49+ Sample Escrow Agreements

-

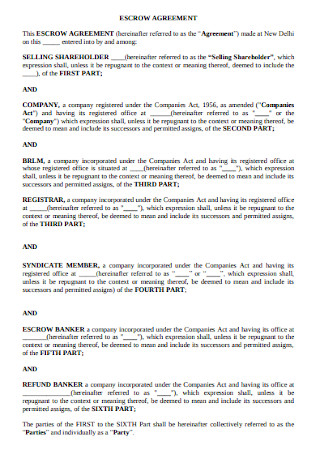

Selling Shareholder Escrow Agreement

download now -

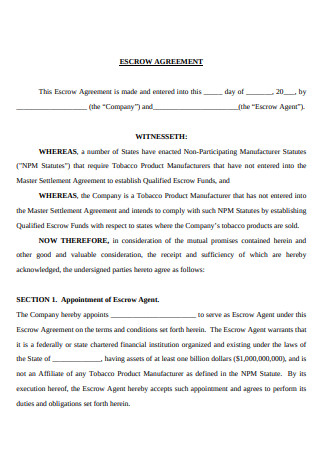

Escrow Agent Agreement

download now -

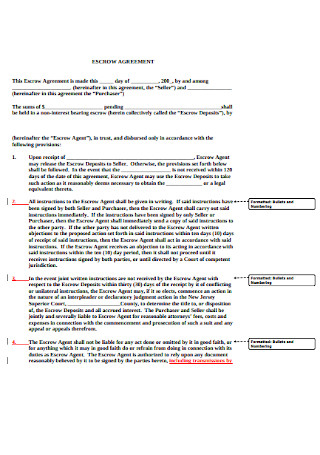

Seller and Purchaser Escrow Agreement

download now -

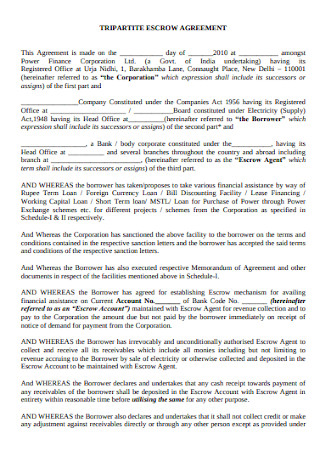

Tripartite Escrow Agreement

download now -

Company and Agent Escrow Agreement

download now -

Limited Company Escrow Agreement

download now -

Sample Escrow Agreement

download now -

Default Escrow Agreement

download now -

Property Escrow Agreement

download now -

Installment Purchase Escrow Agreement

download now -

Contractor Escrow Agreement

download now -

Manufacturing Escrow Agreement

download now -

Banking Corporation Escrow Agreement

download now -

Model Escrow Agreement

download now -

Award Escrow Agreement

download now -

Project Escrow Agreement

download now -

Escrow Agreement Worksheet

download now -

Professional Escrow Agreement

download now -

Performance Escrow Agreement

download now -

Escrow Agent, Buyer and Seller Agreement

download now -

Draft Escrow Agreement

download now -

Mining Corporation Escrow Agreement

download now -

Environmental Escrow Agreement

download now -

Agency Escrow Agreement

download now -

Trust Services Escrow Agreement

download now -

Basic Escrow Agent Agreement

download now -

University Escrow Agreement

download now -

Shares Escrow Agreement

download now -

Escrow Agent and Company Agreement

download now -

Securities Offering Escrow Agreement

download now -

Earnest Money Escrow Agreement

download now -

Formal Escrow Agreement

download now -

Securities Department Escrow Agreement

download now -

Business Impact Escrow Agreement

download now -

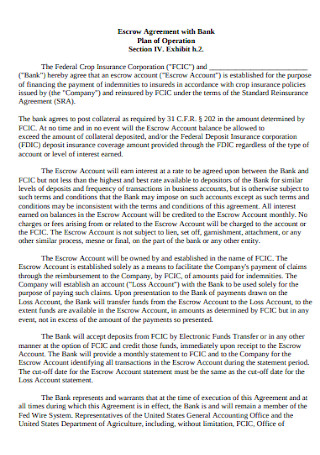

Bank Escrow Agreement

download now -

Escrow Agreement Example

download now -

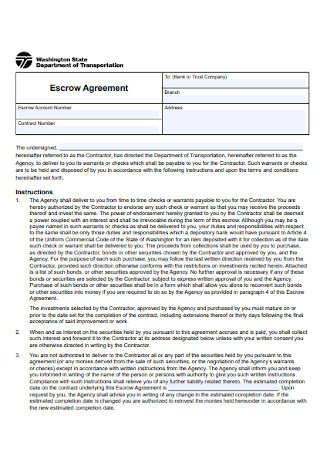

Transportation Department Escrow Agreement

download now -

Sample Escrow Account Agreement

download now -

Finance Agency Escrow Agreement

download now -

Interest Bearing Escrow Agreement

download now -

Escrow and Security Agreement

download now -

Site Plan Landscaping Escrow Agreement

download now -

University Legal Escrow Agreement

download now -

Construction Escrow Agreement

download now -

Financing Authority Escrow Agreement

download now -

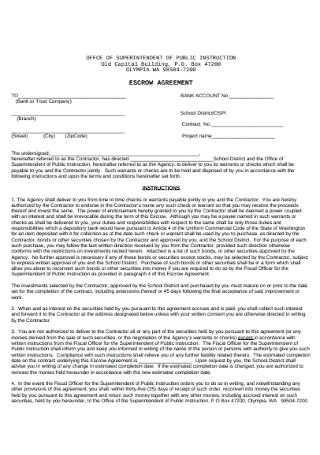

School Authorized Escrow Agreement

download now -

Escrow and Deposit Account Control Agreement

download now -

Standard Escrow Agreement

download now -

Escrow and Deposit Agreement

download now -

Printable Escrow Agreement Template

download now

FREE Escrow Agreement s to Download

49+ Sample Escrow Agreements

What is an Escrow Agreement?

