50+ SAMPLE Accounting Checklist

-

Accounting Checklist

download now -

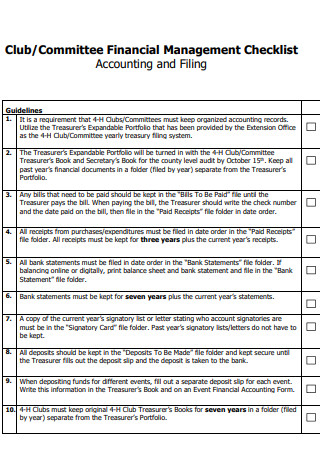

Accounting and Filing Checklist

download now -

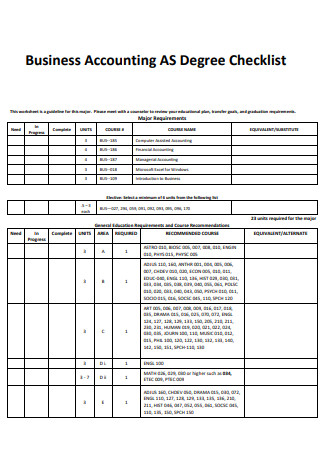

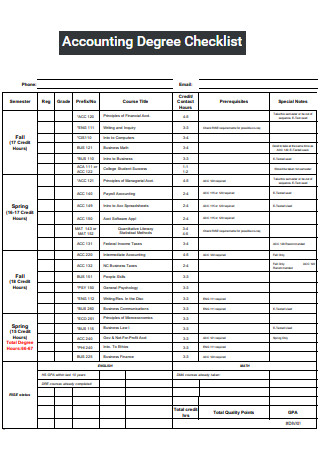

Business Accounting Degree Checklist

download now -

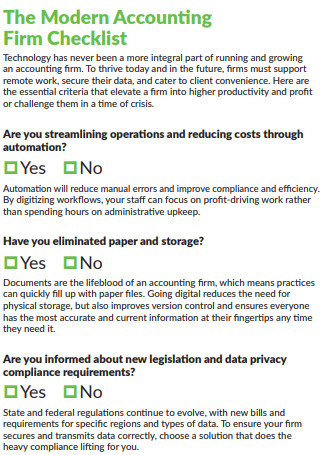

Modern Accounting Firm Checklist

download now -

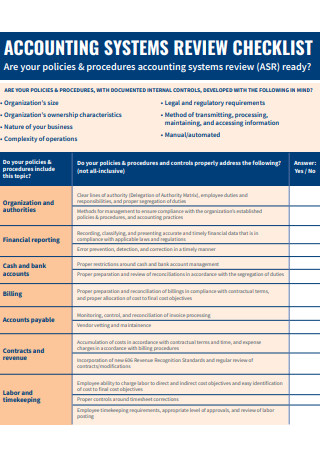

Accounting Systems Review Checklist

download now -

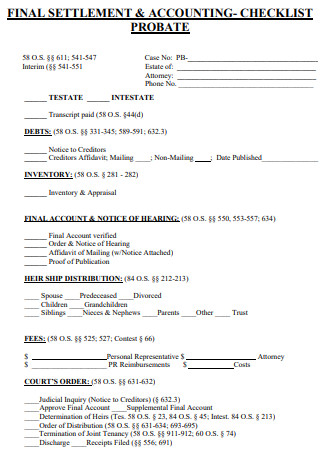

Final Settlement Accounting Checklist

download now -

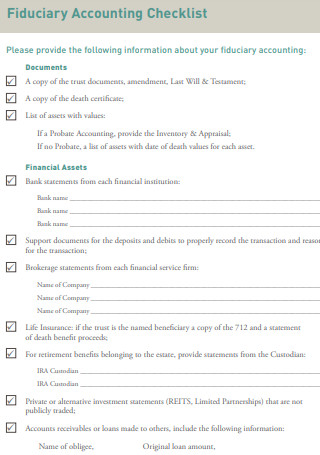

Fiduciary Accounting Checklist

download now -

Accounting Degree Checklist

download now -

Accounting Year End Department Checklist

download now -

Guardianship Annual Accounting Checklist

download now -

Sample Accounting YChecklist

download now -

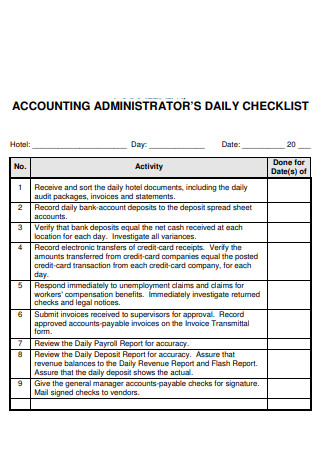

Accounting Administrators Daily Checklist

download now -

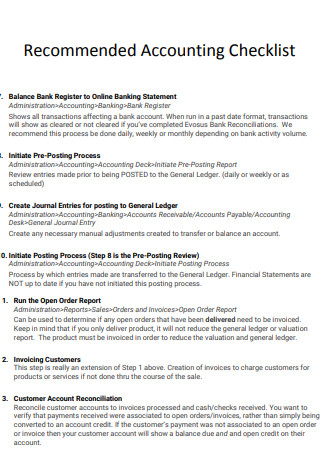

Recommended Accounting Checklist

