54+ Sample Payment Agreements

-

Simple Payment Agreement Template

download now -

Installment Payment Agreement Template

download now -

Monthly Payment Agreement Template

download now -

Sample Instalment Payment Agreement Template

download now -

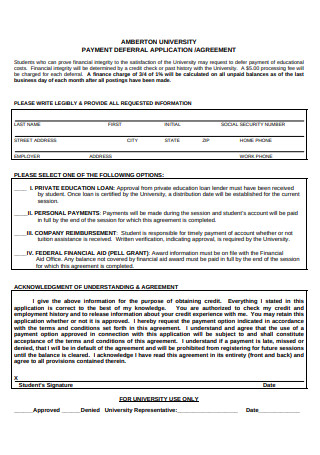

Student Payment Arrangement Agreement

download now -

Printable Payment Agreement for Outstanding Balance

download now -

Payment Rent Agreement Format

download now -

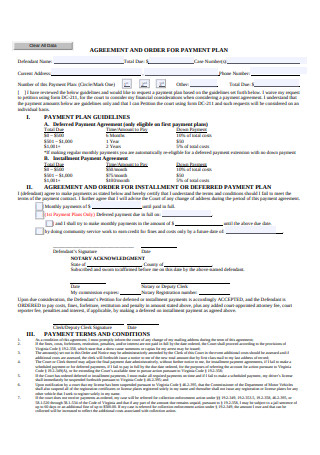

Payment Debt Plan Agreement

download now -

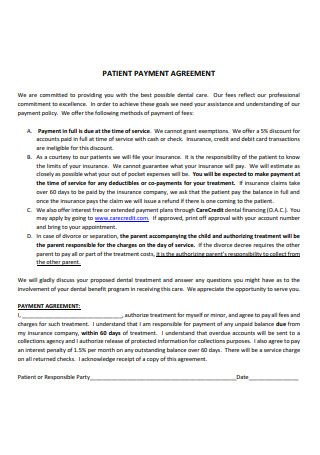

Patient Notarized Payment Agreement

download now -

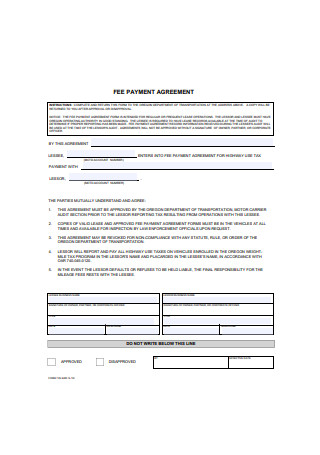

Simple Contract Fee Payment Agreement Form

download now -

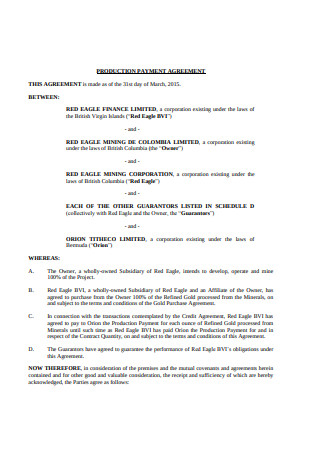

Production Loan Payment Agreement

download now -

Tuition Money Payment Agreement

download now -

Payment Schedule Agreement Example

download now -

General Legal Payment Agreement Form

download now -

Sample Partial Payment Agreement

download now -

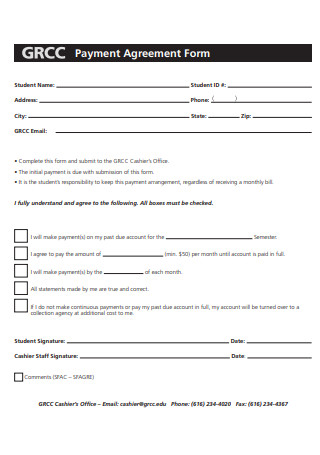

Payment Agreement Form

download now -

Personal Tuition Account Payment Agreement

download now -

Payment Plan Agreement Format

download now -

Business Online Bill Payment Settlement Agreement

download now -

Employee Payment Agreement Sample

download now -

Automatic Notary Recurring Payment Agreement

download now -

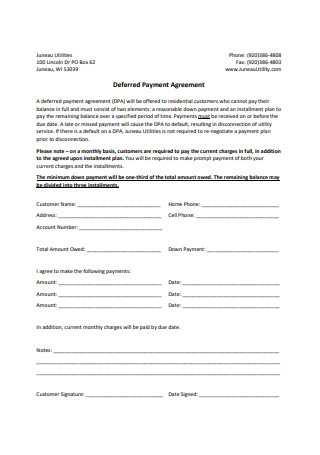

Deferred Child Support Payment Agreement

download now -

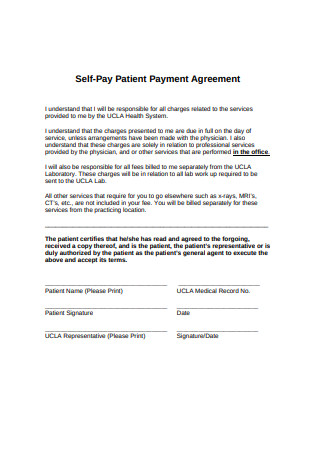

Self-Pay Purchase Patient Payment Agreement

download now -

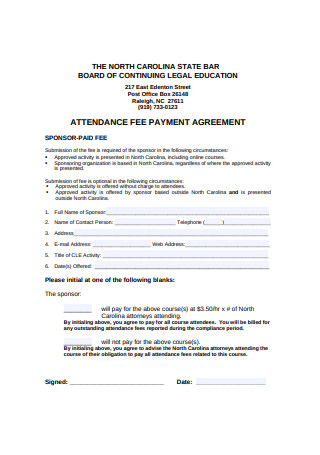

Attendance Fee Payment Agreement

download now -

