49+ Sample Facility Agreements

-

Working Capital Facility Agreement

download now -

Senior Short Term Facility Agreement

download now -

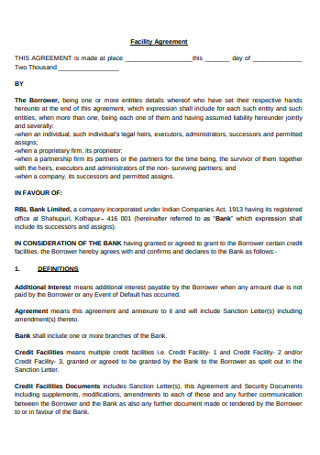

Sample Facility Agreement

download now -

Credit Facility Agreement

download now -

Water Facility Agreement

download now -

Share Facility Agreement

download now -

College Facility Agreement

download now -

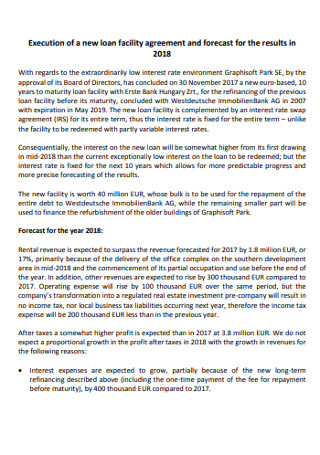

Loan Facility Agreement

download now -

School Facility Use Agreement

download now -

Ground Facility Use Agreement

download now -

Building Facility Use Agreement

download now -

Basic Credit Facility Agreement

download now -

Facility Granting Security Agreement

download now -

Provider Facility Agreement

download now -

University Facility Agreement

download now -

Master Financial Assistance Facility Agreement

download now -

Standard Facility Agreement

download now -

City Facility Use Agreement

download now -

Laboratory Facility Agreement

download now -

Room Facility Agreement

download now -

Stromwater Facility Agreement

download now -

Formal Facility Agreement

download now -

Sample Facilities Use Agreement

download now -

Restroom Facility Agreement

download now -

Basic Loan Facility Agreement

download now -

Parks Facility Agreement

download now -

General Facility Agreement

download now -

Facility Participation Agreement

download now -

Facility Lease Agreement

download now -

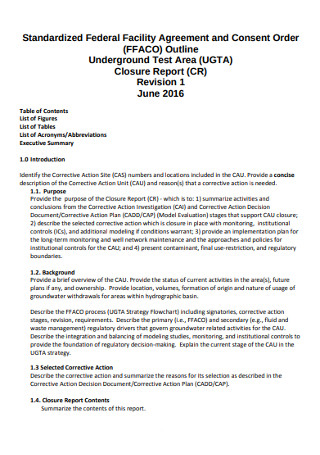

Standardised Federal Facility Agreement

download now -

Facility Quarterly Agreement

download now -

Facility Property Agreement

download now -

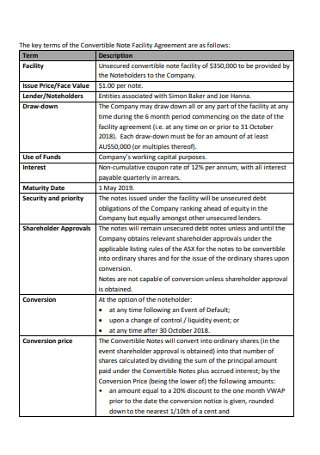

Convertible Note Facility Agreement

download now -

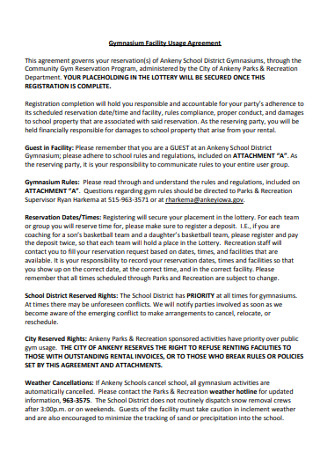

Gymnasium Facility Usage Agreement

download now -

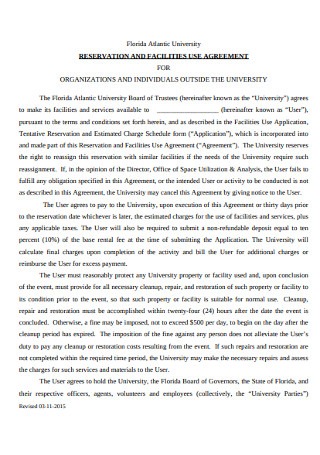

Reservation and Facilities Agreement

download now -

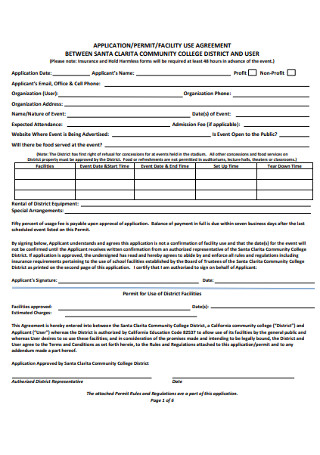

Sample College Facility Permit Agreement

download now -

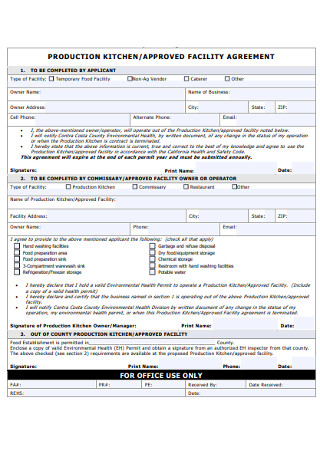

Production Kitchen Facility Agreement

download now -

Facility Policy Agreement