download now -

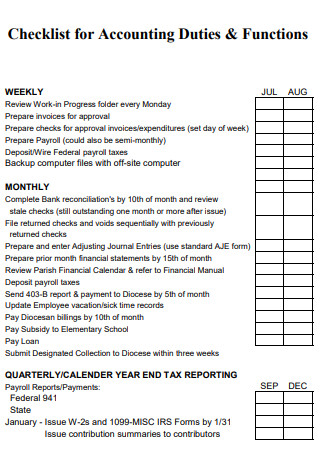

Accounting Duties & Functions Checklist

download now -

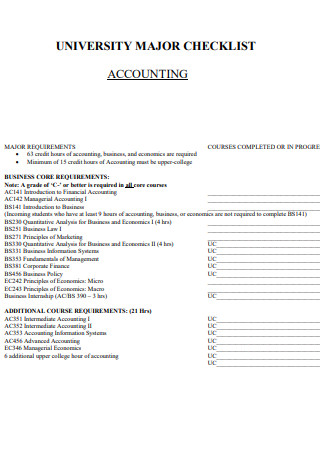

University Major Accounting Checklist

download now -

Simple Accounting Checklist

download now -

Basic Accounting Checklist

download now -

Accounting Systems Annual Checkup Checklist

download now -

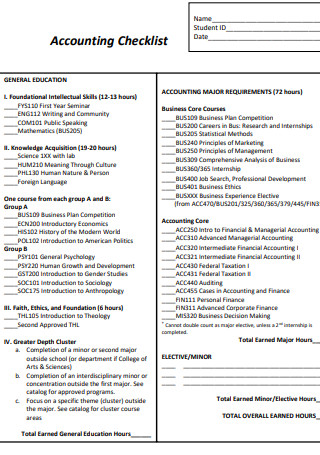

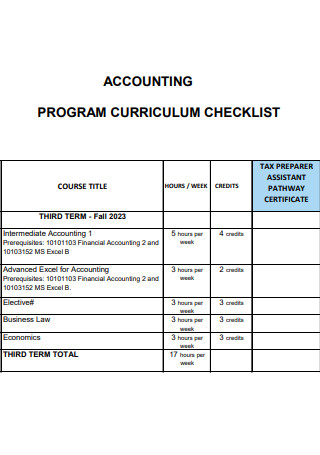

Accounting Program Curriculum Checklist

download now -

Accounting Tax Return Preparation Checklist

download now -

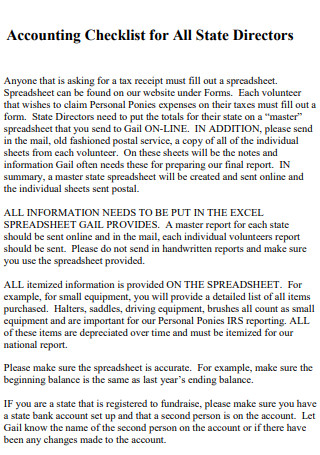

Accounting Checklist for All State Directors

download now -

Accounting Checklist Example

download now -

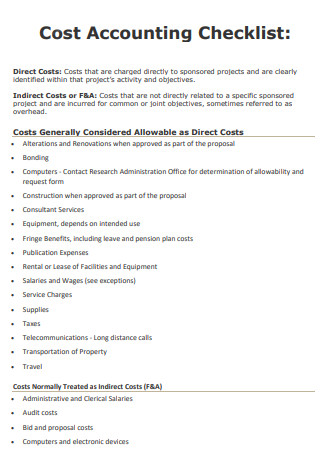

Cost Accounting Checklist

download now -

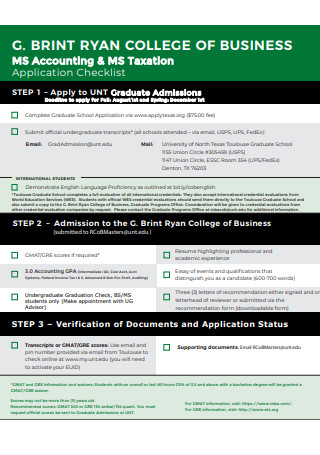

Accounting Application Checklist

download now -

Conservatorship Annual and Final Accounting Checklist

download now -

Student Accounting Fall Checklist

download now -

Accounting for Climate-Related Checklist

download now -

