26+ Sample General Ledger

-

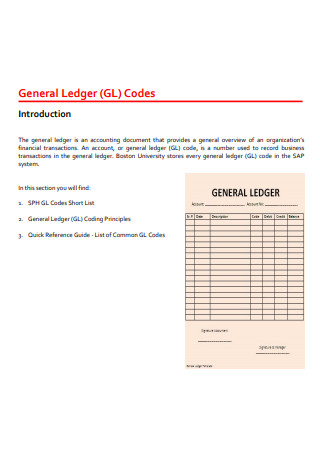

General Ledger Codes

download now -

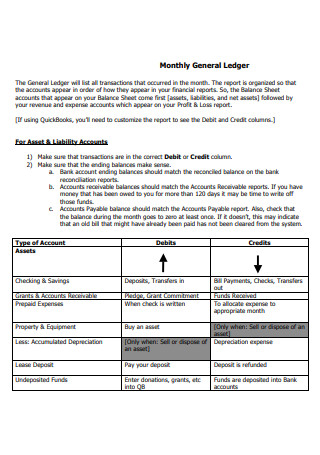

Monthly General Ledger

download now -

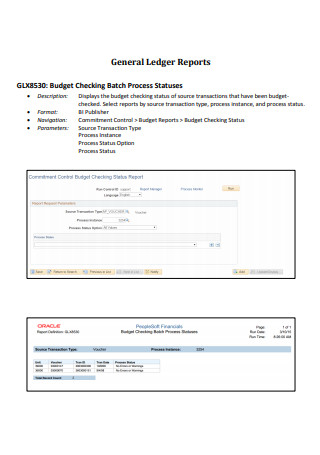

General Ledger Report

download now -

General Ledger Operations Manual

download now -

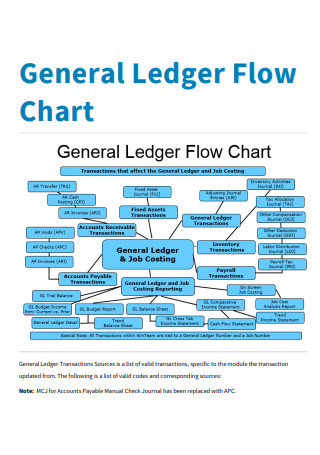

General Ledger Flow Chart

download now -

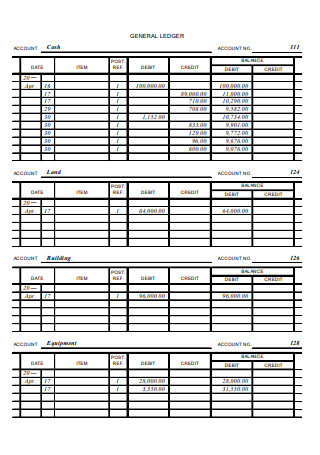

Sample General Ledger

download now -

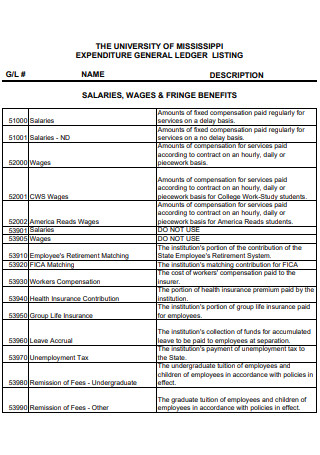

Expenditure General Ledger Listing

download now -

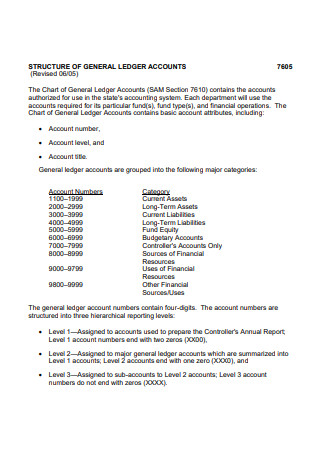

General Ledger Accounts

download now -

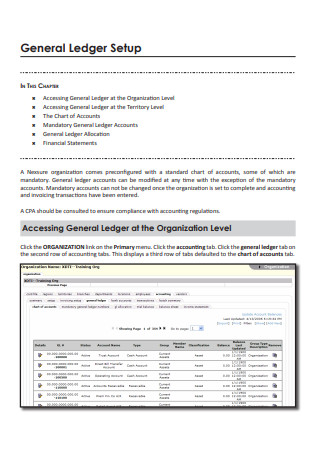

Basic General Ledger

download now -

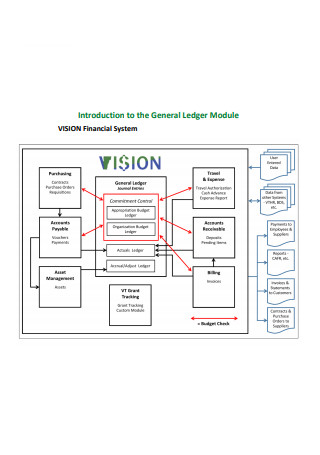

General Ledger Module

download now -

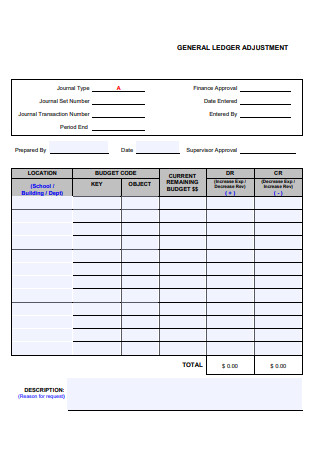

General Ledger Adjustment

download now -

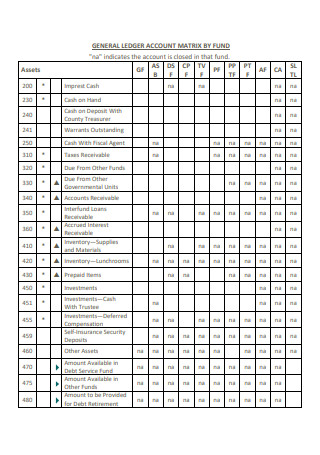

General Ledger Account Matrix by Fund

download now -

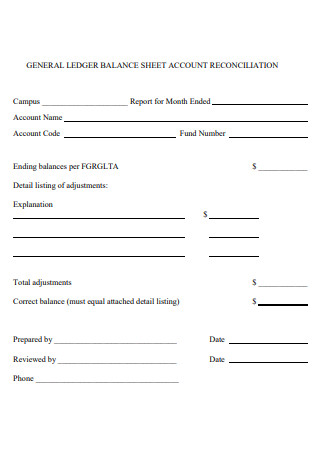

General Ledger Balance Sheet Account Reconciliation

download now -

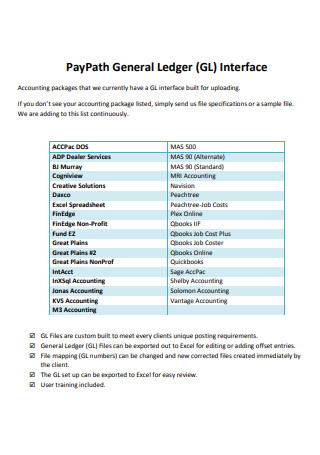

General Ledger interface

download now -

General Ledger Balance Inquiries

download now -

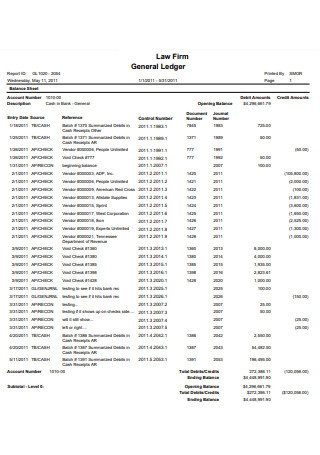

Law Firm General Ledger

download now -

General Ledger Summary Report

download now -

Printable General Ledger

download now -

General Ledger Example

download now -

General Ledger Chart of Accounts

download now -

General Ledger in PDF

download now -

Formal General Ledger

download now -

General Ledger Account Policy

download now -

Simple General Ledger

download now -

General Ledger Format

download now -

General Ledger Account Request

download now -

General Ledger Form

download now

FREE General Ledger s to Download

