that you will feel compelled and obliged to pay for it regularly.

2. Do establish a clear set of financial goals and a clear way of determining progress.

You surely want to be successful in managing your personal finances. It is vital to set clear financial goals that you can benefit from. See to it that your goals are SMART or specific, measurable, attainable, relevant, and time-based to ensure its success. But other than setting financial goals, it is also highly essential to have a clear way of how you can manage and determine your progress towards achieving these financial goals.

3. Do secure a fund for future emergencies

Life consists of uncertainties, and because of that fact, you must secure your emergency fund. By having emergency funds, you no longer need to borrow money from your relatives, friends, or your bank in the event of an emergency. Any expenses coming from the unexpected events of your life can negatively impact your current financial standing at the time of the emergency. By having a ready emergency fund, you will no longer have to resort to debts or loans because you can already cover all the expenses by yourself. It is ideal that separate your savings from your emergency funds.

4. Do track your spending habits.

If you want to ensure that you have an excellent financial status, do not merely focus on savings alone, but you also need to look into your spending habits. No matter how you save up, your bad spending habits can pull you down anytime. Because of this, you must keep track of how you spend your money. From small convenience store purchases to big-time grocery shopping, jot it down into your tracker so you would know your spending habits and know what practices you need to cut down or maintain.

5. Do be realistic when putting your personal financial statement.

When coming up with your financial statement, it is essential to be realistic, especially when it comes to determining your asset’s market worth. Upon doing so, avoid attaching any personal and emotional value that leads you to make the mistake of doubling your asset’s worth.

Don’ts

1. Don’t miss out on your credit card obligations.

It is essential that you fully commit to your credit card obligation. Any negligence can severely affect your credit score, and you know how important this score is upon any loan application. Failure to meet your obligations before or on the due dates, there will be penalties that will cost you a lot, and of course, there will be a negative impact on your credit score.

2. Don’t exhaust a large percentage of your income on rent.

Are you among those people who spend most of their income on rent alone? According to a USA Today report, younger adults spend about 45% of their income in their first ten years of working, leaving them little to nothing for savings or future family building. If you are still about to find a place to rent, make sure not to spend beyond your means, or else you will find it difficult to set aside something for your emergency fund and savings.

3. Don’t live on the high-interest credits.

Keeping a good credit score sounds good, but if you spend nearly half of your monthly income in paying off your debt because of high interests, then you should change some things. Avoid any high-interest credits as much as possible, especially if you’re still starting to live on credit.

4. Don’t miss reading any details printed small.

Before you make any financial commitments such as credit cards, loans, and investments, ensure that you read every single fine print so you wouldn’t blindly get into obligations that have a lot of conditions. You must thoroughly understand the terms and conditions of whatever financial commitment you’re getting into; otherwise, you will find yourself struggling to make ends meet.

Personal financial statements are tools that you can use in keeping track of your net worth, spending habits, and overall personal financial management performance. If you find that you have a negative financial management performance, consider the use of any of our personal financial statement templates and examples uploaded here to get you started. With the use of any of these samples, you can quickly assess how you spend, how you can adjust unfavorable habits, how you can increase your number of assets, and how you can decrease and pay off your liabilities. Soon enough, with the help of this tool, you can finally achieve the financial security you’ve always wanted and the rest of your financial goals.