Accounting System Checklist

download now -

Accounting Legal Service Provider Checklist

download now -

Accounting Court Checklist

download now -

Nonprofit Accounting Year-End Checklist

download now -

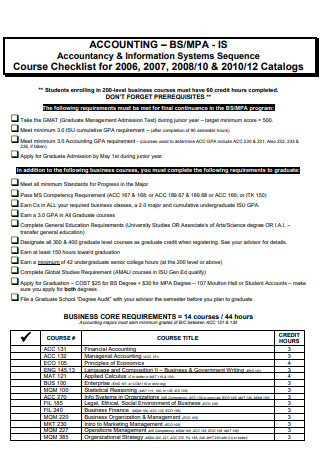

Accounting Curriculum Sequence Checklist

download now -

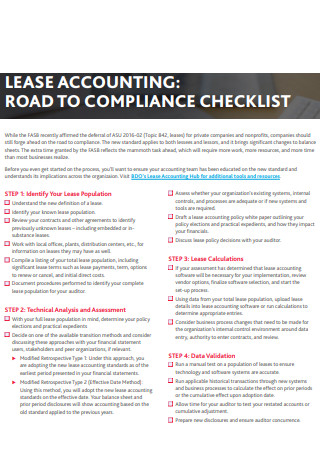

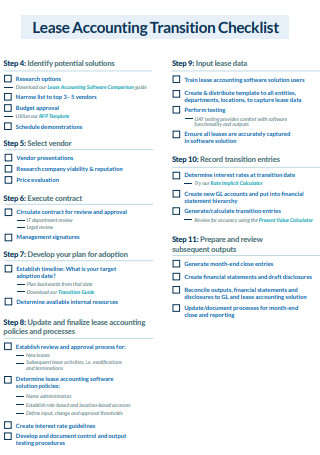

Lease Accounting Checklist

download now -

Nonprofit Outsourced Accounting Checklist

download now -

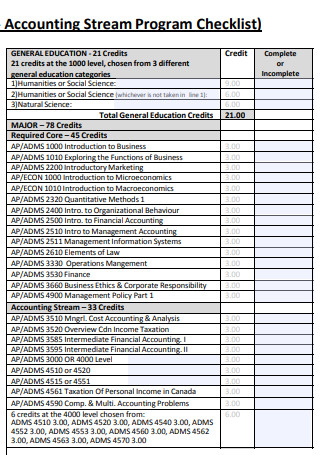

Accounting Stream Program Checklist

download now -

Rental Property Tax Accounting Checklist

download now -

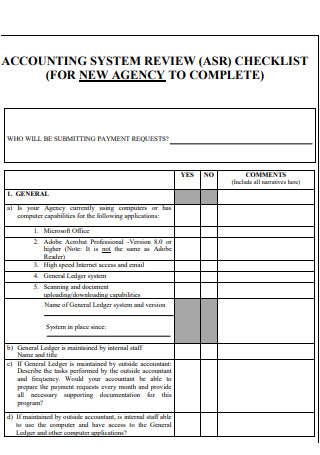

Accounting System Review Checklist

download now -

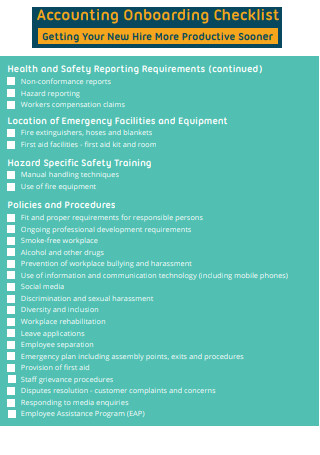

Accounting Onboarding Checklist

download now -

Accounting App Evaluation Checklist

download now -

Year-End Accounting Checklist

download now -

Non-Accounting Checklist

download now -

Lease Accounting Transition Checklist

download now -

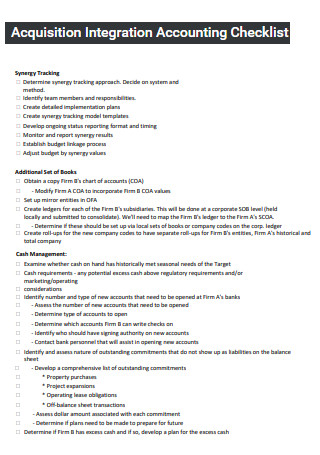