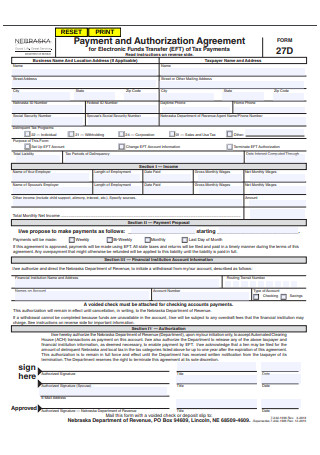

Payment and Authorization Agreement

download now -

Simple Payment Agreement

download now -

Sample Payment Plan Agreement

download now -

Simple Payment Agreement Format

download now -

Basic Payment Agreement

download now -

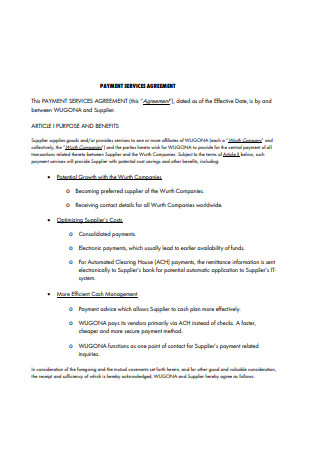

Payment Services Agreement

download now -

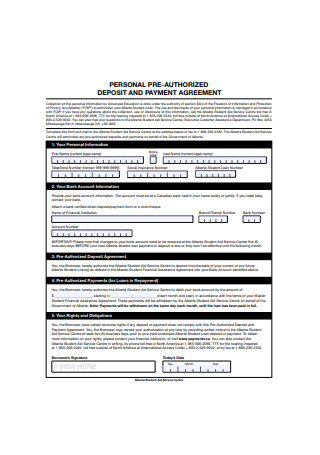

Pre-Authorized Deposit Payment Agreement

download now -

Sample Payment Agreement Form

download now -

Basic Payment Agreement Format

download now -

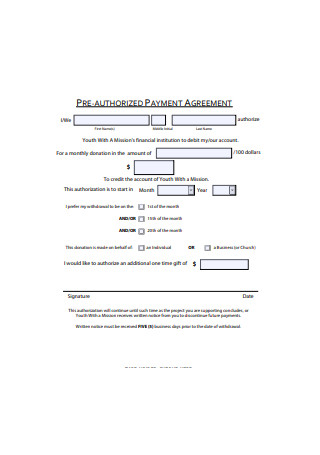

Pre-Authorized Payment Agreement

download now -

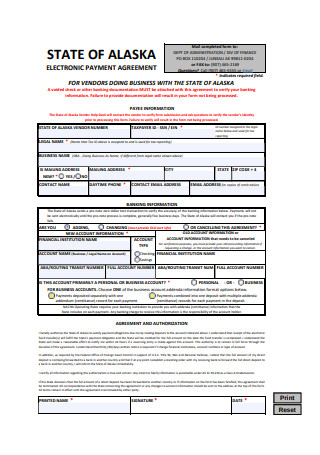

Electronic Payment Agreement

download now -

Basic Payment Agreement Form

download now -

Tuition Fee Payment Agreement Format

download now -

Standard Payment Agreement

download now -

Installment Payment Agreement

download now -

Joint Payment Agreement

download now -

Assessment Payment Agreement

download now -

Bill Payment Agreement

download now -

Budget Payment Agreement

download now -

Client Payment Agreement

download now -

Online Bill Payment Agreement

download now -

Standard Payment Agreement Format

download now -

Payment Deferral Agreement

download now -

Student Payment Agreement Format

download now -

Bill Payment Service Agreement

download now -

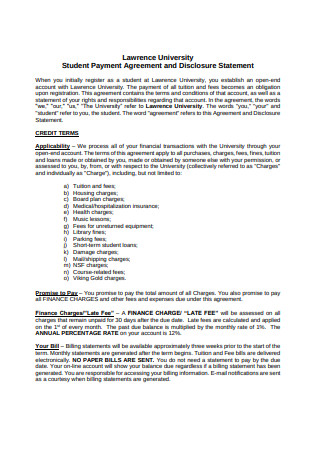

Student Payment Agreement and Disclosure Statement

download now -

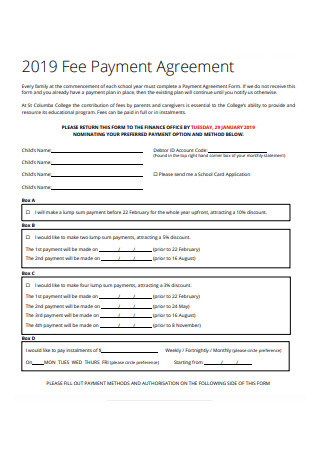

Sample Fee Payment Agreement Form

download now -

Monthly Payment Plan Agreement

download now -

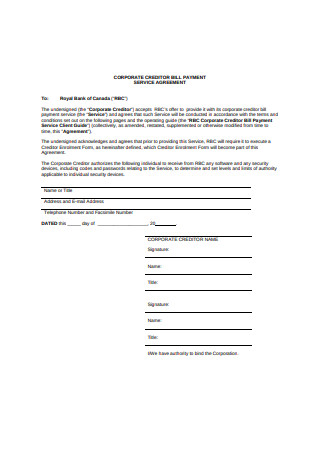

Corespondent Credit and Payment Agreement

download now -

