Commercial Loan Agreement

-

Commercial Loan Subsidy Agreement Template

download now -

Commercial Vehicle Loan Agreement

download now -

Commercial Loan Security Agreement

download now -

Commercial Enterprise Loan Agreement

download now -

Simple Commercial Loan Agreements Template

download now -

Formal Commercial Loan Agreement

download now -

Commercial Construction Equipment Loan Agreement

download now -

Commercial Term Loan Agreement

download now -

Commercial Business Loan Agreement

download now -

Standard Commercial Loan Agreement

download now -

Commercial Bridge Loan Agreement

download now -

Commercial Vehicle Loan Agreement Template

download now -

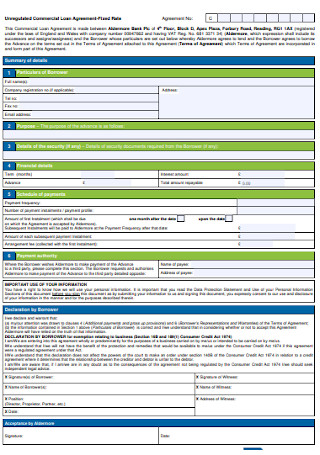

Commercial Fixed Rate Loan Agreement

download now -

Commercial Secured Loan Agreement

download now -

Commercial Credit Loan Agreement

download now -

Commercial Construction Loan Agreement

download now -

Commercial Master Securities Loan Agreement

download now -

Basic Commercial Loan Agreement

download now -

Commercial Funding Loan Agreement

download now -

Commercial Personal Loan Agreement

download now -

Commercial Bond Loan Agreement

download now -

Formal Commercial Loan Agreement Template

download now -

Sample Commercial Business Loan Agreement

download now -

Sample Commercial Business Financial Loan Agreement

download now -

Commercial Bank Loan Agreement

download now -

Commercial Borrower Loan Agreement

download now -

Commercial Loan Agreement Format

download now

FREE Commercial Loan Agreement s to Download

Commercial Loan Agreement

What Is a Commercial Loan Agreement?

What Are the Essential Sections of a Commercial Loan Agreement?

How Do You Process Your Commercial Loan Agreement?

FAQs

How can I qualify for a commercial loan?

Is it hard to get commercial loans?

What are the common types of commercial loans?

What Is a Commercial Loan Agreement?

In finance, loans refer to the money lending process between borrowers and lenders. Loaning is initiated by any person, group, or business and will be lent by another individual, bank, or any entity capable of being a lender. Why consider a loan contract, you may ask? This solution is applicable for dealing with debts since you have quick money to use. However, commercial entities will have to process for a commercial loan agreement form. Unlike the typical personal loan agreement, this type of arrangement is for business purposes alone. In other words, a commercial loan is a deal between businesses and banks or similar entities. Expect commercial loan agreements to work as your company equipment loan or coverage for operational fees. More so, the arrangement for commercial loan financing is debt-based, so it will have to get repaid with interest in the end.