Acquisition Integration Accounting Checklist

download now -

Accounting Course Checklist

download now -

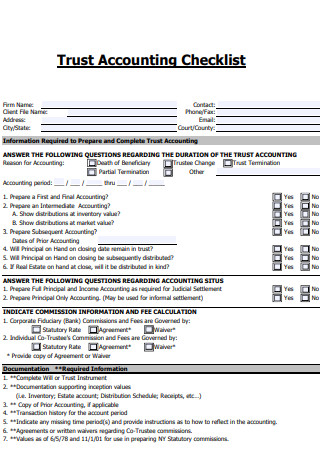

Trust Accounting Checklist

download now -

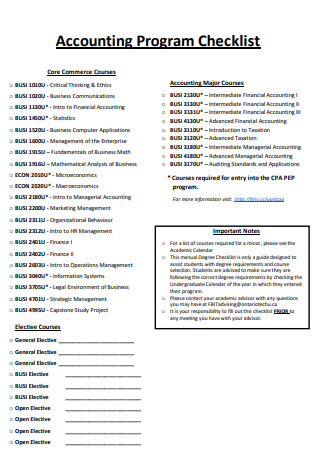

Accounting Program Checklist

download now -

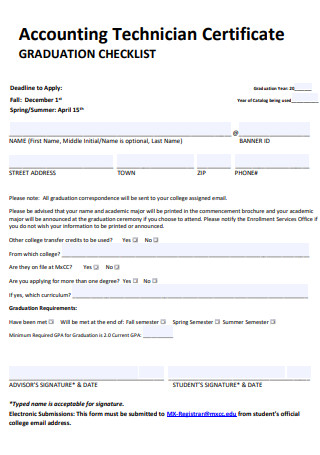

Accounting Technician Certificate Graduation Checklist

download now -

Accounting Month End Checklist

download now -

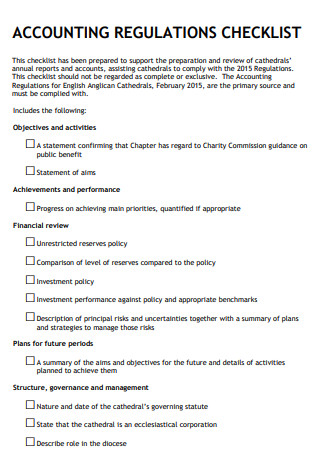

Accounting Regulations Checklist

download now -

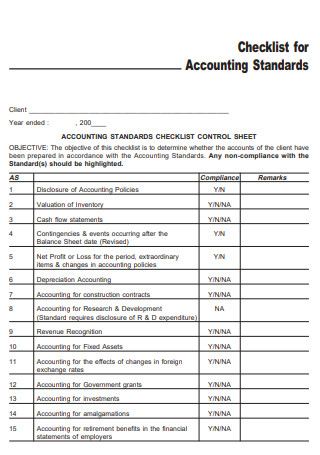

Accounting Standard Checklist

download now -

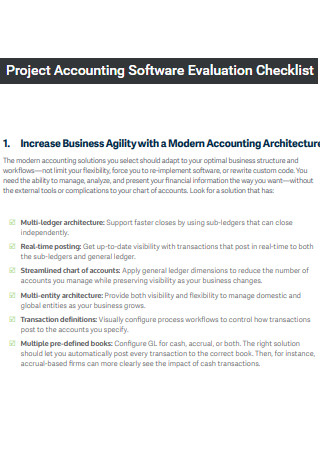

Project Accounting Software Evaluation Checklist

download now

FREE Accounting Checklist s to Download

50+ SAMPLE Accounting Checklist

What Is an Accounting Checklist?

What Is the Purpose of Accounting?

What Are the Types of Accounting?

What Is Included in the Accounting Checklist?

Steps on How to Maintain the Routine of an Accounting Checklist:

FAQs

What Is the Golden Rule of Accounting?

