3+ Sample Mortgage Contract

FREE Mortgage Contract s to Download

However, home ownership is not a dream one easily gives up on due to the lifelong benefits it provides, the first and prominent one being a roof on top of your head, that is why most aspiring homeowners apply for a mortgage loan to make this dream a reality. Before doing so, one must secure a Mortgage Contract that this article will expound more on below. We also prepared Mortgage Contract samples and a run-through of the basic concepts that your Mortgage Contract is likely to contain and you most certainly want to look out for so if you want to find out more about what a Mortgage Contract is, read the rest of this article!

What is Mortgage Contract?

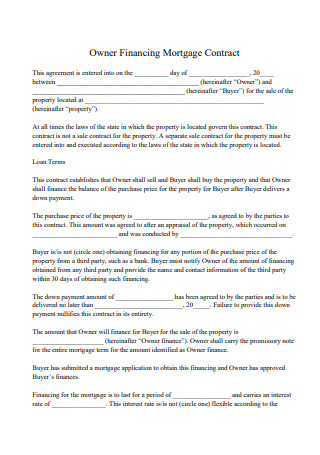

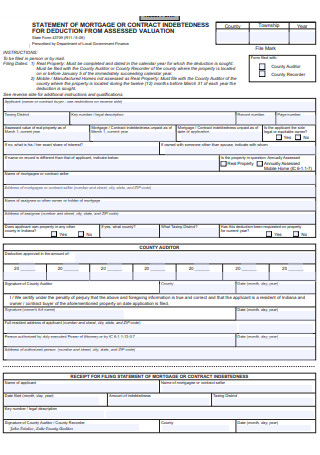

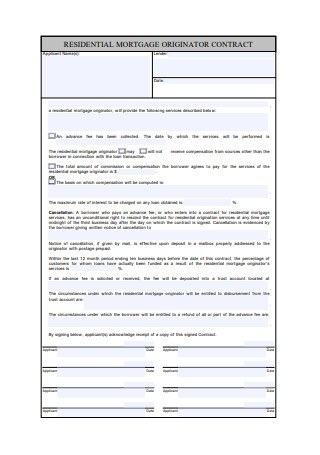

A Mortgage Contract is a legally binding document between the lending bank of choice and the borrower. According to this contract, the borrower will be able to purchase their dream home after having been granted a loan by the mortgagee so in a way, the contract can function as your pledge to comply with the established payments and should you choose to otherwise, the bank has legal rights to take possession of your homes. A Mortgage Contract is necessary for transactions when you want to borrow money to own a real estate or a property, you are to lend money on someone who wants to purchase a home or property and if you are an independent lender or at least manages a company that makes loans.

The ABCs of a Mortgage Contract

Before the article goes deeper into what a mortgage is, let us first establish the terms and their definitions as you are likely to see them all over your Mortgage Contracts and are terms you ought to have a basic understanding in before making big decisions that could potentially impact the rest of your life for the better, or for worse.

