Explanation Letter Samples

-

Explanation Letter to Employee

download now -

Explanation Letter for Mistake

download now -

Explanation Letter for Absent

download now -

Explanation Letter for Work

download now -

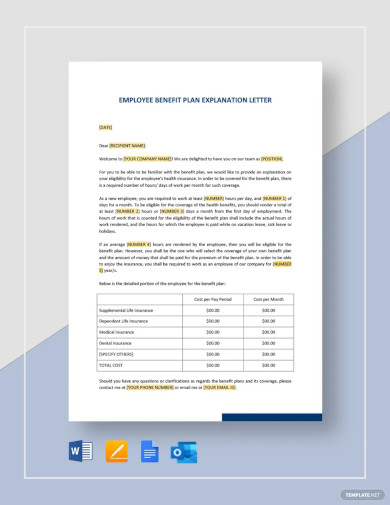

Free Employee Benefit Plan Explanation Letter Template

download now -

Employee Benefit Plan Explanation Letter Template

download now -

Sample Letter of Explanation

download now -

Employee Explanation Letter

download now -

Loan Letter of Explanation

download now -

Government Explanation Letter

download now -

Sample Academic Progress Explanation Letter

download now -

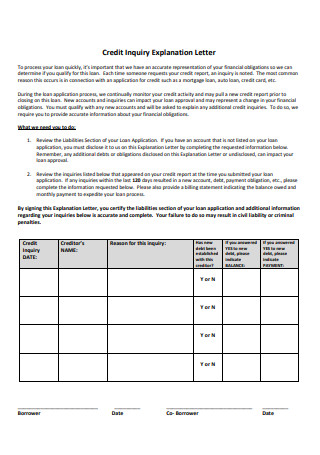

Letter of Explanation for Credit Inquiries

download now -

Mortgage Explanation Letter

download now -

Sample Mistake Letter of Explanation

download now -

Transition Explanation Letter

download now -

Reply Explanation Letter Form

download now -

Fee Explanation Letter

download now -

Work Explanation Letter

download now -

Sample Bank Explanation Letter

download now -

Open Work Permit Letter of Explanation

download now -

Misconduct Explanation Letter

download now -

Lost Receipt Explanation Letter

download now -

Sample Official Explanation Letter

download now -

Business Explanation Letter

download now -

Explanation of Nursing Award Letter

download now -

Explanation of Declaration Letter

download now -

Absent Explanation Letter

download now -

Personal Explanation Letter

download now -

Sample College Explanation Letter

download now

FREE Explanation Letter s to Download

Explanation Letter Format

Explanation Letter Samples

What is an Explanation Letter?

Instances a Bank Underwriter Will Ask For An Explanation Letter

How To Write a Satisfactory Explanation Letter

Is my creditor allowed to reject my explanation letter?

What happens if my potential lender rejects my explanation letter?

Why do lenders and bank underwriters ask for an explanation letter?

What documents should I attach in my explanation letter addressed to a mortgage lender?

How do I avoid having to write an explanation letter?

How Do You Write a Letter of Explanation?

How Do You Write an Explanation Letter for a Mistake?

How Do You Write an Informal Letter Explanation?

What Should a Good Explanation Include?

What Are the Steps of Writing a Letter? Explain with Examples

How Do You Fill Out a Letter of Explanation?

How Do You Start a Good Explanation Letter?

How Long Should a Letter of Explanation Be?

How Do I End an Explanation Letter?

How Do You Conclude an Explanation Letter?

Is a Letter of Explanation Necessary?

How Do You Write an Explanation Letter for Work?

Download Explanation Letter Bundle

Explanation Letter Format

[Your Full Name]

[Your Address]

[City, State, Zip Code]

[Email Address]

[Phone Number]

[Date]

Subject: Explanation Regarding [Specify the Issue]

Dear [Recipient’s Name],

I am writing to provide an explanation concerning [Specify the Issue]. This letter aims to address any inquiries and present a clear understanding of the matter.