What Is Accounting Cycle?

What Is Balance Sheet Format?

What Is an Accounting Checklist?

Accounting Checklist can be an online or written document of list where you create a realistic plan with a budget, record your transactions correctly, review your results regularly and always keep good records. Your comfort level with the three basic financial reports that evaluate your fiscal health is also essential: the balance sheet, income statement and cash flow statement.

In addition, the Accounting Checklist can help track and analyze important data regarding expenditure, investments, and determine an ideal manner for reporting revenue growth. Unfortunately, even though most big companies have a dedicated accounting team to take care of these processes, it is the small businesses which find accounting and finance a challenge.

What Is the Purpose of Accounting?

The purpose of accounting is to accumulate and report on financial information about the performance, financial position, and cash flows of a business. This information is then used to reach decisions about how to manage the business, or invest in it, or lend money to it. This information is accumulated in accounting records with accounting transactions, which are recorded either through such standardized business transactions as customer invoicing or supplier invoices, or through more specialized transactions, known as journal entries.

What Are the Types of Accounting?

Many professional accounting sources may divide accounting usually g careers into different categories. Hence, the four types listed here reflect the accounting roles available throughout the profession. These four branches include corporate, public, government, and forensic accounting.

What Is Included in the Accounting Checklist?

Here is a few information gathered to compose the Accounting Checklist:

Collect and Analyze Financial Statements

Your financial statements are a lifeline for your small business. They give you a glimpse of where your business stands financially. And, statements let you see past and current finances so you can forecast your business’s financial future and plan for the new year. Financial statements help you understand your business’s financial standing and make tax season less of a burden on your company. You can access your financial records in your accounting books. Use an accounting records book to compile and analyze year-end statements. There are a few financial statements that you should have handy, including:

- Income statement

- Cash flow statement

- Income statement

- Balance sheet

Your income statement, or profit and loss statement, summarizes your revenue and expenses. Your income statement lists all of the money you gained and lost throughout the year. You can find your business bottom line by looking at the difference between money gained and lost on your statement. Compare this year’s income statement to last year to analyze the differences in revenue and expenses from year to year.

Cash Flow Statement

Cash flow statements only record the actual cash you have, not credit. Your cash flow statement lists your business’s incoming and outgoing cash. Cash flow can be positive, meaning that your business has more incoming money than expenses. Negative cash flow occurs when you spend more money than what you are bringing in. Moreover, the cash flow statement can show you the timing in which money comes in or goes out of your business. For example, you can see which months have a higher cash flow and the months where your business’s cash flow is struggling. Tracking your cash flow throughout the year and at year-end can also help you create a cash flow forecast and predict your future cash flow.

Balance Sheet

Your business balance sheet shows your assets, liabilities, and equity and tracks your company’s financial progress. Here are the different aspects of the balance sheet:

- Assets: What you own

- Liabilities: What you owe

- Equity: Money left over after you pay expenses

- Liabilities and equity should always be the same amount as your assets.

Collect Past Due Invoices

Try to collect the money that customers owe your business if you want to wrap up your books for year-end. This means putting in a little legwork and trying to collect past due invoices before the new year. Some customers may just need a gentle nudge with a simple invoice reminder. Others may need some additional nudging. So, what do you do if a customer won’t pay?

- Contact customers with past due invoices

- Set up invoice payment terms (the due dates)

- Document the payment process

- Establish a payment plan with customers

When reaching out to customers about past due invoices, be professional. Be understanding, patient, and positive when you talk to late-paying customers. If collecting payments from customers is difficult, consider offering them a payment plan. The customer might not be able to pay their invoice off all at once. Negotiating an installment plan can help you get paid faster. Plus, it shows customers that you understand their situation and care about their needs.

Account for Inventory

You must get an accurate count of the materials and supplies you have on hand if your business has inventory. Otherwise, you could wind up with empty shelves or inventory shrinkage. If your business has inventory, complete an inventory check before year-end. Match your inventory totals to your balance sheet. If you find discrepancies between your count and balance sheet, make adjustments.

In addition, accounting for inventory at year-end can also help you know how much you spent on inventory during the year and its value. And, it can help you better plan next year’s inventory, especially for busier seasons.

Organize Business Receipts

Disorganized receipts can put your small business at risk of sloppy and inaccurate books. Not to mention, messy records can increase your chances of making errors on your business tax return and cause more issues in the future.

