22+ SAMPLE Accounting Agreement

-

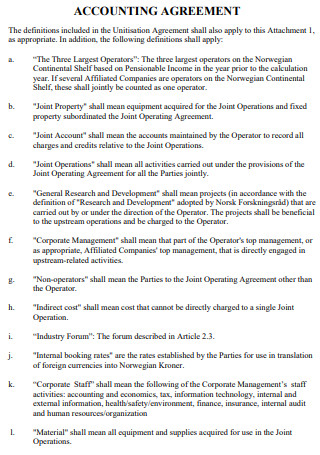

Accounting Agreement

download now -

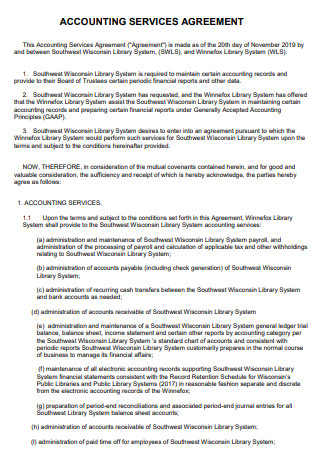

Accounting Service Agreement

download now -

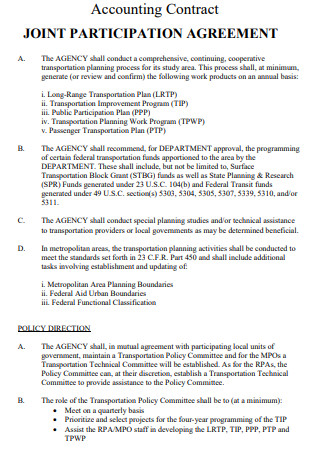

Joint Accounting Participation Agreement

download now -

Articulation Accounting Agreement

download now -

License Accounting Agreement

download now -

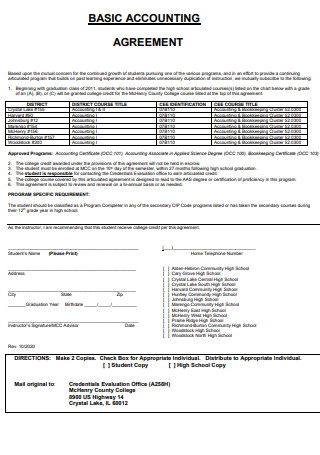

Basic Accounting Agreement

download now -

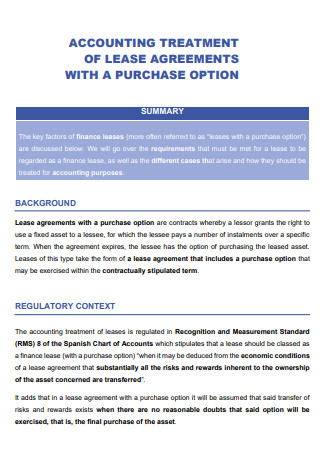

Accounting Treatment of Lease Agreement

download now -

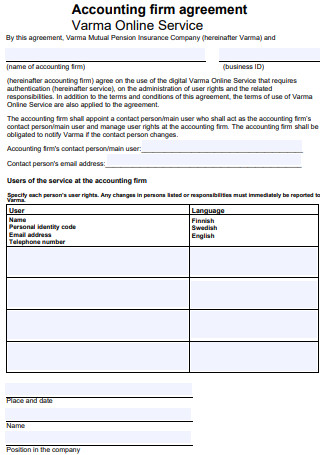

Accounting Firm Agreement

download now -

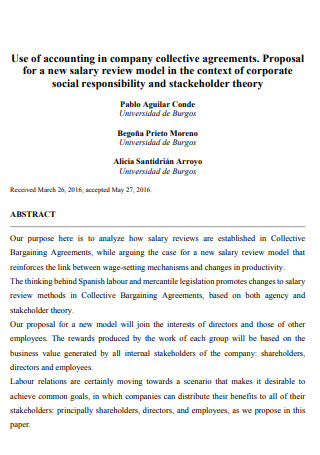

Accounting Collective Agreement

download now -

Accounting And Data Processing Agreement

download now -

Reporting And Accounting Agreement

download now -

Unit Accounting Agreement

download now -

Greenhouse Gas Accounting Agreement

download now -

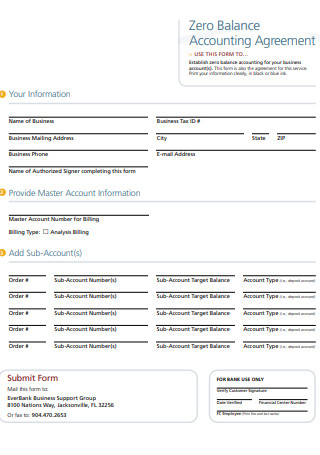

Zero Balance Accounting Agreement

download now -

Accounting Tax and Payroll Agreement

download now -

Accounting Firm Partnership Agreement

download now -

Accounting for Hire Purchase Agreements

download now -

Service Level Agreement Requirements of an Accounting

download now -

Information And Accounting Agreements

download now -

Accounting Transfer Agreements

download now -

Accounting for Chance Agreement

download now -

Accounting Financing Agreement

download now -

Sample Accounting Agreement

download now

FREE Accounting Agreement s to Download

22+ SAMPLE Accounting Agreement

What Is an Accounting Agreement?