Context and Explanation:

- Background: [Provide Background Information]

- Issue: [Describe the Issue]

- Resolution Efforts: [Describe What Has Been Done to Resolve or Address the Issue]

I trust this explanation resolves any queries or concerns regarding the matter. Thank you for your understanding and attention to this issue.

Sincerely,

[Your Signature (if sending via mail)]

[Your Printed Name]

What is an Explanation Letter?

You have probably sent an explanation letter at least once in your life. As students, our teachers or professors would ask us to explain our lack of attendance in class or in school activities. We had to furnish them with a letter containing our reason for not being able to attend on that particular day. If we were sick, we had to attach a medical certificate with the letter. Now as working citizens and a regular employee of a company, whenever we had accumulated x numbers of successive lates in a week we are sent a letter notice to explain by the head HR that we need to come up with a reply within the day. All mentioned are common instances where explanation letters are used. However, explanation letters are not confined to merely these instances, it is also predominantly furnished to banks and bank underwriters.

If you are trying to get a loan for a house, banks will require you to fill out tons of paperwork. Ideally, the paperwork contains all the information the lender-bank needs to know to approve the application. However, in some cases that is not true. If the bank finds some discrepancies in the form you have filled out and their investigation, they might ask for an explanation letter. It might sound daunting, but it is not a big deal. Often, they ask simple questions to help clear out facts that they are unsure of. The primary purpose of explanation letters is to help the bank assess whether you have the ability or financial capability to pay the loan back. Once they are satisfied with your documents and application form, chances are they will approve your loan application form or mortgage application.

Instances a Bank Underwriter Will Ask For An Explanation Letter

The main reason why a mortgage lender or loan officer would ask you for an explanation letter is for him to thoroughly understand your financial standing. If he sees anything out of the ordinary in your credit history that would cause suspicion or those that can be considered as red flags, he may request an explanation coming from you to explain your side. Some common instances a mortgage lender or loan officer will ask for an explanation letter are as follows: a history in bankruptcy for a failed business undertaking, foreclosure of a previous mortgage, delinquency in paying credit, job change, erratic income, change in name, having multiple social security numbers, loan delinquency, pending civil or criminal case in court, constant change in address, downsizing to a condo or apartment, job gaps or history of non-employment, large deposits or withdrawals in one of your bank accounts, existing loans or credit, and other miscellaneous circumstances of unexplained financial irregularity.

You can explain these occurrences to the loan officer through the explanation letter. If he finds your reply satisfactory, then there’s a higher chance of your loan or mortgage application getting approved. Hence, be mindful of how you write the letter and its content. It could either make or break your loan or mortgage application. You may also see Contract Letter

