8+ Sample Debt Settlement Agreements

-

Debt Marital Settlement Agreement

download now -

Chemical Debt Settlement Agreement

download now -

Simple Debt Settlement Agreement

download now -

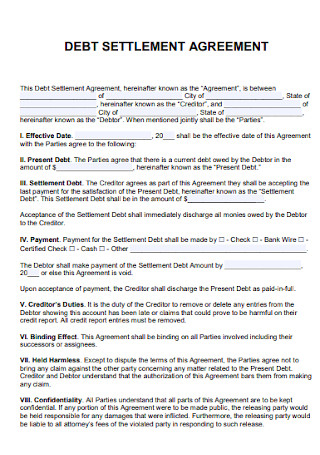

Debt Settlement Agreement Format

download now -

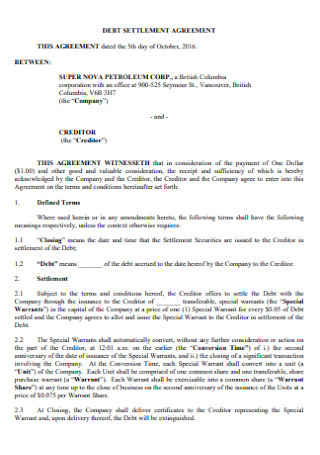

Debt Settlement Agreement for Corporation

download now -

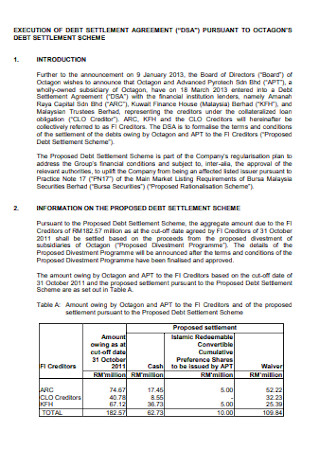

Execution of Debt Settlement Agreement

download now -

Municipality Debt Settlement Agreement

download now -

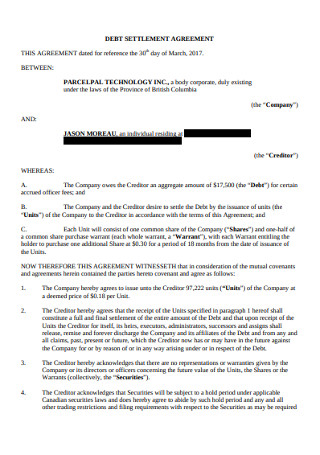

Sample Debt Settlement Agreement

download now -

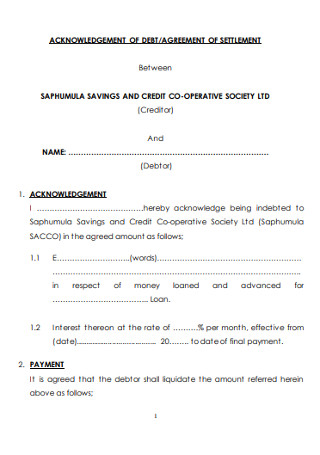

Basic Debt Settlement Agreement

download now

FREE Debt Settlement Agreement s to Download

8+ Sample Debt Settlement Agreements

What Is a Debt Settlement Agreement?

Benefits of Debt Settlement

Tips to Avoid Debt

How to Negotiate a Debt Settlement Agreement

FAQs

Will my credit score go up after debt settlement?

Is it better to settle or pay in full?

Can I get a loan after settlement?

What Is a Debt Settlement Agreement?

Debt settlement occurs when your debt is settled for a lesser amount than what you owe, with the promise that you will pay the agreed amount in full. Debt settlement, also known as debt relief or adjustment, is typically handled by a third-party company, although you could take it on your own. Not all creditors accept debt settlements, which could cause more financial damage than good in some cases. 77% of American households have a debt of some kind.

Benefits of Debt Settlement

If a creditor’s willingness to accept a portion of what you owe in exchange for the cancellation of the remainder of your debt might be good to be true, it usually is. Outside of the debt settlement industry, consumers view debt settlement as a risky endeavor, partly because it can be a haven for con artists. Sometimes, the thrown life preserver will not keep your head above water. However, consumers considering debt settlement are aware of their limited options. And the advantages for these individuals are worthy of consideration.