Escrow Agreement: The Processes Involved

How to Draft of an Enforceable Escrow Agreement

FAQs

How much is the fee for an escrow agent?

Is money from an escrow account withdrawable?

How long does an escrow agreement last?

How do you terminate an escrow agreement?

Is opening an escrow account compulsory?

What is an Escrow Agreement?

In most real estate business deals, an escrow agreement serves as a legal paper that lays out the terms and conditions for the parties involved in a transaction. When a buyer and a seller decides to keep their deed, property, or money in escrow, they are legally bound to fulfill their duties written in the escrow contract before the assets are going to be released to them. “In escrow” is a term used to describe an item that is momentarily surrendered to an escrow agent. An escrow agent serves as an asset holder between a buyer and a seller who signed an escrow agreement. In this arrangement, it is the agent’s responsibility to keep the assets safe until both parties meet the conditions written in the contract. Note that real estate, titles, money, and funds are assets that one can temporarily keep in escrow.

Escrow Agreement: The Processes Involved

Purchasing a house is not as simple as it seems. A seller may be hiding some information from the buyer concerning the property he/she is selling. On the other hand, a buyer may be promising the seller of his/her ability to pay for the property even if he/she doesn’t have enough money in his/her pocket. There can be a lot of issues arising from selling and purchasing a home. With that said, let us see and understand the processes involved in an escrow agreement.

According to Philipp Huhn, by the year 2023, the revenue of real estate appraiser offices in the U.S. will reach about 6.153,1 million dollars.

How to Draft of an Enforceable Escrow Agreement

Remember that an escrow agreement is a contract made between a buyer, seller, and a third party agent. These three should be included when drafting the correct escrow agreement. Here are the steps in creating one:

Step 1: Write the Date and the Information Required

First, write the date the agreement would effectuate. Then, specify the complete name or company name of the buyer, seller, and the escrow agent. An escrow agent could be an attorney, a title company, or a bank. One example is an agreement signed on a specific date by a company that wishes to buy stock from an individual seller, and both are mediated by a bank that acts as the escrow agent.

Step 2: Incorporate Preceding Clauses

Recitals are preceding clauses that give an overview of what the contract is all about. These clauses serve as a preparatory statement and are used to define the purposes of the agreement. A rundown of the purchase agreement and financing agreement are also included in this part of the agreement. Additionally, these clauses should also state the role of all the parties involved.

Step 3: Place the Conditions for the Parties Involved

Terms and conditions cover the body of an agreement. It commands how each party involved in the contract should behave and relate to one another. In an escrow agreement, the following matters are specified: role of the escrow agent, amount to be deposited in escrow, taxes, payment terms, indemnification clauses, fees for the agent, and other crucial sections. Each section should be as specific as possible to give the parties involved a clear understanding of the plan and purpose of the contract.

Step 4: Finish the Contract with Miscellaneous Provisions

This is the most commonly overlooked part of a contract. Miscellaneous provisions usually include the laws applied, jurisdiction involved, amendment clauses, etc. These overlooked provisions can greatly influence the rights of the contract holders. Therefore, they should be taken into account. For example, the laws applied are used to interpret, govern, and enforce the contract.

FAQs

How much is the fee for an escrow agent?

The fee for an escrow agent can be different in every state, and the same is true whether a seller or a buyer is accountable for paying the agent or not. Most of the time, the seller and buyer decide to split the escrow fee. Typically, an agent will ask for one to two percent of a property’s full price. For small business tradings, escrow agents only ask for the basic price.

Is money from an escrow account withdrawable?

The purpose of an escrow account is to secure the money one party has willingly deposited in escrow. Money in an escrow account is non-withdrawable; neither is one party permitted to take money from the account. This means that the money kept in escrow is safe, and it can only be released once the buyer or the seller has met the requirements written in the escrow agreement.

How long does an escrow agreement last?

An escrow agreement usually lasts up to 30 days, yet the length still primarily depends on the agreement made by the buyer and the seller. The duration of the agreement is influenced by what the seller or buyer needs to do to meet the conditions of the contract. During the process, a buyer may perform property inspections, which could last for a maximum of 12 days. He/she may also apply for a loan, which will take some time to complete.

How do you terminate an escrow agreement?

In normal cases, an escrow agreement can only be terminated after its completion, but there are cases when both parties consent to the termination of an agreement prematurely. If this happens, other agreements in connection to the escrow agreement should also be canceled. In a situation where both parties have not met the conditions listed in the agreement on time, the assets they have deposited to an escrow agent will be returned to them accordingly.

Is opening an escrow account compulsory?

Opening an escrow account is unavoidable, especially when a homebuyer applies for a mortgage. Aside from the loan, additional payment is deposited into an escrow account on a monthly basis. Usually, a bank receives payments for taxes and insurance every month. When a homebuyer loans money from a lender, the home automatically becomes the collateral. In this case, opening an escrow account will depend on the lender and the type of loan the buyer has applied for. If a buyer is under the Federal Housing Administration, then he/she is required to open an escrow account. The FHA is a government agency in the United States that secures loans made by private individuals or entities. Note that escrow is mandatory when the loan a buyer applies for is risky.

Michael Jordan, in one of his quotations, once expressed, “You should be true to your game, so the game will in return, be true to you. If you plan to shortcut the game, the game will do the same to you. If you give all of your efforts, great things will be given to you. That’s how you play a game, and in a way, it describes life too.” As you see, using an escrow agreement is like playing a sport, both parties are expected to play fair before an award is given.