Deffed Payment Agreement

download now -

Booking and Payment Agreement

download now

FREE Payment Agreement s to Download

54+ Sample Payment Agreements

What Is a Payment Agreement?

Tips to Keep Track of Your Payment Plan

How to Compose a Standard Payment Agreement

FAQs

What is a demand letter?

What happens if you disregard a demand letter?

How much do you pay an attorney for a demand letter?

What is a payment letter?

When is the right time to send an invoice to a customer?

What Is a Payment Agreement?

When we purchase goods from stores, supermarkets, or online shops, we usually get receipts. These receipts serve as an acknowledgment of our payments. A payment agreement is a receipt that comprises the specifics of a loan. It outlines the stipulations a loan agreement typically has. If you plan to borrow or lend money or apply for amortization, you will need a payment agreement. This agreement will organize all important information concerning payment and also the lender-borrower relationship. While payment agreements come in many forms, they all have one goal—to receive what is due for the service or product given. It can be an installment plan, personal payment arrangement, or business payment agreement.

Tips to Keep Track of Your Payment Plan

According to Statista, in 2019, Tennessee had a personal bankruptcy rate of 496.8 individuals per 100,000, and Alaska had 52.34 per 100,000. Bankruptcy happens when a borrower no longer has money to pay for his/her debts. Since we are talking about loans and payment, here are some tips to keep track of your payment plan. With these tips, a borrower will be able to pay off his debts consistently, and a lender will receive payments as agreed.