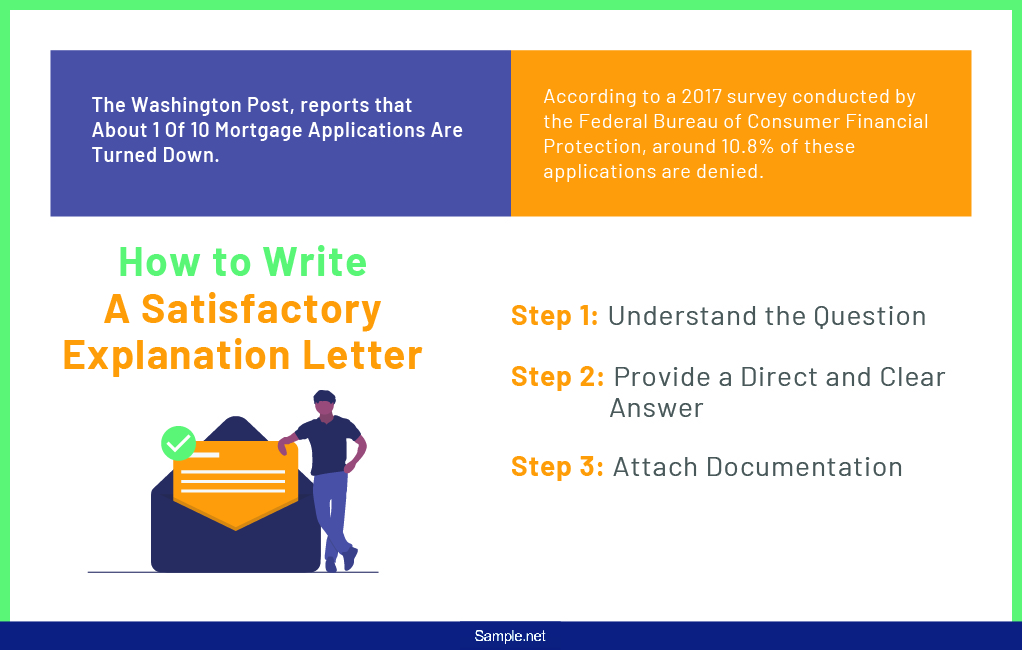

How To Write a Satisfactory Explanation Letter

Millions of Americans dream of buying their own homes. When they apply for a mortgage application, their major concern is “will the bank say yes or turn us down?” Shockingly, a huge number of loan applications don’t make it. According to a 2017 survey conducted by the Federal Bureau of Consumer Financial Protection, around 10.8% of these applications are denied. To avoid this, an applicant should take caution in the application process. Especially when asked to provide an explanation letter. To help you, below are some tips you can follow when writing an explanation letter to your lender or bank underwriter.

Step 1: Understand the question

Bank underwriters usually request letters of explanation to clarify the reasons behind a person’s financial history that could potentially affect his ability to pay the loan. Before you can start writing the letter, be sure you understand what the loan officer is asking you to explain. It is best to ask questions and specific instructions from the requesting party to be able to come up with a responsive reply. You may also see Warning Letter

Step 2: Provide a direct and clear answer

Explanation Letters to a mortgage underwriter are not letters per se. A common misconception when writing letters of explanation is that it is long. But, you only need to provide just one or two liner sentences. The reader will greatly appreciate a direct, concise, and clear reply. So keep it short and direct to the point. You do not need to explain profusely, just enough to clearly answer the lender’s inquiry. You may also see Referral Letter

Step 3: Attach documentation

Most loan officers will ask you to secure supporting documents with the letter. Even if you are not asked for such documents, consider including it since it would greatly benefit you. When you do have to include these to your letter, make sure you provide certified copies or originals. If you send the original, keep a copy for yourself for future reference. You may also see Confirmation Letter

Is my creditor allowed to reject my explanation letter?

It is common for creditors to ask you for an explanation letter explaining a bad debt history, change in job, change in residence, or about any else that could potentially affect your financial credibility in paying an ongoing credit line with them. Basically, anything that affects your ability to pay, your creditor has a right to look into it and investigate. Initially, he will ask for an explanation letter from you and hear your side of the story before he can start his own investigation. However, if your explanation letter is unsatisfactory and seems not believable, your creditor has the right to reject it and may cause the termination of your lender-borrower relationship. One of the major causes why creditors reject an explanation letter is the lack of documentation that backs up the claims made in the letter. When writing one, be sure to attach the proper evidence that can back your explanation. You may also see Acceptance Letter

What happens if my potential lender rejects my explanation letter?

If a potential lender rejects your explanation letter, it may also mean he is rejecting your loan application. If this does happen, the first thing you should do is find out why the lender disapproves so. It may be because the letter was written unsatisfactorily. You can ask a potential lender how to refine it up to his standards. Most often, a lender (especially for underwriters working for banks) will work with you and help you in your loan application process to make the approval easier and faster. Common advice they give to loan applicants when writing their explanation letters is to attach supporting documents to the letter. However, if it gets rejected again, you might want to try with another lender and work with improving your credit.

Why do lenders and bank underwriters ask for an explanation letter?

Mostly, lenders and mortgage underwriters ask an applicant for an explanation letter to protect themselves as creditors. Before they can grant your loan application, they need to make sure that you have the means to pay them back for what you owe them. Asking the letter is a way for them to cover their bases, to make sure that they have exhausted efforts in doing a background check on you, especially your credit history. With this in mind, make sure when you are asked for an explanation letter, you should send one quickly and provide accurate information so your credit application will get approved. If you choose to not provide the letter, or send it late, you could forfeit your application or your loan could get denied. You may also see Vacation Request Letter

What documents should I attach in my explanation letter addressed to a mortgage lender?

