17+ Sample Credit Dispute Letters

-

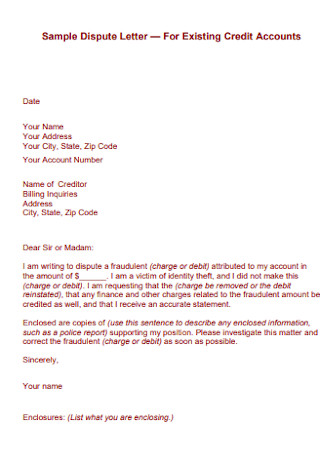

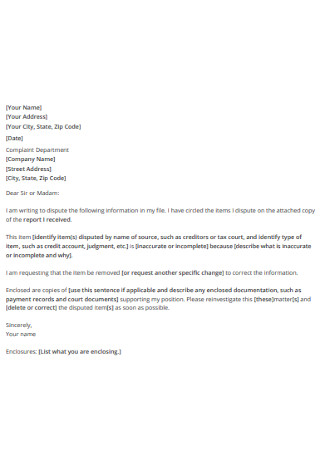

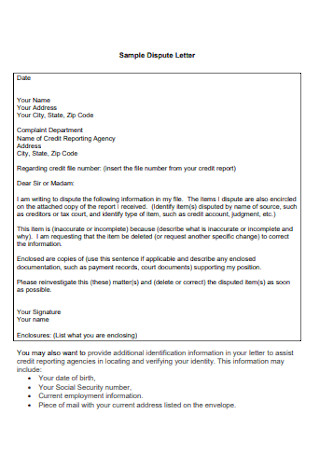

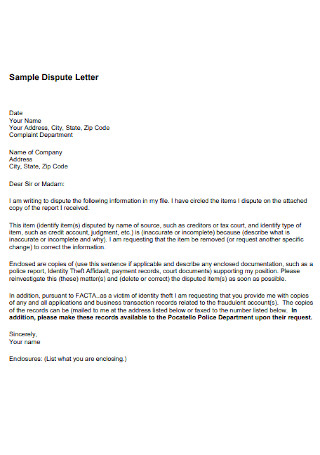

Sample Credit Dispute Letter

download now -

Credit Accounts Dispute Letter

download now -

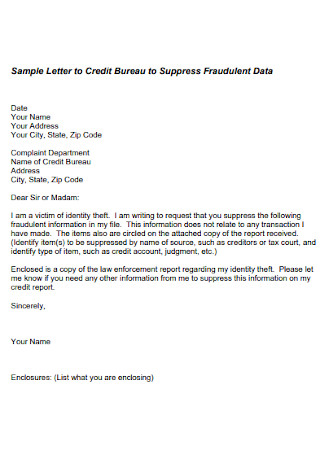

Credit Suppress Fraudulent Dispute Letter

download now -

Sample Credit Report Dispute Letter

download now -

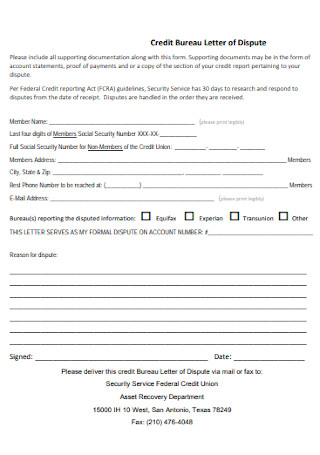

Credit Bureau Letter of Dispute

download now -

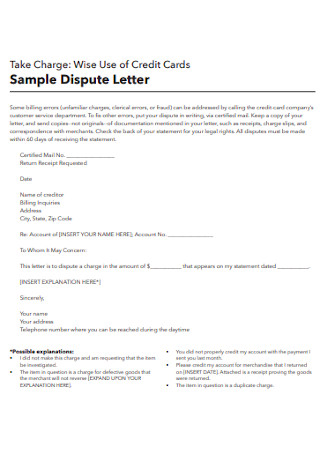

Sample Credit Cards Distribute Letter

download now -

Incorrect Credit Dispute Letter

download now -

Simple Credit Distribute Letter

download now -

Credit Dispute Report Errors Letter

download now -

Credit Card Letter of Dispute

download now -

Formal Credit Dispute Letter

download now -

edit Dispute Letter Format

download now -

Letter of Credit Disputes

download now -

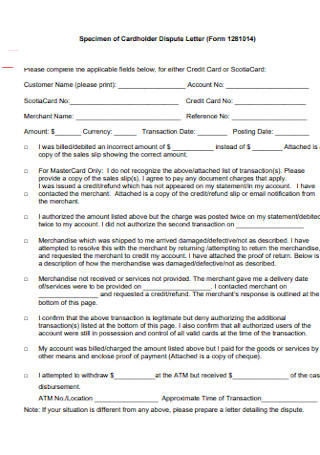

Specimen of Cardholder Credit Dispute Letter

download now -

Initial Debt Collection Dispute Letter

download now -

Business Letter of Credit Dispute

download now -

Sample Credit Dispute Letter Template

download now -

Standard Credit Dispute Letter

download now

FREE Credit Dispute Letter s to Download

17+ Sample Credit Dispute Letters

What Is a Credit Dispute Letter?