Reconcile Bank Accounts and Credit Cards

A major aspect of your accounting year-end procedures checklist is reconciling your bank accounts and credit cards. That way, you verify that your accounting records match your bank accounts. To reconcile your accounts, compare your bank and credit card statements to your accounting records. Your statements should match the balance listed in your books. If they don’t match, do a little digging to find the discrepancy. You may need to adjust one of your records for the balances to be equal.

Review Accounts Payable and Receivable

Prior to year-end, review both your accounts receivable and accounts payable to ensure you settle all collections and debts. In accounts receivable, check for past due invoices. If a customer has any late or unpaid invoices, contact them as soon as possible via email, phone call, or any messaging app. Look at your accounts receivable aging report to see if you have any late or unpaid bills before year-end. Follow up with vendors and pay off bills to start off the new year with a clean slate.

Back Up Information

To make sure you securely save your accounting data for the new year, add backing up information to your year-end closing checklist. The last thing you want to do is lose important accounting information from this year and previous years. To ensure your data is safe, have a reliable backup system in place.

Thus, you could back up accounting information on your computer or smartphone or print off documents and store them in a secure spot. If you use online accounting, you can rest easy knowing that your information is secure in the cloud. Whatever you decide to do, make sure you have a plan in place to back up those precious accounting records for your business.

Get Necessary Documents Ready for Your Accountant

If you use an accountant in some shape or form for your business such as accounting software in conjunction with a tax professional, you need to get documents ready to go for your accountant before year-end. Although it depends on what your accountant is handling for you, here is some information you may need to gather:

- Petty cash records

- Invoices and receipts

- Financial statements

- Bank and credit card statements

- Sales records

- Payroll records

- Loan information

Steps on How to Maintain the Routine of an Accounting Checklist:

Creating a daily routine for accounting tasks goes a long way in improving the accuracy and effectiveness of your company’s books. Here are some recommended tasks you should complete each day:

Step 1: Refresh and Update Your Financial Data

Your accounting software automatically syncs your bank and credit card feeds, and the sales data from the POS system, into your accounting software. If it does not, you will need to do this manually. This gives you an up-to-date look at your accounts, showing you the money moving in and out of your business.

Step 2: Reconcile Cash and Receipts

Reconciling cash and receipts at the end of each day helps you discover cash shortages or overages quickly, so you can figure out where the money went and identify errors or theft. This is also essential in establishing controls and accountability in your organization, which breaks down when not tended to every day.

Step 3: Review and Reconcile Transactions

If your accounting software is connected to your bank and synced daily, there is no need to wait for your monthly bank statement. Many accounting applications simplify reconciliation by suggesting matches, so all you have to do is review and approve them. Spending a little time on this task each day is easy and eliminates a grueling month-end chore. It is also a good time to review pending transactions for any errors or abnormalities, so you can investigate potential issues promptly.

Step 4: Record and Categorize Expenses

Many accounting software programs have apps that you can use to report expenses and upload receipts, so it is easy to take care of them immediately. Rather than sort through a stack of receipts at the end of the month, just snap a picture of the receipt and jot a note about the details.

Step 5: Record Inventory Received

Entering inventory into your system the same day you receive it keeps your system current, giving you a more accurate look at your stock. If you do not do this, your staff may lose sales by telling customers you are out of stock when an item just hasn’t been entered into the system. Also, if your staff sells out of an item, reordering may be delayed if your system is not set up to allow negative inventory counts.

FAQs

What Is the Golden Rule of Accounting?

Debit the receiver and credit the giver. Debit what comes in and credit what goes out. Debit expenses and losses, credit income and gains.

What Is Accounting Cycle?

The accounting cycle is a collective process of analyzing, identifying, and recording the accounting events of a company. It is a standard 8-step process that begins when a transaction occurs and ends with its inclusion in the financial statements.

What Is Balance Sheet Format?

The balance sheet is a report version of the accounting equation that is balance sheet equation where the total of assets always is equal to the total of liabilities plus shareholder’s capital. Assets = Liability + Capital.

Reconciliation of all your cash business transaction entries need to be accurate so that you always know how much cash liquidity you have available on a monthly basis. This will make it easier to correct errors or find omissions which can then be looked into and corrected.

A healthy cash flow is greatly vital and should be right at the top of the accounting checklist for all types of businesses, especially the small ones. This is because knowing how much cash you will be generating over the coming months will help you set deadlines for the payment of various bills, both to the people you employ as well as to your vendors. This would also help you in the long run by allowing you to make more informed decisions.