Tips to Avoid Debt

Debt can harm your financial well-being, but it need not be the enemy. If you incur debt for a desirable cause, and if paying it back fits comfortably within your budget, debt can assist you in developing sound financial habits, enhancing your credit, and achieving your objectives. However, there are occasions in which it is preferable to avoid debt. For instance, credit card debt for which you can only afford the minimum monthly payment can result in sky-high interest rates and poorer credit ratings. Another illustration is a car loan with a monthly payment that strains your budget. This can put you in danger of falling behind on payments and hinder your capacity to pay other essential expenses. These six suggestions can help you remain on the right side of debt, which means only incurring debt when it is necessary, affordable, and beneficial.

1. Build an Emergency Fund

It may sound contradictory, but an emergency fund is essential for avoiding debt. Experts advise saving three to six months’ worth of necessary expenses, or more if your work is seasonal, freelance, or unpredictable, to provide a financial cushion in the event of job loss. A second use for an emergency fund is to pay for unforeseen expenses that would otherwise be charged to a credit card. Use your emergency fund to pay for unanticipated costs such as car restorations or dental work if possible. In this way, you can avoid accumulating credit card debt that could take years to repay.

2. Choose a Spending Plan

If you consistently make purchases you cannot pay off at the end of each month; overwhelming credit card debt might sneak up on you. Creating a strategy for each dollar you earn is a unique approach to avoid overpaying. A budget might be as general or as specific as necessary. It may involve separating your spending into needs, wants, and short- and long-term financial objectives with the plan or utilizing one account for set expenses and another for discretionary spending with the two-account approach. A zero-based budget allocates every dollar to a specific purpose, so you know precisely where your money is going. Regardless of your system, you will develop the habit of tracking expenses and ensuring you spend less than you earn.

3. Stick to a Routine of Savings

Automating your savings plan makes building an emergency fund simpler than saving for other goals, such as retirement budgets. Additionally, separating this money from your checking account makes you less likely to spend it and incur debt. Set up monthly transfers to your emergency fund, retirement fund, and college savings account if you do not contribute directly from your paycheck to a workplace. The optimal amount to save depends on your specific cases, but if you use the 50/30/20 allocation as a guide, you should allocate roughly 20% of your income after taxes to savings and debt repayment.

4. Pay Your Full Credit Card Bill Each Month

Credit cards may encourage you to purchase expensive products you cannot immediately afford, given that you can pay off the debt in installments. This can be beneficial if, for example, you need to make an extensive home repair but want to utilize only some of your emergency fund. Only purchase products for which you will have sufficient funds in your checking account by the due date. You will never incur interest charges, and your credit utilization will remain low, perhaps boosting your credit score. Moreover, you will not incur debt that may be difficult to eliminate.

5. Only Borrow What You Need

When seeking other forms of credit, such as a vehicle, mortgage, school, or personal loan, choose the smallest debt to help you achieve your objectives. A significant down payment on a car or home might help reduce your monthly payments. Mainly, student loans should be considered a last resort for college after federal, state, and school grants, private scholarships, and work-study funds have been exhausted.

6. Keep Your Credit Score Strong

It may be impossible to avoid debt if you want to buy a house, attend college, or purchase a car. With a decent credit score, you can limit your monthly payments and obtain a cheaper interest rate. The higher your credit score, the more probable it is that not only will a lender accept your application, but you will also receive the best possible terms, thereby saving money. Numerous fundamental debt avoidance activities can boost your credit score. Maintaining a low debt-to-credit ratio, paying all bills on time, and limiting the amount of new credit you apply for are all important methods to build good credit.