Parts of a Credit Dispute Letter

How to Dispute Errors in a Credit Report

FAQs

What is the importance of filing a dispute letter?

What happens when a denial follows a dispute raised on a credit report?

Does disputing a credit report affect a consumer’s credit score?

Which credit laws must a consumer remember?

A popular mode of payment at present is through the use of credit cards through credit. Most individuals use credit because it is convenient and easy to use. However, when a problem arises in a person’s credit report, the individual must address the situation immediately. The creation of a credit dispute letter is advisable to address a circumstance that concerns credit. It is essential to know the definition, components, and process of creating a credit dispute letter. Check out the article below to learn more about this type of letter.

What Is a Credit Dispute Letter?

A credit dispute letter is a written document to address a conflict concerning inaccuracies or errors in an individual’s credit report. The credit bureaus receive a letter from the complainant who highlights the disparities. The dispute letter aims to find a way to resolve the problem by excluding or editing the errors found on record. The letter identifies each item in the complaint, declares factual information, and includes a precise explanation about the exclusion or correction of the mistake. It is also necessary to attach documentation and highlight the particular items to support the claim made by the individual. Assure that the letter finds the correct credit bureau to ensure smooth coordination.

According to a study conducted by the Federal Trade Commission about the U.S. credit reporting agency dated February 03, 2013, five percent of consumers found errors on one of their three major credit card reports. The items include car loans and other insurances, making the individuals pay more because of services or products they did not acquire.

Parts of a Credit Dispute Letter

At present, most credit disputes are easy to process. Plenty of credit service bureaus and organizations offer online services and assistance to consumers that have a problem with their credit records. There are dispute resolution forms available on their websites. However, if it’s not possible, creating a credit dispute letter is the best alternative. The credit dispute letter includes the following information.

How to Dispute Errors in a Credit Report

Errors in consumer credit reports are more likely to occur than you think. As an individual, it helps to know and identify the mistake on the credit report before the issuance of a dispute letter. Here are the steps to disputing an unwanted error in a credit report.

Step 1: Accurately Identify All Errors in the Report

The most reliable way to check for credit mistakes is through a meticulous examination of the copy of the credit record. Free annual credit reports are made available from each credit bureau through the website, AnnualCreditReport.com. The credit reports are also available for unemployed individuals as a job requirement, recipients of government grants and assistance, or if the individual is a victim of identity theft. Some states have laws regarding free credit reports and are entitled to receive their copies of the record. It is advisable to review all credit reports from the three credit bureaus to ensure there are no errors in any of them.

Step 2: Classify Which Errors Are Disputable

In all technicality, a consumer is allowed to despite any erroneous information found in a credit report. However, the credit bureaus only delete or update items the law permits them to change. Under the law, bureaus are allowed to amend information that is inaccurate, incomplete, and unverified. Some details remain in the credit record for a definite period. Negative entries older than seven years are allowable to be amended or disputed. Late payments made on time, other accounts, inaccurate information about credit amounts, creditors, and account statuses are examples of credit disputes honored by the credit bureaus.

Step 3: Determine the Means of Communicating the Dispute

At present, there are different ways of communicating with the credit bureaus, either through online, mail, or phone calls. Online transactions are the most convenient. However, if the consumer uses online transactions, the results of the dispute are only available online. It is also difficult to complete the online process if the bureau requires supporting documentation transfers through the mail. Each bureau provides its landing page for matters about disputes and is easily accessible and navigable. Addressing the conflict through mail takes additional time but gives enough evidence if the bureau does not respond promptly.

Credit bureaus process investigations for 30 days and up to 45 days if there are further documents. If the bureaus fail to answer within the time frame, the consumer has the right to sue in court. The dispute letter explains the reason for the removal of the dispute in detail and accuracy. Attach all necessary documents with a return receipt request as proof of the dates included in the process. If the consumer opts for a phone call, they must record the time of the conversation, the representative’s name, and information relating to the discussion.

Step 4: Wait for a Response Regarding the Dispute

The credit bureau can address the dispute earlier than 30 days and deletes the item in question. However, if the bureau finds sufficient evidence that the information is legitimate after deleting these items, the credit bureau must notify the consumer in writing. All data presented for the investigation of inaccurate detail reverts to the company that provided the information, and the organization must review and report back the findings to the bureau. Upon completion of the process, the bureau gives the consumer a complimentary copy of the record with changes present. Note that disputes found in one credit report must appear in the others. It is necessary to check records from all the bureaus to find the inaccuracies. There are instances where the creditor verifies the disputed information. In this instance, it is advisable to discuss the dispute with the creditor.

FAQs

What is the importance of filing a dispute letter?

