11+ Sample Debt Recovery Letters

-

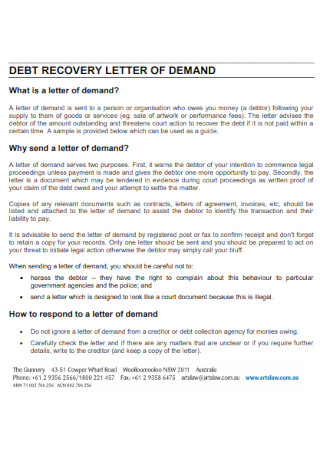

Debt Recovery Letter of Demand

download now -

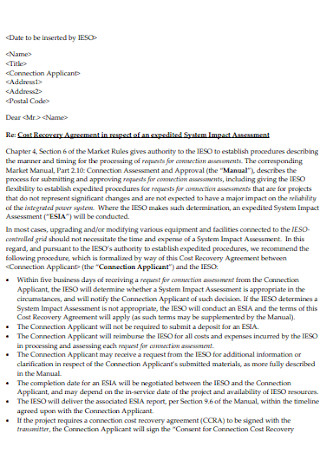

Debt Cost Recovery Letter

download now -

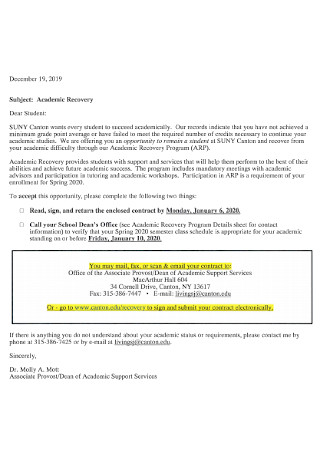

Debt Academic Recovery Letter

download now -

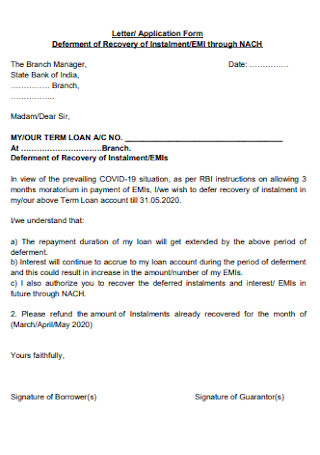

Debt Deferment of Recovery Letter

download now -

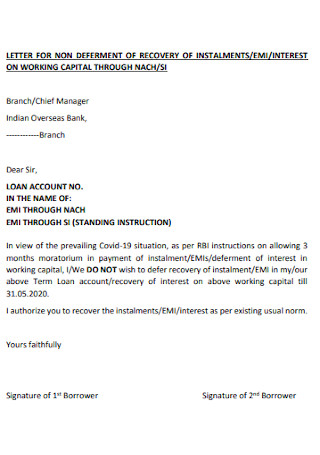

Letter for Non Deferment of Recovery

download now -

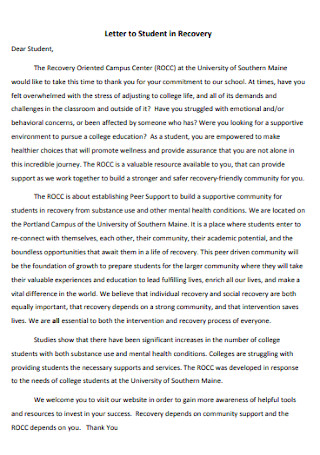

Letter to Student in Debt Recovery

download now -

Debt Recovery Coach Academy Letter

download now -

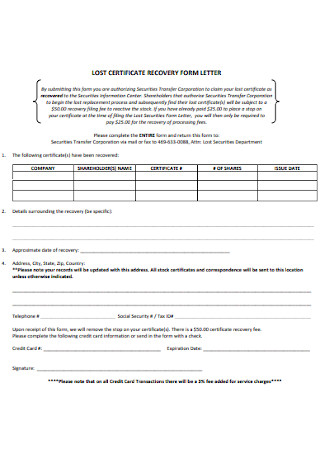

Lost Certifiicate Recovery form Letter

download now -

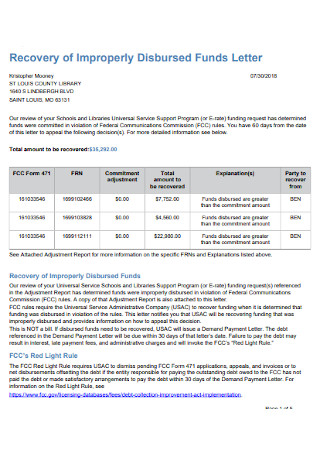

Debt Recovery of Funds Letter

download now -

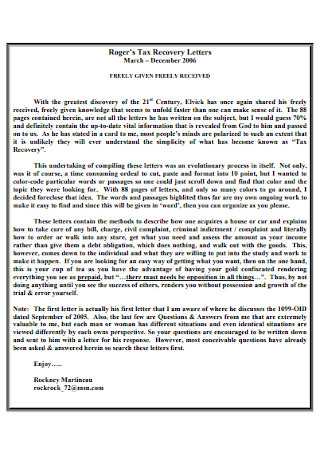

Tax Debt Recovery Letters

download now -

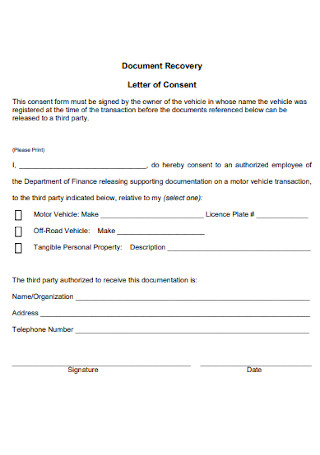

Debt Recovery Letter of Consent

download now -

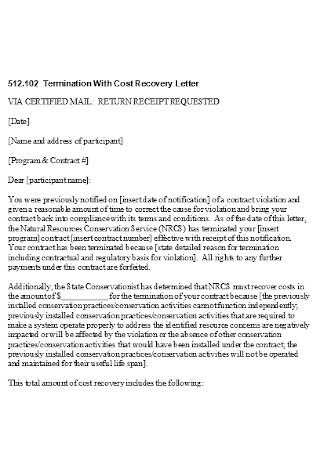

Termination With Cost Debt Recovery Letter

download now

FREE Debt Recovery Letter s to Download

11+ Sample Debt Recovery Letters

What Is a Debt Recovery Letter?

Benefits of Being Debt-Free

Tips on How to Get Out of Debt Fast

How to Stay on a Budget

FAQs

What is the debt recovery procedure?

Should I ignore my debt?

Can the creditor refuse the payment of the debtor?

What Is a Debt Recovery Letter?

A Debt Recovery Letter is a gentle reminder to your client or customer that they owe you or your organization money. Debt Recovery Letters should be utilized whenever a client or customer fails to pay an invoice timely. Debt Recovery Letters are the initial stage in the process of debt collection. Recent statistics indicate that the average success rate for debt collection agencies in the United States is between 20 and 30 percent.

Benefits of Being Debt-Free