Amortization: This refers to the process of paying off a mortgage loan through regularly scheduled and equal installments that include both interest and principal. Amortized Mortgage: An Amortized Mortgage is a type of an Amortized loan in which the borrower has to repay in regular installments in accordance to the agreed loan amortization schedule to fully repay the loan made. Amortization Period: The Amortization Period is the length of time that will take before a mortgage is repaid in full. For example, if your mortgage has a 40-year amortization period, this means that it should take 40 years before your balance is reduced to a zero, assuming that payments are regularly made and are of equal amount as agreed on in the terms.Annual Percentage Rate (APR): This is defined as the annual interest rate that you must pay on a loan and is usually represented by a percentage.Appraisal: An Appraisal would be the rough, unbiased estimate of your home’s value. This is required by the mortgagees in order to validate that the amount of money that the borrower requests from the lenders is appropriate and ensure that the money they are loaning is not worth more than the home’s value.Appraisal Report: This is a written report that states the estimated value of a home or property. An opted type of Appraisal Report is a Narrative Appraisal Report as it thoroughly describes the methods used to arrive at the estimated value. To solidify claims, the report must be supported by data and solid computations. Arrears: Arrears will only reflect in your credit files if you are unable to pay for your payments in the required time asked of you to do so. If you keep this up, your home or property is most likely to be repossessed by your mortgagee. Assets: An asset is anything that you own that has monetary value. This is needed for the lender to verify that you are financially capable of covering the mortgage even when you face unfavorable events concerning financials. In the context of a mortgage, assets will include but are not limited to: Properties, vehicles, jewelries, money in your savings accounts, Certificate of Deposits (CDs), pensions, and stocks. Capital: The Capital refers to the amount that the borrower will request to make an investment for their home or property. Closing Disclosure: A Closing Disclosure is a form that is five pages in length providing the borrower the final details, including the terms and costs of the agreed upon mortgage loan. Mortgage lenders are required to provide this form at least 3 days before completing the transaction and before the loan closes. Because it outlines the final information on your mortgage loan, this must be thoroughly reviewed and understood hence the three day window which you should be able to optimize that should you have any concerns and supplemental questions, they have to be queried immediately to the lender.Collateral: Like a Promissory Note, the Collateral in the context of a mortgage is a pledge and essentially an asset made by the borrower to assure the lender that they are capable of making the payments. It could be likened as the lender’s safety net in the case that the borrower defaults on the mortgage loan, especially for loans that are huge in quantity. If the borrower is unable to make the payments, the lender is legally allowed to be in possession of the collateral assets to make up for the financial loss. Credit Report: A Credit Report that can function similarly as a financial report is a thorough breakdown of the borrower’s credit history for the lender to evaluate your finances. The credit history should detail payments made in the past as well as income and expense statements and outstanding debt levels. This is required by the mortgage lender to determine your financial ability to repay the mortgage loan. Credit Score: The Credit Score pertains to the rating that lenders give you before they are to identify the amount of money to lend to you and your likelihood of paying the installments and ultimately make the decision to move forward with the application for a mortgage loan. It ranges from 0-999 with 961-999 being the excellent score that could afford you the best mortgage deals with lower interest rates. 881-960 and you could still be eligible for some of the best mortgage deals. 721-880 and you could be approved for deals with the appropriate interest rate. 561-720 will get you mortgage deals although higher in interest rates and finally, a very poor score of 0-560 might not even get you any mortgage deal unless it’s coupled with a high interest rate. A credit score of this rate will be denied a mortgage deal. Deed: The Deed would be the tangible document that proves your ownership of a property. Down Payment: The Down payment or the initial bank deposit that you make and is usually not refundable. This must be be paid in cash and paid up-front. This is the partial payment that mortgage lenders require you before you are finally able to purchase a home under the terms and conditions of your Mortgage Agreement. While most mortgagees will require a 20% down payment, some would offer as little as 3%. Escrow: Most mortgagors will be made an escrow account which you can liken to a savings account except it will be managed by a third-party mortgage servicer or an escrow agent if you will, and will hold the assets or funds in behalf of the parties involved who are currently in the process of finalizing the mortgage transaction. They will remain in-charge of the funds until the parties involved have complied with the terms and conditions stated in the contract. Fixed-Rate Mortgage: A fixed-rate mortgage refers to the loan made that has a fixed interest rate all throughout the entire loan period. Most mortgages under a fixed interest rate are Amortized Loans. This is the usual preference of borrowers because the interest rate is not affected by market conditions and borrowers are more sure of how much they should pay on a monthly basis. Mortgage: A mortgage is a loan or the funds that a mortgage lender, usually credit unions and brokers but mostly banks, lends you for you to finally purchase that dream home or a property you have been working hard for. Because this is a loan, it must be paid back over time or there will be consequences, the worst being owing more money in the form of penalties and interest charges as well as required appearances in court that if it does come to the point, you must attend. Mortgagee: The mortgagee or the lender would be any entity and financial institutions that mainly function to lend money to the borrower or the mortgagor with a specific purpose of owning a home or a property. Mortgage Deed: A Mortgage Deed, also referred as the Mortgage Agreement, is the physical document that officially recognizes the agreement that the mortgagee and the mortgagor has made. It details the loan amount, the interest rate and everything that is in relation to the loan that has been granted by the lender to you. Mortgage Promissory Note: This is the written agreement that attests of the borrower’s promise to repay the mortgage loan acquired form the mortgage lender. The Mortgage Promissory Note shall also explain how the loan will be repaid including when should the payments be made and for how long should the regular installments be paid. Mortgage Rate: This is the interest rate charged on your mortgage. A lender is responsible for determining the interest rate on the loan and your credit history and credit score will largely serve as a lender’s basis. Mortgagor: The mortgagor or the borrower is any individual, couple or entity that borrows money for the sole intent of home or property ownership. They will only be granted the money after a process that begins with an assessment of their financial status and capabilities of repaying the loan they request. Preapproval: A preapproval is a document that assesses the amount of money you are able to borrow to purchase the home of your desires. This is likely to be the first and important step in acquiring a mortgage as it’s during this process that a lender would go over and verify your employment, income, assets, credit history and and credit score to identify which loan option best fits your current financial status, the amount of money you are eligible to borrow as well as the interest rate. Be sure to distinguish the Preapproval from a Prequalification because while they may be used interchangeably, they are technically not the same. The latter is not as thorough in their evaluation of your finances since they do not involve asset and income verification. Principal Payment: The Principal would have to be the amount that you borrowed. Its amount decreases over time if you were to pay your payments regularly.