In the event, a mortgage underwriter assigned to you will ask you to provide an explanation letter, it is best to attach supporting documents. Basically, any document or records that can corroborate the claims made in the letter. However, if you are unsure what to include as an attachment, ask for clarification or advice from the underwriter tasked to manage your loan application. He might you specific instructions. The documents that should be attached in an explanation letter vary from a case to case basis. For example, a potential lender found out an erratic change in your income flow. You explain the change is due to you embarking on a business venture. You can attach in the letter a copy of your business plan permit to back up your claim that you have just opened your new business.

How do I avoid having to write an explanation letter?

One of the things you can do to avoid having to write an explanation letter is to fill out the loan application form as completely as possible. Make sure all entries you write do not raise suspicion on your ability to pay the loan back. Be cautious in answering questions that could cause a potential lender to review your financial background. For example, you have a history of bankruptcy for a failed business undertaking. Be upfront about this fact, and explain outright and thoroughly the circumstances leading to the bankruptcy. If you are having difficulties filling out the loan application form, ask for assistance. A clean, complete, and convincing loan application form will have a higher likelihood of getting your loan approved. You may also see Petition Letter

How Do You Write a Letter of Explanation?

Writing a letter of explanation involves clear communication of the facts to address concerns or questions raised by the recipient.

- Identify the Issue: Start by clearly stating the issue you are explaining.

- State the Facts: Outline the relevant facts that relate to the issue at hand.

- Provide Context: Explain the circumstances that led to the situation.

- Outline Steps Taken: Detail any corrective measures or important actions taken.

- Formal Closing: Use a formal letter format to conclude, ensuring professionalism. You may also see Letter of Support

How Do You Write an Explanation Letter for a Mistake?

Addressing a mistake through an explanation letter requires tact and clarity to effectively communicate your response.

- Acknowledge the Mistake: Begin by openly acknowledging the mistake.

- Apologize Sincerely: Express genuine remorse for any inconvenience caused.

- Explain the Reasons: Provide a clear explanation of how the mistake occurred. You may also see Letter of Employment

- Detail Corrective Actions: Describe the steps you have taken to correct the error.

- Reassure Future Commitment: Reaffirm your commitment to preventing future errors, using a tone suitable for an excuse letter.

How Do I Address an Explanation Letter?

Properly addressing an explanation letter helps ensure that it reaches the intended recipient and is taken seriously.

- Recipient Information: Start with the recipient’s full name and title.

- Company/Organization: Include the company or organization’s name if applicable.

- Salutation: Use a formal salutation, such as “Dear Mr./Mrs. [Last Name]”.

- Subject Line: Clearly state the purpose of the letter, e.g., “Subject: Explanation of [Issue]”.

- Professional Tone: Maintain a professional tone throughout, akin to writing a To Whom It May Concern letter & email.

How Do You Write an Informal Letter Explanation?

An informal explanation letter allows a more personal tone but still needs to clearly convey the message.

- Friendly Opening: Begin with a friendly greeting.

- State the Purpose: Quickly explain why you are writing the letter.

- Share Details Informally: Convey the explanation in a conversational tone.

- Personal Touch: Add personal remarks that relate directly to the recipient.