Today, debt is a common occurrence in the United States. According to a report, approximately eight out of ten, Nearly 70% of respondents, would prefer not to be in debt. Still, they view it as a necessity, and a comparable percentage believe that loan agreements and credit cards have increased their life opportunities. These contradictory emotions reflect that debt can be beneficial and detrimental. Good debt is a valuable financial tool, allowing you to do things that will improve your financial situation in the long term, such as attending college, purchasing a home, or starting a business. Also, poor debt, such as credit card debt, merely burdens you with interest payments without boosting your income. This increases your reliance on borrowing to get through the month, trapping you into an endless debt cycle. Being in debt prevents you from doing everything you want with your money. However, its effects extend far beyond the financial sphere. Over time, the constant pressure of debt can also harm your health, relationships, and career. Eliminating your debt can improve your life in virtually every aspect.

Tips on How to Get Out of Debt Fast

Creating your plan to eliminate debt is feasible. Even with a low income, you can get out of debt quickly if you make fundamental lifestyle adjustments. However, turning your financial situation around only occurs sometimes. It requires dedication, organization, and self-discipline. Fortunately, it becomes easier as you develop improved spending habits. Take back control of your existence immediately. There are numerous methods to escape debt quickly. Check out these debt repayment suggestions:

1. Stop Borrowing Money

The first and most essential measure to getting out of debt is to stop making new loans: no more credit card use, no more loans, and no more debt. The most fundamental change that must occur is a shift in one’s perspective on finances and debt. To avoid accumulating more debt, you must comprehend the cost of using credit cards and obtaining new loans. Resolve to survive on cash while implementing your changes. You’re still in the beginning phases, so you shouldn’t worry about debt consolidation or balance transfers. You should only exchange one type of debt for another once you comprehend your financial situation and have a plan.