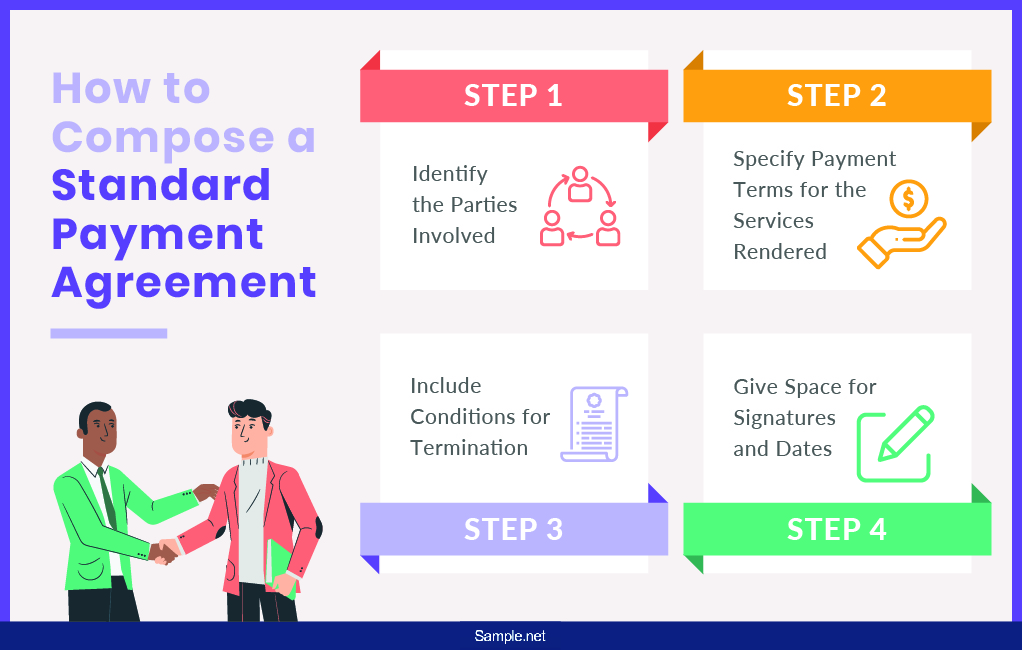

How to Compose a Standard Payment Agreement

A written agreement is key to any business proceeding. A payment agreement is a proof that a lender and a borrower have come into terms. Additionally, it gives both parties similar thoughts on what to expect from each other while being bound to the contract. The following are steps on how to compose a payment agreement.

Step 1: Identify the Parties Involved

In the earlier section of the agreement, you must identify the legal and complete names of both the payer and the lender. Also, take note of the date the agreement effectuates. Without this section, the entire contract will be invalid.

Step 2: Specify Payment Terms for the Services Rendered

Specify the goods or services provided and the payment that is due. Give a clear description of what was rendered. Then, determine the payment schedule. Is it going to be on a monthly, quarterly, or annual basis? Keep a list of the exact dates for payment. Moreover, set the method for payment, if it can be through cash, check, credit card, or even bank transfer. Add in policies and specify the additional charges in case fees are not being paid on time.

Step 3: Include Conditions for Termination

As we’ve mentioned earlier, not all plans continue as they should. In your contract, include conditions for termination. Write in detail how termination is to proceed along with a specific timeline. Commonly, the party who desires to terminate the contract has to send at least a 30-day prior notice. In addition to that, incorporate provisions for dispute resolution in case conflicts arise later on. Also, it is important to take note of the state laws that will govern your contract.

Step 4: Give Space for Signatures and Dates

In the last section of the agreement, give space for the parties involved to date and sign the contract. The signatures of both will finalize the agreement and make it come to fruition. Remember to make copies of the agreement and let them sign the original copies for keeping.

FAQs

What is a demand letter?

According to Investopedia, a demand letter is a document one party forwards to another to request for payment. The person who receives the letter may have violated the contract. Attorneys usually write this document, but it is not legally binding. Individuals use it to remind the violating party of his/her payment duties. If the violator refuses to submit, then the sender may bring the issue to court. Note that in the United States, the state laws and the Fair Debt Collection Practices Act lays out rules on how debt collection is to be performed.

What happens if you disregard a demand letter?

If you happen to receive a demand letter, ask help from your lawyer. Most people think that simply ignoring one will resolve the issue, but that is not the case—especially if the sender hired an attorney. Confront the issue immediately instead of allowing it to reach the court. Courts will not be in favor of those who disregard demand letters. You can negotiate with the sender and maybe ask for a lesser payment amount. It is better to deal with disputes as early as possible than wait for it to get worse.

How much do you pay an attorney for a demand letter?

A lawyer creating a demand letter may take at least 5 hours of his/her time. These hours may be spent in consultation, researching, drafting, reviewing, etc. A lawyer with so much experience may charge you $275 per hour. That is pretty expensive. Some lawyers may only charge for an hour. In other words, fees mainly depend on the law firm or the lawyer himself/herself.

What is a payment letter?

A payment letter is a paper that reminds a customer of his/her unpaid bills. Some may forget to pay their bills on time because of tight schedules. Any entity who has the right to receive payment can make this letter. Even if it is asking for delayed payments, it should still be written politely.

When is the right time to send an invoice to a customer?

An invoice is a file that records dealings between a seller and a buyer. It can be a sales invoice, receipt, or debit note. Businesses bill their customers through an invoice. Unless a customer is asked to pay ahead of time, an invoice is usually sent after a customer receives the goods or services.

If you own a lending business and you want it to generate profit, you must keep a payment agreement with you. Keeping one is like keeping your money in a bank. You will have the right to take your money when it is time. On the other hand, if you are a borrower, you must keep up with a payment agreement because it is a legally binding document. You may be borrowing money for a good reason. Therefore, think of a payment agreement as a driving factor for you to reach your goals.