17+ Sample Variance Analysis

-

Standard Costing and Variance Analysis

download now -

Four-Variance Analysis

download now -

Budgetary Control and Variance Analysis

download now -

Variance Analysis in Airlines

download now -

Actual Variance Analysis Template

download now -

Sample Understanding Variance Analysis

download now -

Cost Accounting Variance Analysis

download now -

Beyond Variance Analysis Template

download now -

Sample Overhead Variance Analysis

download now -

Variance Analysis in Construction

download now -

Basic Variance Analysis Template

download now -

Mean-Variance Analysis Template

download now -

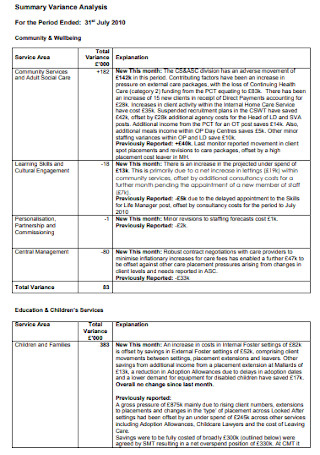

Sample Summary Variance Analysis

download now -

Variance Analyses from Invariance Analyses

download now -

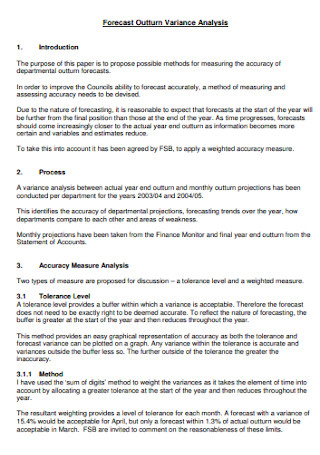

Forecast Outturn Variance Analysis

download now -

Strategic Variance Analysis

download now -

Variance Analysis for Policy Template

download now -

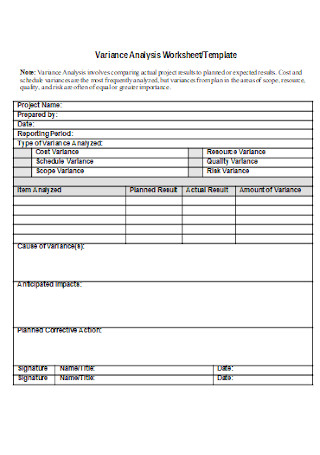

Variance Analysis Worksheet Template

download now

Variance Analysis: What Is It?

Differentiating between the planned and actual behavior is how variance analysis is summed up. So in the concept of accounting or project management, variance analysis is a quantitative investigation that helps you gain control of a business. A simple concept is when your budget sales plan is $10,000. Yet, actual sales reached $6,000. Hence, variance analysis yielded $4,000 as its difference. And such analysis has played a major role in defining budgets and financial performances of many organizations worldwide.

Based on a survey, the US accounting industry was expected to total revenue of $110 billion in 2020.

What Are the Types of Variance?

To understand how variance analysis works, you have to get introduced to its different types first. The analysis is not conducted in one approach because differences apply to every formula and consideration as well. And the important variance types are the following:

How to Conduct Variance Analysis

Variance evaluation is part of the many responsibilities in management. So, it would be best to consider variance analysis to fully report and control your organization effectively. But, don’t be intimidated by the process because analyzing is attainable when you know the steps. And the basic steps in conducting variance analysis are:

Step 1: Recognize Your Areas of Concern and Purpose

Conduct a thorough review about what your organization’s areas of concern are. A lot could be identified may that be an issue from the balance sheet, income statement, raw materials, and so much more. Eventually, you will understand your main purpose for analyzing. You are not just considering analyzing for fun but for the sake of evaluating and forecasting your organization’s planned and actual behavior anyway. Your purpose helps you know how to tailor the analysis later on.

Step 2: Figure Out the Appropriate Type of Variance Formula

Now that you know your purpose and areas of concern, identify what type of variance you are looking for. Recognizing the variance type helps you know what appropriate formula must be used for your analysis. So if you are concerned about specific rates, use price variance. For efficiency, you have quantity variance. And you can use the types of variance discussed earlier as your reference here.

Step 3: Observe an Easy-to-Follow Presentation

In presenting the formulas and calculations, and even the whole analysis report itself, be sure your presentation is easy to follow. You can present every detail without confusing audiences by using a chart instead of writing the report like a lengthy essay. Also, input the appropriate labels. Your calculations might confuse audiences without acknowledging what each variable means. Another practice is to include instructions so people won’t have a hard time reading the document.

Step 4: Interpret Results Clearly

One of the important parts of variance analysis is to write your interpretation of the results. This part marks your analysis’s closing statement by ensuring everything is explained from start to finish. So how did you derive those results? Is the outcome good or bad? How is the result going to reflect your business? Answer those questions. And the interpreted results will eventually be used to formulate an action plan of whether to maintain the positive results or change the negative outcomes into something better for the organization.

FAQs

What are some challenges with variance analysis?

Variance analysis is challenging because of standard setting. You will be comparing standard variables to actual results. But, the different results may sometimes not yield important information. Also, it takes time in conducting the analysis. For example, accountants may have to gather all variances per month before actually displaying the outcomes to the management. And probably the most challenging is to gather the right information. You might have the wrong source of info from the material bills, labor routes, and other records that may bring adversities.

What are other examples of variance analysis?

Besides the four main types of variance analysis mentioned earlier, you may also have to deal with the following specific examples:

- Purchase price variance

- Selling price variance

- Labor rate variance

- Labor efficiency variance

- Fixed overhead spending variance

- Variable overhead spending variance

- Variable overhead efficiency variance

- Material yield variance

What is the concept of variance?

Variance is a concept known for statistical measurements, particularly between numbers in a set of data. Also, variance helps you recognize how different every number in a set is, including what they mean and how it affects every number in a set. And ?2 is the symbol used for a variance.

Variance analysis is, no doubt, an integral part of any business’s information system for responsible accounting and management. Consider variance analysis reports as standards to benefit the materials’ cost and quantity, labor, and even overhead of producing specific products and services. Without analysis, you would fail to measure and forecast your organization’s financial performance. Stay in direct control of every designated responsibility’s performance now using sample variance analysis.