- Casual Closing: End with a warm, informal sign-off. You may also see Board Resolution Letter

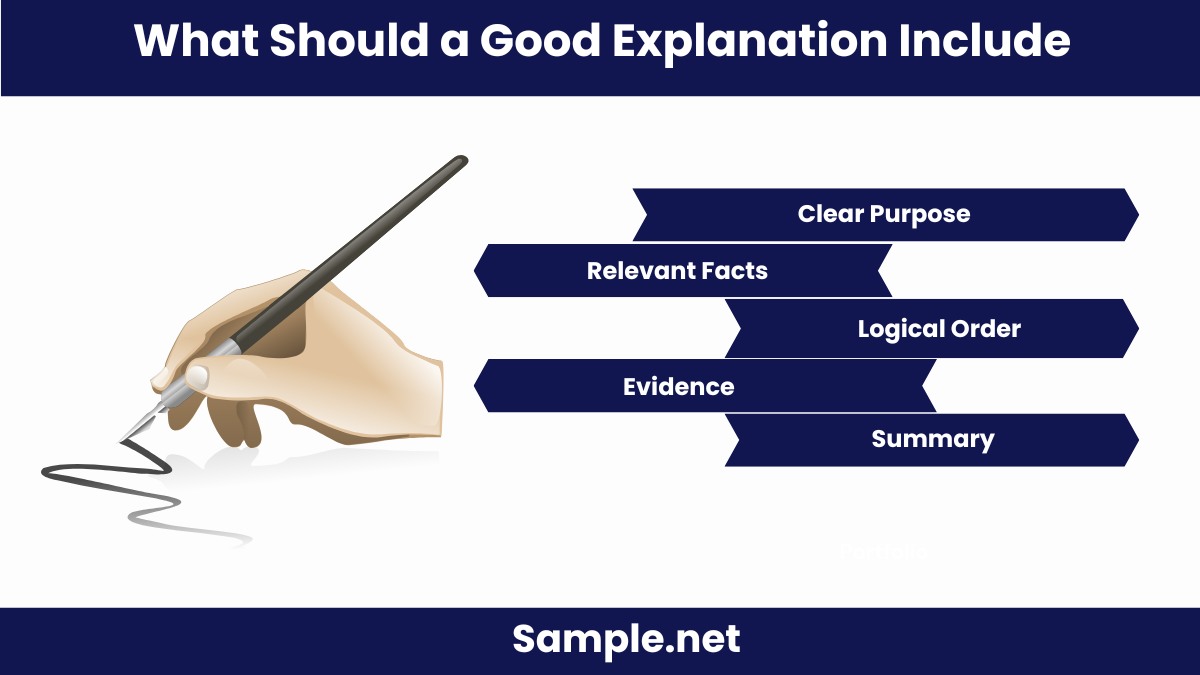

What Should a Good Explanation Include?

A good explanation provides all necessary details to clear up confusion and is understood by anyone who reads it.

- Clear Purpose: Define the purpose of the explanation clearly at the beginning.

- Relevant Facts: Include all relevant facts and figures.

- Logical Order: Present information in a logical sequence.

- Evidence: Attach or reference documents as evidence if applicable, such as a consent letter.

- Summary: Conclude with a summary of the explanation and offer further contact if needed. You may also see Explanatory Letter

What Are the Steps of Writing a Letter? Explain with Examples

Effective letter writing involves several structured steps to ensure clarity and purpose are maintained.

- Planning: Determine the letter’s objective and gather all necessary information.

- Introduction: Introduce yourself and state the purpose of the letter.

- Body: Write the main content of the letter, organized into paragraphs. You may also see Apology Letter

- Conclusion: Summarize the letter’s main points and state any required actions.

- Signature: End with your signature and name, using a format suitable for an event invitation letter.