download now -

Facility Use License Agreement

download now -

Trade Finance Facility Agreement

download now -

Facility Rental Agreement

download now -

Procurement Facility Agreement

download now -

Mobile Retail Restroom Facility Agreement

download now -

Global Debt Facility Agreement

download now -

Agreement for Sharing of a Permitted Food Facility

download now -

Margin Facility Agreement

download now -

Amendment of Facility Agreement

download now -

Formal Facility Licence Agreement

download now -

Bank Facility Agreement

download now -

Litigation Facility Agreement

download now -

Standard Facility Agreement

download now

FREE Facility Agreement s to Download

49+ Sample Facility Agreements

What Is a Facility Agreement?

The Distinct Classifications of a Facility

How to Correctly Draft a Facility Agreement

FAQs

What is a credit facility?

What is a commitment fee?

How do you calculate a commitment fee?

What does a facility agent do?

What are the factors that determine a credit score?

What Is a Facility Agreement?

A business that needs money to continue its operation can apply for a “facility.” A facility is a solution that lending companies provide to companies that need financial help. It is a loan that a business takes out for its benefit. Most loan facilities don’t demand collaterals. Typically, the borrowing entity pays the principal amount and the interest on a monthly or quarterly basis until the whole debt is paid. For example, a boutique store that has low sales in the middle months of the year can apply for a $500,000 facility from a lending institution, which the store will pay back during the Christmas season.

The Distinct Classifications of a Facility

There are different classifications of facilities open for short-term or long-term borrowing entities. Here are some.

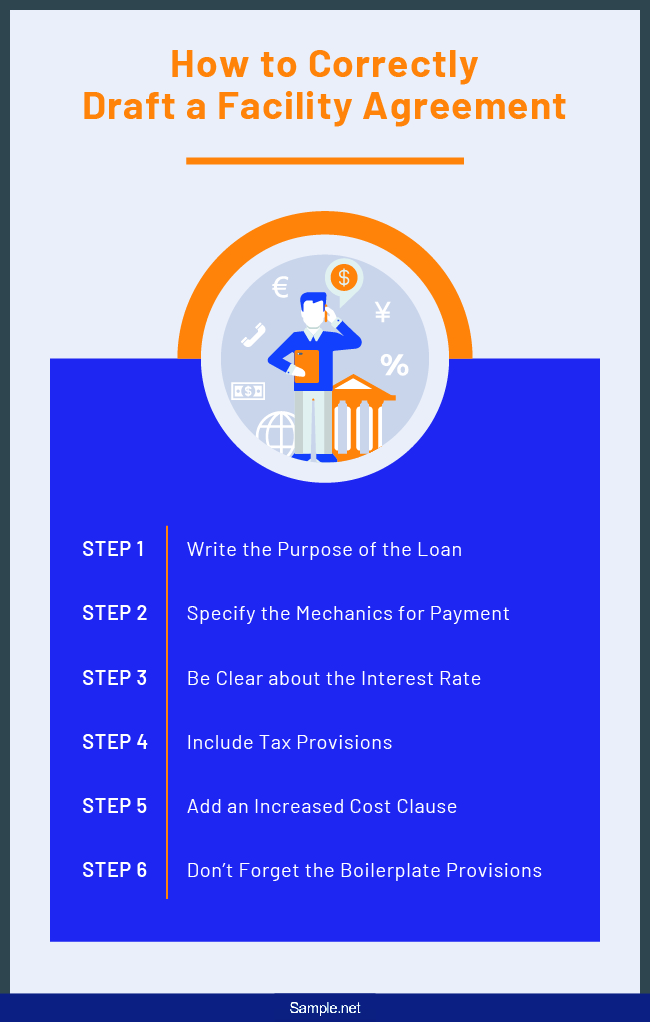

How to Correctly Draft a Facility Agreement

The contents of a facility contract may differ from one agreement to another. Nevertheless, common facility agreements will have the same substance and structure. Follow the steps below to create a facility agreement sample.

