20+ Sample Validation Letters

-

Permit Validation Letter

download now -

Debt Validation Letter

download now -

Sample Validation Letter

download now -

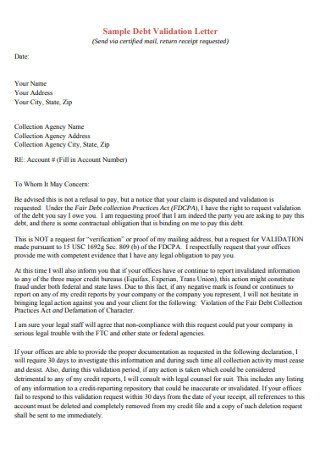

Sample Debt Validation Letter

download now -

Supplier Validation Letter

download now -

Sample Bank Validation Letter

download now -

Rogers Device Certification Letter

download now -

Validation Finding Letter

download now -

Software Validation Letter

download now -

Simple Validation Letter

download now -

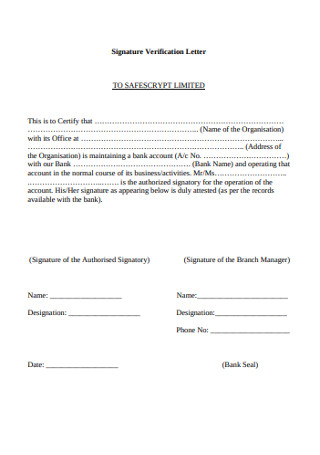

Signature Validation Verification Letter

download now -

Basic Validation Letter

download now -

Validation Collection Letter

download now -

Sample Identity Validation Letter

download now -

Standard Validation Letter

download now -

Endorsement Validation Letter

download now -

Printable Validation Letter

download now -

Validation Certification Letter

download now -

Business Validation Letter

download now -

Single Validation Activity Letter

download now -

Direct Validation Letter Template

download now

FREE Validation Letter s to Download

20+ Sample Validation Letters

What Is A Validation Letter?

Reasons Why People Write Validation Letters To Collectors

How To Write A Validation Letter To A Debt Collector

FAQs

What happens when you dispute a debt?

When should you dispute a debt?

Can disputing hurt your credit score?

What Is A Validation Letter?

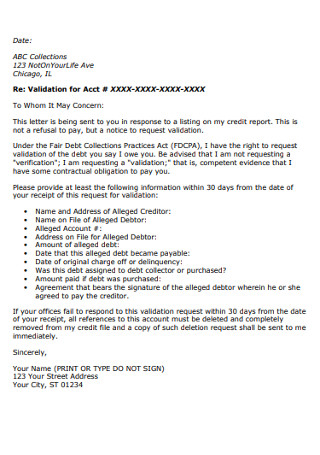

Let’s say around 2016, you canceled your membership in a country club. You paid your remaining balance for the month and stopped thinking about it again. Just today, you found a notice in your mail that you owe the country club an extra $ 900, and it has gone to collections. Something seems off about this situation. Do not get scared and immediately pay the amount. The first thing you should do is write the collection agency a validation letter. Under the Fair Debt Collection Practices Act (FDCPA), you have the legal right to ask the debt collector to send you a written debt validation notice containing all the necessary information about the debt they wish to collect, also known as a debt verification letter. By sending a validation letter to the debt collector, you can confirm the debt with certainty and do not have to worry about paying a wrongful debt.

Reasons Why People Write Validation Letters To Collectors

Receiving an intimidating call from a debt collector about an alleged debt you owe may pressure to immediately pay the debt and get it over with. This holds true especially when you know the debt is yours or if you are in the process of applying for a loan agreement and want to clean your credit report. However, if you have uncertainties about the debt collection, this may prompt you to inquire and investigate. Paying a debt that does not belong to you sounds like a rip-off. Hence, whenever possible, you should exercise your right to request verification of a debt. Below are a few reasons why people write and send validation letters to debt collectors.

1. To Verify that the Debt is Theirs

Wrongful debt collection happens as often as you think. which is why writing a debt validation letter is an extra safety precaution that you should make to protect yourself, your hard-earned cash and your credit score. It is not novelty news that collection agencies send bills and make calls for bogus debts. Do not be too trusting and expect that a bill from a collection agency means you owe them money. The first thing you should do is question it outright especially when you do not recall procuring any debt. Make your own investigation and determine whether the demand is legit.