Advantages of a Mortgage Loan

It allows you to budget.

Homeownership comes with a cost and one of this is to be cautious and ever mindful of your budgeting. That being said, you must have a budget plan in the first place keying in the Mortgage Loan under the Fixed Expenses heading to ensure that a fixed amount from your income would be going into your Mortgage savings.

It is an affordable way of owning a home.

As mentioned, home ownership is probably one of the things everyone fantasizes about. Applying for a mortgage loan will make this affordable since the interest rates are relatively lower than other kinds of loans, especially personal loans. The loan granted to you is also one that is best adjusted to fit your current financial status so it allows you to pace your payments and manage them on a level that you are able to.

Disadvantages of a Mortgage Loan

You pay more than what you borrow.

Due to the interests and the additional fees placed on your monthly payments, you are likely to end up paying more than your principal amount. This is why it’s important to be meticulous of the fees and to pick a type of mortgage that you understand and is the most suited to your financial situation to avoid monthly surprises.

FAQs

What is a Contract for Mortgage?

A Contract for a Mortgage is a legally binding agreement between the mortgagor and a mortgagee wherein the latter is effectively mandated to adhere to the terms and conditions and fulfill the duties stated in the contract that should mostly be in relation to the monthly installments.

What are 3 types of Mortgage?

- Fixed Rate Mortgage: The interest rate is consistent throughout the period regardless of the fluctuations of interest rates in the general market.

- Variable Rate Mortgage: This a the complete opposite of a fixed rate in the sense that for this particular type of mortgage loan, rates can change at any time which is why this type of mortgage requires you to have extra savings allotted for your mortgage payments in the case that the interest rate does increase.

- Standard-Variable-Rate Mortgage (SVR): Like a Variable Rate Mortgage, monthly installments can increase however unlike a Variable Rate Mortgage, it can also decrease depending on the changes of the interest rates.

Which Type of Mortgage is the best?

Choosing the mortgage option can be considered as an important factor for you to carry out your payment abilities. You must go for the option that your financial status can afford but with the various mortgage loan types, it might be confusing to choose one. A go-to mortgage is the Fixed Rate Mortgage that according to the Financial Conduct Authority, 90% of homeowners go for. It’s popularity is probably because the amount you pay is stagnant therefore you can easily determine how much of your income can you budget to go into paying the loan. With no changes in the rates, you are also assured that repayments won’t have to increase therefore there is less anxiety and pressure to fulfil the contract’s condition of paying on time.