Step 1: Write the Purpose of the Loan

Facility agreements may contain a purpose clause that determines where the loan gets used. This is to ensure that the borrowing company will repay its debts and will not use it for illegal purposes. If the company uses the money for purposes that are not written in the contract, the lender may get the money back through a “Quistclose trusts” provision.

Step 2: Specify the Mechanics for Payment

Provide provisions in the agreement on how to settle payments. It may deal with the dates of repayment or prepayment, the limitations of prepayment, and the conditions regarding the availability of the loan facility. Advances happen when a borrower settles a loan before its due date.

Step 3: Be Clear about the Interest Rate

As mentioned earlier, an interest can be fixed or floating. A fixed interest rate is typical with short-term loans, while a floating interest rate is typical for long-term investments. Compared to floating rates, fixed rates can be higher. Some borrowers go for fixed interest rates when they are low. It is good to know that the Consumer Financial Protection Bureau prescribes interest rates in different locations. The CFPB is an agency that regulates the operations of financial institutions.

Step 4: Include Tax Provisions

This may include tax gross-up, credit, and indemnity. Tax gross-up is money paid by a borrower to cover up for withholding taxes that a lender pays. The tax credit is money subtracted from the taxes a taxpayer owes to the government. Tax indemnity protects the profit of a lender by passing all the tax burdens to a borrower.

Step 5: Add an Increased Cost Clause

In case a law changes after the signing of the agreement, having a clause that explains why the cost is increasing is vital. The primary purpose of this clause is for risk management on the lender’s part. This allows a lender to recover the money that is lost after complying with a new law.

Step 6: Don’t Forget the Boilerplate Provisions

An agreement may comprise of different boilerplate provisions. A critical requirement that one shouldn’t forget to include is the governing law. This clause decides what law to use to interpret the whole contract in case disputes arise later on. Also, identify the jurisdiction who will rule and make the final decision if conflicts do happen.

FAQs

What is a credit facility?

A credit facility is a loan that allows businesses or corporations to borrow money from a lending company for a long period instead of repeatedly reapplying for it. This type of agreement may include details concerning the borrower’s obligations, loan guarantees, interest rates, lending sum, nonpayment penalties, and repayment conditions.

What is a commitment fee?

A commitment fee is a fee a lender asks from a borrower for his/her lending service. It can be a flat fee or a percentage taken from the loan amount. This fee will guarantee a borrower that a lender will supply funds in the future regardless of the credit market conditions.

How do you calculate a commitment fee?

The borrower and lender can negotiate a commitment fee if it is only one-time. As mentioned earlier, it can be a flat fee (e.g., $1,500), or a fixed percentage from the total loan amount (e.g., 3%). According to Investopedia, the formula for calculating an open line of credit is by multiplying the average “unused” fee by the “agreed fee,” and multiply the result to the number of days.

What does a facility agent do?

A facility agent serves as a middleman between a borrower and a group of lenders who are part of a syndicated loan. A syndicated loan is financial assistance provided by different lenders to one borrower. The borrower can be the government or a corporation. This type of loan is for instances like major projects, where a large amount is necessary. A facility agent simply manages the interaction between the parties involved. Aside from that, he/she controls the flow of finances and deals with all transactions.

What are the factors that determine a credit score?

Three factors determine a credit score. The first is character. A lender may ask about your credit history. This may include issues concerning your use of credit, your ability to pay on time, your current address, your job, etc. The second is capital. A lender needs to know whether you have assets such as savings, investments, real estate, and personal property, which may serve as collateral. The third is capacity. This will determine your ability to pay your debt. The lender may ask questions about your salary, expenses, other debts, dependents, etc.

If you own a business or corporation, you can use facility agreements to your advantage. These agreements come in different forms, so you can choose whatever fits your needs. If you need to complete a major project plan, but you don’t have enough funds, you can always ask help from trustworthy lending companies. Note that the LaGuardia Airport wouldn’t be established without enough funding.