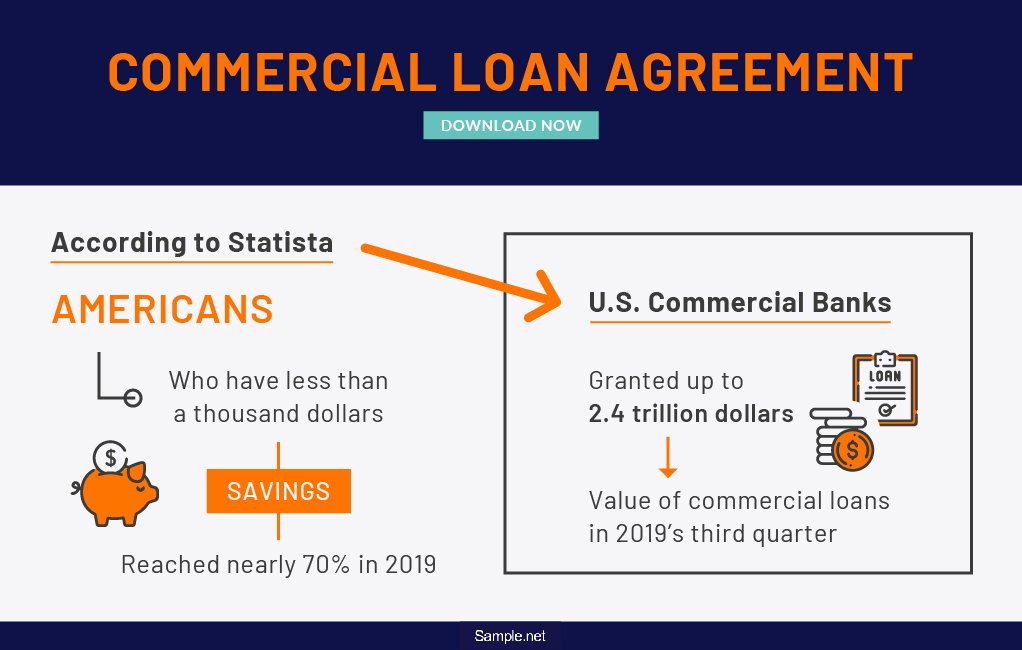

According to Statista, Americans who have less than a thousand dollars for savings reached nearly 70% in 2019.

Additionally, Statista stated that U.S. commercial banks have granted up to 2.4 trillion dollars in value of commercial loans in 2019’s third quarter.

Moreover, it has been estimated that 7.7 million business establishments in the U.S. have at least one employee back in 2016.

Commercial Loans: How It Works and Why It Is Important

Various industries depend on commercial loans, but how does it work? Commercial loaning will most likely require collateral from businesses. The collateral can be of any acceptable property or, perhaps, equipment that lenders will seize if borrowers cannot meet the conditions of the loan agreement letter. Such a requirement works as hypothecation wherein assets or properties are declared as collateral for securing loans. In avoiding losses of assets, like having those confiscated by the bank, businesses better prevent any default, bankruptcy, and related blunders. If only every borrower remains responsible for the money agreement between two parties, then no issue will commence.

In terms of importance, commercial loans play a pivotal role, typically in short-term business funding. For example, businesses may need replacements, repairs, or enhancements in the form of capital expenditures. Those funds deal with the maintenance of the physical assets of commercial entities. That way, business operations need not cease since a loan covers it for the meantime. Furthermore, different industries can also make use of commercial funding for processing a construction loan, vehicle financing along with an auto contract, or issuing mortgages to a commercial home loan. Thus, a lot can benefit from this tool. Nevertheless, it may not happen without proving how financially capable businesses are in paying afterward.

1947: The First-Ever Loan from the World Bank

The Business Journals reached an estimation of up to 7.7 million American business establishments with a single employee back in 2016. And some businesses have likely loaned at some point with their operations to last in the industry, too. Did you know that the World Bank granted the first loan on May 9, 1947? Moreover, June 25, 1946 marked as the opening day of the World Bank. Although, reconstruction loan preparations and services only began on February 23, 1947, which was during John J. McCloy’s turn as the Bank’s president.

France and other Western European countries applied for the loan. The first-ever loan application was in the form of a simple but detailed letter regarding the $500 million reconstruction plan of the government called the Monnet Plan. The message detailed that the finances will cover $214 million worth of raw materials, $180 million worth of coal or petroleum, and $106 million worth of ships, trucks, cars, and additional equipment. Because of this immense French loan, the World Bank became highly respected in terms of lending by that time. As time went by, more businesses apply for a loan until these days.

What Are the Essential Sections of a Commercial Loan Agreement?

If you will apply for a commercial loan, you need to sign a contract or agreement regarding the terms of arranging a commercial loan for the business. Also, the agreement form consists of certain parts, which cover several terms and conditions. To know about each component, here are the essential sections found in commercial loan agreements:

How Do You Process Your Commercial Loan Agreement?