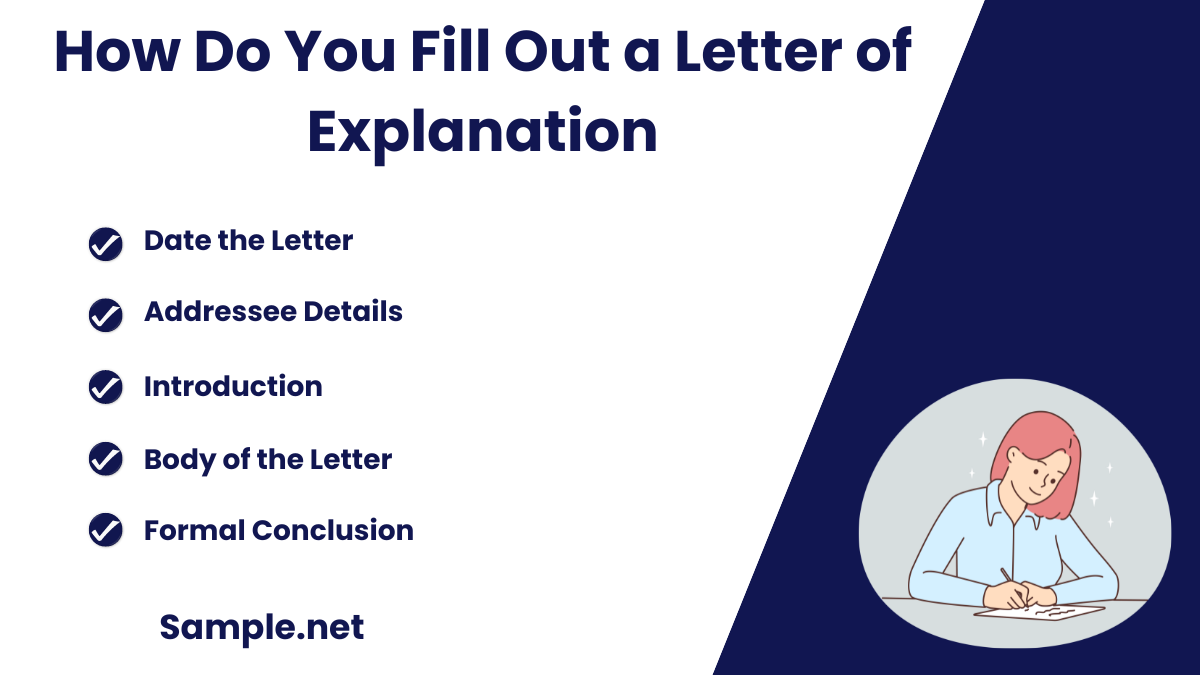

How Do You Fill Out a Letter of Explanation?

Filling out a letter of explanation correctly is crucial to ensuring your message is conveyed accurately.

- Date the Letter: Start with the date on the top left side.

- Addressee Details: Write the recipient’s name, title, and address.

- Introduction: Clearly state the reason for writing. You may also see Job Letter of Recommendation

- Body of the Letter: Fill out the details of the explanation as planned.

- Formal Conclusion: Close with a formal sign-off and your signature, similar to a permission request letter.

How Do You Start a Good Explanation Letter?

Begin with a polite salutation, introduce yourself if necessary, and clearly state the purpose of your explanation, using a tone appropriate for an authority letter.

How Long Should a Letter of Explanation Be?

A letter of explanation should be concise—typically one page or less—to ensure clarity and maintain the reader’s attention. You may also see Authorization Letter

How Do You Start Off a Letter?

Start off a letter with a professional greeting, address the recipient by name, and include a courteous opening statement, similar to starting a sponsorship letter.

How Do I End an Explanation Letter?

Conclude your explanation letter with a courteous closing statement, reiterate your willingness to provide further details, and sign off formally, akin to an appeal letter.

How Do You Conclude an Explanation Letter?

End your explanation letter by summarizing the key points, expressing your hope for understanding, and inviting further discussion if needed, which mirrors the close of a nomination letter.

Is a Letter of Explanation Necessary?

Yes, a letter of explanation is necessary when you need to clarify or justify situations or discrepancies, much like a salary increase letter would be used to justify a pay raise.

How Do You Write an Explanation Letter for Work?

Start by stating the purpose of your letter. Clearly explain the situation or issue, take responsibility if appropriate, and detail any solutions or steps you have taken, similar to a job reference letter.

In crafting an Explanation Letter, it is essential to be clear, concise, and honest. This type of communication can significantly impact how situations are perceived and resolved. By providing detailed examples and a format that can be adapted for various needs, this guide aims to assist you in drafting effective letters that convey your explanations with integrity and clarity. Whether accompanying a cover letter or standing alone, each Explanation Letter has the power to clarify doubts and build understanding, making them indispensable tools in personal and professional communication.