26+ Sample General Ledger

What Is a General Ledger?

Types of General Ledger Accounts

Elements of a General Ledger

How To Create a General Ledger

FAQs

What is the importance of a company’s general ledger?

What is a general ledger reconciliation?

What are the various types of ledgers?

Knowing the difference as you set bigger and bolder challenges for yourself is critical to your sanity, success, and satisfaction.” It is challenging to grow and develop your company, but engaging in the right processes results in a future of success and satisfaction. In terms of financial affairs, a general ledger provides the company with the information it needs. What is it, and what significance does it hold for the business? Learn more about these documents, including their description, composition, and construction. The article also contains answers to frequently asked questions regarding general ledgers.

What Is a General Ledger?

A general ledger is a master accounting document representing the company’s record-keeping system that contains the financial information of debit or credit accounts through the validation of trial balance. It provides a report regarding financial affairs and transactions that happens within the organization’s time of operation. It also contains necessary account information to prepare for the organization’s financial statements. It helps the company see the bigger picture and status of accounts. These accounts undergo sorting into various categories, including assets, liabilities, revenues, expenses, gains, and losses. Once the subcategories or sub-ledgers are closed out, the production of a trial balance follows. A company produces other vital documents, including financial statements, balance sheets, income statements, cash flow statements, and corresponding financial reports through the trial balance.