Statista mentioned that commercial banks in the U.S. granted nearly 2.4 trillion dollars commercial loan value back in the third quarter of 2019. Imagine how many businesses benefited with that massive amount. Your business or company can take advantage of commercial loans, too, with the help of an agreement. Are you wondering how to write a loan agreement? Or perhaps, how to process your commercial loan properly? You will learn in due course with these essential steps:

Step 1: Be Sure with Your Decisions

Before processing or making a commercial loan agreement, you have to settle significant decisions. First, specify the type of loan in case you mix this up with an auto loan or any property loan. Also, is it a secured or unsecured loan? Next, identify the intended use of the loan. Lenders would naturally ask the purpose before deciding to lend money for assurance if the money is for commercial purposes or not. On the other hand, you decide ahead about the loan amount and collateral, as you need these prepared once the agreement ensues.

Step 2: Use the Appropriate Template and Edit

Download a commercial loan agreement template; there can be a bunch of choices up for grabs. With many options to choose from, you may get confused in selecting. A tip is to compare the pros and cons of each option until you derive your final choice. Make sure it is an appropriate template as well and not other agreement templates like the hold off agreement, car purchase, and other examples. Then, modify the template by adding the critical details asked.

Step 3: Fill in the Parties’ Details

One of the first things to check in general agreements or work contracts is the party information. In this section, lenders and borrowers need to be identified thoroughly. Maybe you have not stated which particular bank is responsible for lending you. Missing out any important detail is discouraged because you will still be asked further about whatever is lacking. More so, you need to check if the spelling and information given are correct.

Step 4: Finalize the Repayment Option and Payment Schedule

One cannot ignore how borrowers observe a repayment agreement with their lenders. It can get done in the form of fixed or on-demand repayment. In most cases, people who manage bigger investments or purchases can benefit from fixed repayment. Thus, on-demand repayments are highly suggested to smaller purchases and those who borrow for short-term purposes only. Moreover, the schedule in dealing with such payments require transparency. Every party must stay wary about when to expect payments. That way, expectations will be crystal clear on the payment amount and duration of repayment.

Step 5: Incorporate the Governing Law

The essential bits of stating the rules and laws are always part of an agreement. For example, things might not be clear yet on the cancellation policies, prohibitions, and other conditions. You may think that nobody would disobey the regulations, but maybe there is a point where that happens in particular circumstances. Failing to secure this part means that businesses who breach the agreement can easily get away with their mistakes. Therefore, the parties should respect what they promise to ensure fairness.

FAQs

How can I qualify for a commercial loan?

Expect a series of factors that will help you qualify for a commercial loan. These are the credit score, time in business, and annual revenue. By credit score, that means you must at least reach the passing mark because those who have lots of debts and poor credit will least likely receive approval. Meanwhile, your time in business matters; lenders trust those who have lasted long in the industry than new ones. Lastly, annual revenue is also important to check how much you earn and how capable you are for repayment.

Is it hard to get commercial loans?

It is quite easy, as stated in the steps above. However, it may be difficult when you disagree with certain parts of the agreement or when you do not qualify to loan at all. Make sure to review the agreement and maintain good credit if you wish to proceed.

What are the common types of commercial loans?

The common types of commercial loans are permanent loan, bridge loan, takeout loan, construction loan, conduit loan, SBA 504 loan, SBA 7a loan, hypothecation, and more. You need to recognize what makes each example different so that you can use the correct type and experience its benefits.

Costly capital expenditures and other business operations requiring instant money would benefit from a commercial loan. But the content of the agreement is not something you can just overlook. Financial responsibilities and important obligations also come to play. Furthermore, failing to adhere to everything incorporated in the agreement would lead to consequences, such as losing your collateral or undergoing court processes. Indeed, you can look forward to the release of the loan, but receiving that means you also have to give back through the installment arrangement agreed in the document. Consequently, you should come up with a strategic plan to repay the loan before signing the commercial loan agreement.