A credit report considerably influences a person’s credit score. A low credit score prevents individuals from applying for credit loans, credit cards, including job and housing opportunities. A credit report involves information relating to a consumer’s address up to bill payment history. Credit reporting identities sell the data present in the credit report to individuals or agencies related to creditors, insurers, employers, and other organizations to evaluate applications for credit, loans, insurance, and employment. Financial advisors encourage consumers to review their respective credit reports periodically. It is necessary because the credit report reflects information that affects loan applications and approvals, including the value of money. It also ensures the items on record are accurate, complete, and current before applying for loans or major purchases. It also safeguards the consumer from identity theft. Identity thieves may use the information to make unsolicited purchases and create a new credit account under the consumer’s name. Inaccurate information affects credibility and credit score.

What happens when a denial follows a dispute raised on a credit report?

Initial investigations started by credit bureaus are not always reliable. The process results in the contact of the primary creditor or reporting entity and inquiring if the item on record is correct. The creditor must provide documentation to verify the debt; however, it is not always substantial. As a result, the dispute remains unsettled and denied, and the incorrect items still appear on the credit report. If the problem persists, follow up the dispute by collecting and relaying the necessary information to support your case. Supporting documentation includes letters from creditors, canceled checks confirming payments, and actual billing statements. There are instances where the consumer overlooked some data without realization.

In this situation, it is advisable to check past credit reports where inaccurate information starts to appear. Afterward, contact the creditor and make necessary arrangements to catch up with payments, and ask the creditor to adjust the credit reports sent to the bureaus. When the credit bureaus deny the change in the disputed information, it is helpful to seek advice from a financial advisor. The experts can help in addressing the problems that the consumer may have overlooked. A good credit counselor helps legally improve credit scores. Stay away from advisors that seek to raise credit rankings immediately and question every item in a credit report. However, the best way to resolve disputes is time. Even if it continues, work on restoring the credit score instead. Remember to pay bills on time, keep the balance low on credit limits, and always observe the credit report.

Does disputing a credit report affect a consumer’s credit score?

Filing for a dispute does not, in any way, impact the credit score. However, if there are changes made after addressing the conflict, the outcome can influence the credit scores. Late payments negatively affect a consumer’s credit score. Eliminating the inaccurate details indicated in the credit record increases the credit score. The dispute only changes the content found on the credit report through the challenges raised by the consumer if it is proven inaccurate. If the conflict is unsuccessful and the lender’s or creditor’s bank statement is accurate, the item remains in the report. It will not affect the credit score of the consumer in any way.

When the dispute is about personal information corrections or updates, including name, address, and social security number, the credit score will not affect the consumer’s credit score. Note that all names and addresses of the customer are stored in the bureau’s database, including past addresses and disclosed nicknames and aliases. However, if the consumer notices any unauthorized and unfamiliar transactions from various names and addresses, it may be a sign of identity theft and must be immediately reported to the concerned credit bureaus. It is desirable to raise a dispute on the fraudulent items or transactions appearing on the credit report and file a police report of the illegal activity.

Which credit laws must a consumer remember?

There are plenty of credit laws that cover the rights of consumers and help to understand the process of addressing problems that arise. Consumers must have familiarization with these five credit laws.

- Equal Credit Opportunity Act (ECOA): The act restricts lenders from discriminating against people or institutions based on non-financial factors. These factors include gender, race, color, religion, marital status, age, or disabilities. Under the ECOA, lenders must explain why an individual’s application for credit led to a denial. It must be within 60 days of the date of the decision and elaborate on the reasons for the rejection.

- Fair Credit Reporting Act (FCRA): The act defines how consumer credit information is collected and used by credit bureaus and other consumer reporting agencies. The FCRA gives consumers the right to review free credit reports upon request from each credit bureau and several consumer reporting agencies. The FCRA gives consumers the right to question and dispute items that are inaccurate on credit reports.

- Fair Debt Collection Practices Act (FDCPA): The federal law governs what third-party debt collecting bodies do when collecting a debt and only applies to personal debts. The FDPCA defines when debt collectors are allowed to make contact with individuals. Under the FCPCA, the person has the right to sue a debt collector for violations of rights.

- Truth In Lending Act (TILA): The act defines what information the lenders disclose when customers apply for credit products, services, or loans. Under the TILA, the lender must disclose the annual percentage rate, fee charges, financed amount, payment schedule, and total repayment amount in the loan term.

- Credit Repair Organizations Act (CROA): The act applies to persons or organizations taking money in exchange for improving credit. Under the CROA, credit repair companies disclose all information of a client’s credit history and discourage lying to current and future creditors. Any company that asks its client to waive rights is punishable under CROA.

It is essential to be aware of credit purchases for the goods and services a consumer receives. There are plenty of ways to check if the credit report is factual and accurate based on the purchases an individual makes. The three credit bureaus offer free copies of the credit report and encourage consumers to raise disputes for inaccuracies. Remember that the credit report influences an individual’s credit score, and negative items on the credit report negatively impact the credit score. It is necessary to review the credit reports from all credit bureaus to avoid any false entries and correct them immediately. The phrase “Prevention is better than cure.” applies even to managing credit. Check out the credit dispute letters sample above and ensure entries on your credit report is true and accurate.