What’s Inside an Accounting Agreement?

How to Create an Accounting Agreement

FAQs

How different is accounting from bookkeeping?

Why is this document important?

How is accounting information often used by business owners?

What Is an Accounting Agreement?

First and foremost, we need to define what is accounting all about. Well, in its most basic definition, refers to the process of collecting and summarizing business and financial activities, as well as evaluating, validating, and reporting the resulting data to oversight authorities, regulators, and tax collection bodies. What happens to these results, you may ask? Well, the data that is gathered from these reports are then used to make judgments about how to run the company, invest in it, or lend money to it. Accounting is a critical role in making decisions, cost planning, and assessment of economic performance measurement in all businesses, which is why they need this function, no matter how big or little they are.

In the case of various companies that specialize in accounting (known as accounting firms), they need to deal with their respective clients properly and protect their interests while engaging in business with them. A legal document known as an accounting agreement will make this possible. Businesses that want specific portions of their money handled and people with particular accounting requirements both require an accounting agreement. When a company wants to create a professional connection between a client and an independent accountant, they utilize this agreement. Furthermore, when it comes to financial adherence and guidance, this document protects both clients and accountants, which is why it is required anytime a client agrees to conduct business with the accounting company. In other words, this document aids in the setting of expectations and the reduction of the risk of conflict between the parties concerned.

What’s Inside an Accounting Agreement?

In order to be effective in serving its purpose, an accounting agreement needs to have the following key components in place:

How to Create an Accounting Agreement

Here are the steps that should be followed when creating an accountant agreement in order for it to be effective:

1. Identifying the Parties Involved

In creating an accounting agreement, or any type of agreement, the first thing that should be done is to identify the parties involved and who’s who throughout the entire time that the agreement is in effect. In the case of an accounting agreement, the parties involved are the accountant and the client. The role of the accountant in this agreement is to provide the services to the client as needed in a professional manner and within the client’s best interest. The role of the client in this agreement is to communicate everything that they need to the accountant so that it may be addressed properly and without any problems.

2. Drafting the Main Clauses

When the parties involved in the accounting agreement have already been identified along with their roles, the next thing that needs to be done is to draft the main clauses of the agreement. What are considered to be the main clauses of the agreement? Some of the main clauses of the agreement include the engagement, the term, the compensation, the relationship, and the confidentiality clause. The engagement clause dictates in writing the main responsibilities of the client and the accountant. The term basically determines the start and end dates of the agreement. The compensation clause determines the amount to be paid by the client to the provider, when and how it is going to be provided, and if there are any additional expenses that should be included. The relationship clause basically states that the accountant acts as an independent contractor of the client and not as a full-time employee, and the confidentiality clause serves to protect any trade secrets or confidential information that may be shared throughout the course of the agreement.

3. Drafting the Boilerplate Clauses

When the main clauses of the accounting have already been drafted, the boilerplate clauses will then come next. Boilerplate clauses are also known as standard or general clauses that are present at the end of most legal documents such as this agreement. Some of the boilerplate clauses in this agreement include the representations and warranties clause and the severability clause. The representations and warranties clause states that all parties concerned in this agreement represent that they are properly authorized to engage in the agreement. The severability clause of the agreement states that an ineffective provision of the agreement shall be considered null and void and shall be removed from the document while those that are effective will continue to do so.

4. Verifying the Document

Once the main and boilerplate clauses have already been drafted, it’s time to verify the entire document, which also serves as the last step. In this step of creating the agreement, verify if there are any clauses that have missing or inconsistent wording that may cause it to be ineffective. Additionally, check if everything that needs to be included is present in this document. A good tip here would be to seek legal help in verifying this document. Once everything has been verified and the document is deemed to be complete, the parties involved can then proceed to pen their signatures to put this agreement into action.

FAQs

How different is accounting from bookkeeping?

Although accounting and bookkeeping are both components of the same process, which is to keep your financial records in check, they serve different objectives. On the one side, bookkeeping focuses on documenting daily financial transactions and activities, whereas accounting analyzes, strategizes, and plans taxes using that financial data.

Why is this document important?

An accounting agreement is important since unmanaged or erroneous accounting services may cost clients thousands, if not hundreds of thousands of dollars to rectify. Furthermore, because accountants are viewed as trustworthy advisers with access to sensitive financial information, they may violate corporate ethics and privacy, which might be disastrous for all parties involved. This document, when effectively written, will prevent such scenarios from happening.

How is accounting information often used by business owners?

Accounting information is constantly used by business owners to build budgets for their firms. Company owners may use historical financial accounting data to get a thorough look at how their organizations have spent money on various business tasks. They may also use this accounting data to create future budgets, ensuring that their firms are on the right track financially.

As stated earlier, an accounting agreement protects the interests of the parties involved (the client and the accountant) whenever they do business with each other by holding them accountable when providing financial records in order to make sure that they are accurate and up to date. This document also helps all parties involved establish a professional relationship through the course of the agreement. If you find yourself in difficulty when creating this document, this article contains sample templates that should serve as a solid foundation/reference when you need to make one.