The United States Bureau of Fiscal Service provides all US businesses a standardized financial system through the United States Standard General Ledger or USSGL. Organizations possess consistent accounting charts and practices with technical regulations regarding federal agency accounting. The USSGL is easily accessible to all companies through its direct website.

Types of General Ledger Accounts

Most general ledgers follow five types of accounts, otherwise known as categories. These accounts are where organizations classify their business transactions throughout the entirety of their operations. Each category contains sub-ledgers, covering more precise information, including the remaining balance on hand, accounts receivable, and accounts payable under the organization. Below are the five account types that are present in general ledgers.

Elements of a General Ledger

Remember, general ledgers contain vital information regarding a company’s financial transactions and all connected accounts to accurately account and forecast representations of the organization’s financial status. With that, it serves as the company’s primary database for financial records and documents, with other necessary financial papers stemming from the general ledger. Below are the three main components that must be present in your company’s general ledger.

How To Create a General Ledger

As established, companies rely on general ledgers to ensure that their financial transactions are precise and accurate. Each company must have a general ledger that ensures the management of monetary matters and keeps track of all ledger accounts. Below are simple steps that your company must follow to create a general ledger.

Step 1: Identify and Create the General Ledger Accounts

Start by classifying financial transactions into the five ledger accounts. These must be relevant to the form of the general ledger you choose to use. The USSGL also provides a statutory format that you can utilize to start your ledger. Guarantee that the table you have consists of assets, liabilities, equities, revenues, and expenses accounts. Allocate a table for each account in your general ledger.

Step 2: Transfer the Necessary Accounts from the General Journal

Companies that utilize the double-entry bookkeeping method have a general journal. The general journal is the initial record of financial transactions of an organization. Entries in the general journal are also written chronologically and make it easier for the individual to transfer entries into the general ledger through an account-by-account basis. Guarantee that all necessary information in the general journal must be present in the general ledger.

Step 3: Make Sure to Number All the Entry Records

The general ledger must contain a number column where you can indicate the journal transaction ledger corresponding to the general ledger account. Enforcing this step allows the company accountant or the individual handling the transfer to cross-reference entries for an accurate and precise record.

Step 4: Indicate if Cash Payments are Debit or Credit

It is critical to state whether the account is on credit or debit. This allows the person to utilize the double-entry bookkeeping method to guarantee the company’s financial health is in balance.

Step 5: Ensure the Presence of a Running Balance in the General Ledger

Keep a running balance on your general ledger to balance the credits and debits present in the ledger accounts. It determines whether the account maintains stability after all journal entry transactions are entered into the ledger. Afterward, the general ledger becomes the master accounting document and record-keeping system. Finish off the general ledger by double-checking the presence of the transaction names, debit and credit status, dollar amount, and the running balance.

FAQs

What is the importance of a company’s general ledger?

The general ledger serves multiple purposes to the company. Generally, it holds all of the financial statements you need to compose other finance documents. It also serves as a source or proof document for company invoices and receipts. Aside from this, the general ledger aids the company in its loan applications, as it provides a complete and detailed document of financial records. It also helps with balancing company checkbooks through a trial balance. The company can also prepare for auditing processes for the Internal Revenue System or IRS. The general ledger also lessens fraudulent situations and enables internal and external communication between the company, management, and customers.

What is a general ledger reconciliation?

A general ledger reconciliation is a method of comparing different data accounts. Individuals who a responsible for reconciliation must verify books and records against various financial documents, including statements, reports, and accounts. Companies also utilize sub-ledgers under the accounts payable and receivable categories. This allows the two documents to match up properly with the general ledger.

What are the various types of ledgers?

Ledgers are known to be principal accounting books and permanent records composed of all known business transactions. There are three types of ledgers that are recognizable in the business industry, including sales, purchase, and general ledgers. A sales ledger, otherwise known as a debtor’s ledger, is a collection of accounts regarding the sale of goods or services to customers. A purchase ledger groups different accounts focusing on sellers and the incurred purchases coming from credit. Lastly, a general ledger includes a nominal and private ledger, meaning it includes accounts with numerical values and confidential records.

In handling company operations, it pays to have a clear and comprehensive record of transactions, monetary or non-monetary in value. A general ledger is a valuable system to have in a company. It provides easier access to account records, financial statements, and filing taxes. For starting companies, it is best to start with a general journal to aid in creating the general ledger. If you don’t know where to begin in creating this system, general ledgers samples are available to use and download above for your convenience. Start making your organization’s general ledger to secure and record all your business’ financial transactions.