How to Negotiate a Debt Settlement Agreement

If you feel as though you are drowning in debt, the thought of settling for less than you owe can be appealing. You could hire a debt settlement company to negotiate settlements with your creditors on your behalf. Before dropping your accounts, you may need to accumulate enough money to pay the creditor plus the settlement company’s charge. Consequently, working with a debt settlement company may lengthen the process and cost you more money overall. Although many creditors may be willing to settle your debt for smaller than you owe, there is no assurance that debt settlement will be successful. If you’re thinking about attempting it on your own, here are some steps you may want to take:

1. Assess your situation

Create a list of your past-due accounts, including the names of your creditors, the amount you owe, and the amount of time you are behind on payments. This list will serve as the foundation for your plan and help you prioritize which accounts to tackle first. This may be a preferable option if you believe you can afford to make minimum payments or stay current on your accounts with a hardship payment plan. Debt settlement can save you money, but it’s not guaranteed to work, can harm your credit, and may incur additional fees in the interim.

2. Research your creditors

When creditors accept a settlement offer and how much they will take can vary by the creditor. For example, a creditor may need at least 90 days of delinquency on an account before settling. Or, certain creditors may not settle at all, requiring you to wait until the debt is sold to a new entity. Some creditors may be more prone than others to sue you to gather an unpaid debt. It may be prudent to negotiate settlement agreements with these creditors initially. You can conduct online research to learn about others’ experiences and shape your proposal, but keep in mind that their outcomes may not reflect the company’s current procedures.

3. Start a settlement fund

Although you will not be required to refund the total amount, you must still pay something to settle an account. Typically, creditors may demand a lump sum payment of 20 to 50 percent of the total amount owed. You may be able to pay this amount over numerous monthly installments, although doing so may incur additional fees. You may open a new bank account for your compensation fund so you are not tempted to spend it elsewhere and avoid unintentional overdrafts throughout the settlement procedure. Make consistent deposits into the account to accumulate sufficient funds to make an acceptable settlement offer. It may be prudent to maintain your settlement funds in a statement not managed by a creditor with whom you are negotiating, to prevent the company from gaining insight into your financial situation.

4. Make a debt settlement offer to the creditor

Once you believe you have sufficient funds to pay a debt, you can contact the creditor and make an offer. In rare instances, the creditor may have previously extended an offer of settlement. You might either accept the offer or make a smaller counteroffer. Communicate why you can only afford the settlement amount you’re proposing, whether you’ve lost your job or are suffering from medical problems. Verify if the offer is for a particular monetary amount rather than a percentage of your balance to ensure everything is clear. If the creditor refuses to settle, you may wait until the debt is sold and then negotiate with the debt buyer or collection agency.

5. Review a written debt settlement agreement

A company representative could offer you a fantastic deal over the phone, but you need a formal offer on paper. Include your name, the name of the creditor or debt collector, and the account number on the proposal. Ensure that the letter specifies that your payment will fulfill your commitment. It may state that the account will be settled, paid in full, recognized as a complete settlement, or words to that effect. Keep a duplicate of the letter and any payment confirmations if a debt collector reaches you again. You may sometimes be required to negotiate a payment plan with your original creditor before receiving the settlement letter. Give the corporation several business days to deliver the letter to you in the interim while you attempt to negotiate a payment plan for the future. You may then cancel the payment if no note is received.

FAQs

Will my credit score go up after debt settlement?

Once you begin the debt settlement process, your credit score may initially drop, but it will gradually increase as you pay off your debts and handle your credit more responsibly. You can restore your credit score and improve your credit history.

Is it better to settle or pay in full?

You may pay in full if your account is current, past due, or in collections. Regarding debt repayment, it is preferable to pay in full rather than settle. When a debt is paid in full, it indicates that all payments have been made. It means to lenders that you can meet your financial obligations.

Can I get a loan after settlement?

Before considering granting a loan to a borrower, banks and lenders primarily evaluate his repayment history. And if the settlement appears on the borrower’s credit report, banks and lenders will reject the loan application.

Although the option of negotiating a resolution should drive everyone to try, there is a considerable probability you will hear “no” at some point. If so, you should not simply hang up the phone and leave. Instead, ask your credit card provider whether it may cut your annual percentage rate (APR) or monthly payment or offer an alternate payment plan. Often, the debt settlement agent for your credit card will feel guilty about rejecting your offer and may be prepared to agree to one of these alternative possibilities.