2. It Helps Them Better Understand the Debt

Receiving a call from a debt collector may cause confusion on your part, particularly when you are not the type of person to incur any debt. By sending a validation letter to the collection agency, you will be able to ask for the information regarding the alleged debt. Information such as the exact amount of the debt, a computation or breakdown of the debt, information about the original creditor which you owe the debt to, and if possible, other supporting documentation of the debt that will help you better understand it.

3. To Clean Up Their Credit Report

If you are applying for a loan or mortgage from a bank or credit institution, they will need to look at your credit report. An unpaid debt from a debt collector will reflect on your credit report and will not look good to the loan or mortgage officer. If you have paid the amount of the debt, or feel like the debt is not yours, you should write a validation letter to the collection agency and verify your payment or dispute the debt and request for it to be removed from their data. Removing it from their database will clean up your credit report and help your credit scores to be more appealable.

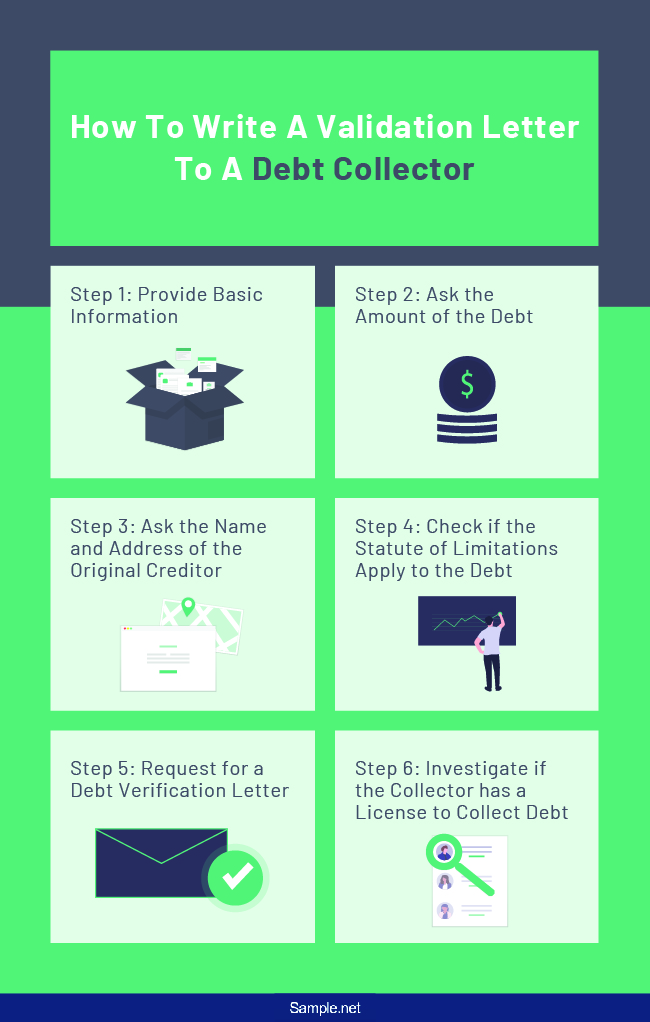

How To Write A Validation Letter To A Debt Collector

Unpaid debt can really hurt your credit scores. If you genuinely believe that the debt does not belong to you, then the best approach is to send the collection agency a validation letter. The validation letter is not a dispute letter per se since it merely asks the debt collector to verify the debt information. To help you start writing the letter, below are some steps that can guide you.

Step 1: Provide Basic Information

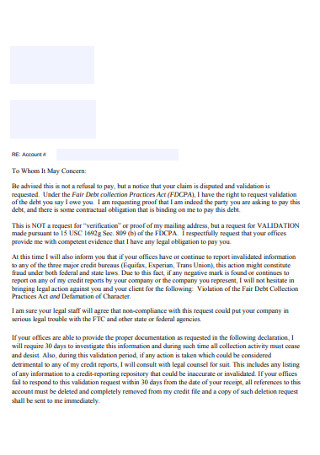

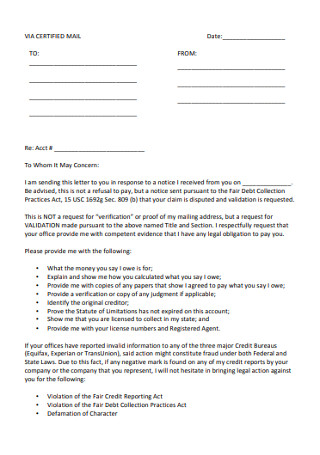

It is important that you include your name, address, and contact information in the letter so the collection agency knows you are serious in removing negative information from your credit report. Make sure you make it known to the agency that you are not disputing the debt outright but merely asking for verification. When you automatically dispute a debt, this prompts the collection agency to immediately take action. Don’t be surprised if you find a demand letter from them the next day. Hence, the first paragraph of your validation letter should contain the phrase “This is not a refusal to pay or dispute the account but a request in pursuant to the Fair Debt Collection Practices Act 15 USC 1692g Sec. 809 (b) whereas a collection agency you are required to provide verification for the debt you wish to collect.”