2. Track Your Expenditures

Determining where your money is going is the next step in rapidly eliminating debt. With a complete picture of what you pay for and how you spend money, it can be easier to determine where to make budget cuts. It is best to monitor your monthly bills and daily spending for at least one month. While tracking, pay attention to include your debt payment obligations. Regardless of the method you choose, make sure it is one that you will remember to use daily, and that will give you a complete picture of your spending.

3. Set up a Budget

After keeping note of your expenditures, you should create a budget plan. This budget should cover your needs using your typical expenditures as a guide. The monitoring will also reveal areas where you can reduce spending. You’ll be able to identify areas where you’re spending too much and where you can make cutbacks without sacrificing your quality of life. You may also discover places requiring modifications you wish to avoid making. To get out of debt, balancing livability and a strict budget is essential.

How to Stay on a Budget

Calculating and adhering to a budget can simplify achieving professional and personal objectives. Not only does sticking to a budget prevent you from purchasing items you cannot afford, but it can also help you pay off debts and develop savings more quickly. You may believe that creating an annual budget is difficult, but the real work begins after you’ve completed it. Because adhering to the budget requires constant practice, this is the case. Listed below are some helpful measures for sticking to a budget:

1. Invest in Yourself First

Savings are indispensable for anyone seeking a better future and should always be a top priority. This includes a tax-free savings account or a registered retirement budget, which should be opened after every paycheck slip. The most helpful way to achieve this is to automate your savings transfers as you would automate your bill payments. Paying yourself first is an effective strategy for reaching your objectives.

2. Consider Before Making Major Purchases

Spend at least a week contemplating purchasing something you do not require. Consider factors such as whether the large purchase comes with a payment plan agreement that could affect your budget or savings. Ensure you conduct a cost-benefit analysis to determine if the acquisition will add measurable value to your life.

3. Shop Alone

It is enjoyable to shop with family, but the habit can be financially draining. This is because at least one individual will feel compelled to acquire something. To avoid disappointing them or other family members, you may consent to the additional purchase, which may result in several purchases exceeding your budget. The most effective method to avoid overspending is to shop alone or set aside money for special requests. You always work diligently for your money, but when you need to make a purchase, you forget about it. This may explain the temptation to make large purchases, only to regret them when the money runs out. You can avoid this by equating your assets with the time you spent earning the money. Consider the purchase when $100 in shoes represents four hours of labor.

4. Negotiate Pricing

Always attempt to negotiate the lowest price a retailer can offer for a specific item. When you deal, you may discover discounts you would have missed had you purchased the item at the marked price. You have nothing to yield by asking for a value. The worst that a retailer can do is say “no.” It is common to incur unanticipated monthly costs that may strain your budget. You can prepare for these costs by saving money to cover the miscellaneous acquisitions. Keep track of these costs and determine if they occur frequently, as you will have to add them to your estimate budget if they do.

5. Track Your Purchases

Small purchases can significantly impact a person’s budget by the end of the month. Tracking your shopping habits, including dollar and five-dollar assets, is a beautiful strategy for identifying and avoiding them. By the end of the month, you can assess your overall expenditure and determine where you can make cuts. You can also combine small quantities of frequently purchased items and purchase them in volume at a discount. Second, since name brands are more expensive than generic brands, you may incur additional expenses when buying them. The amount may be tiny, such as when purchasing groceries, but monthly compounding makes such small amounts significant. Consider the value you receive for the additional cost and whether you would be better off buying a generic alternative.

FAQs

What is the debt recovery procedure?

When a loan, such as a credit card balance, remains unpaid and a creditor hires a collection service to concentrate on collecting the money, this is debt recovery. Debt recovery is crucial because it directly correlates with your credit score.

Should I ignore my debt?

It is never a good idea to disregard messages from debt collectors. It may make matters considerably worse for you. The debt collector may file a group lawsuit in court, resulting in the garnishment of your wages, the seizure of your personal property report, or the levying of funds from your bank statements.

Can the creditor refuse the payment of the debtor?

Generally, a creditor’s refusal to accept payment does not release the debtor from the obligation to repay the debt. This is because a simple denial does not cancel the debt. The debtor must locate the creditor and repay the debt, which you appear to have done.

The Debt Recovery Letter is a formal notice that must be delivered correctly. Check your contract to see what it specifies regarding legal notices. Any special laws regarding the delivery of messages must be adhered to. The most secure means to deliver your Debt Recovery Letter is in person, failing which by courier, mail, or email. Keep a copy of the signed letter and any additional materials. Are you prepared to write your letter of debt collection? Check out the templates provided above!