Step 2: Ask the Amount of the Debt

The primary reason you are sending the validation letter to the collection agency is to confirm the amount of the debt, and if it really belongs to you. Ask the agency for the exact amount of debt and a breakdown of how the debt came to be. Consider including in your letter “If you could kindly provide me with the complete and correct amount you claim I owe you and please explain to me how you have computed the amount. If possible, provide me a copy of any documentation you have to support the alleged amount.”

Step 3: Ask the Name and Address of the Original Creditor

By knowing who the original creditor is, it may give you clues if you really do owe the money. The original creditor can be a shop you frequent going to which you keep a tab with, a subscription provider you had a previous subscription plan with, an organization you used to be a member or any person or entity you had a previous transaction with. Ask the collection agency to identify who the original creditor is and when the transaction happened.

Step 4: Check if the Statute of Limitations Apply to the Debt

If the debt has surpassed the allowed time for it to be collected, then there is no use writing a validation letter to the collection agency. If the statute of limitations for the debt has expired, the collection agency cannot sue you for the recovery of debt since their right to do so has also expired. The statute of limitations for debts varies from state to state and the type of debt. Generally, debts are categorized into four-types: written, oral, promissory notes, and open-ended accounts. Check your local state law regarding debt statutes of limitations, and you may not have to pay your debt collector.

Step 5: Request for a Debt Verification Letter

The collection agency must clearly and convincingly prove that the specific debt really belongs to you before they are able to collect it. If they cannot demonstrate that you legally owe the debt, you have every right to write them a cease and desist letter so they can stop harassing you. Under the Fair Debt Collection Practices Act, they have 30 days from receipt of your letter to send you a written debt verification letter. When writing your validation letter, consider clearly asking that they send you a verification letter including proofs such as a copy of the bill containing the debt or copy of the judgment.

Step 6: Investigate if the Collector has a License to Collect the Debt

Make sure you are not being scammed. Ask the collection agency to show you their license number and registered agent. Wait for the agency to reply and provide you the license number of their business operation and investigate if the agency is legit. You do not want to waste your time writing the letter or hand your hard-earned money to a scammer. Once everything is in order and you have finished writing the validation letter, make sure you send it through registered mail and keep the receipt as proof of mailing.

FAQs

What happens when you dispute a debt?

If you ever receipt a bill from a collection agency that does not belong to you, then your option is to dispute the debt. Once you signify your intention to dispute the debt, the agency has to stop debt collecting activities until it complies and sends you proof that verifies the debt. If he is unable to provide such proof, then he has to stop bothering you again. If he does not stop bothering you, then he may be liable for harassment. However, if he does provide the necessary documentation that proves the debt, then he may report it to a credit reporting agency and note that the debt is being disputed. In this case, prepare yourself, you might receive a subpoena from a court requesting your presence to defend yourself in a collection suit.

When should you dispute a debt?

Under the Fair Debt Collection Practices Act (FDCPA), you have 30 days from receipt of the debt demand letter to dispute the claim. Within that 30 day period, if you are uncertain of the correctness of the claim, you can send the collection agency a validation letter so they can verify the information contained in the claim such as the correct and exact amount of claim, the name of the original creditor, when the credit was incurred, and other necessary and relevant documentation that can verify the debt. In the same light, the credit collection agency has another 30 days to form and compile a response that will provide you the asked information and confirm that the debt is certainly yours.

Can disputing hurt your credit score?

Disputing a debt collection does not hurt your credit scores. In fact, if you win the dispute and prove that the debt collection is wrongful, the information in your credit report will change and reflect that the bad debt has been eliminated. In turn, it elevates your credit scores.

Receiving a phone call from a debt collector telling you you owe money can be scary. It is even scarier when you don’t recall making the debt. The first thing you should do when confronted with this situation is to verify the information. You can outright ask the collection agency for proof that it is indeed you that owes the debt. To do this, you will need to write them a validation letter requesting to verify the debt that you allegedly owe. Once you send your letter, wait for their response, and then determine if you need to pay the debt obligation.