Land Sale Agreement Samples

-

Agriculture Land Sale Agreement

download now -

Private Land Sale Agreement

download now -

Promotional Land Sale Agreement

download now -

Vacant Land Sale Agreement

download now -

Land Purchase and Sale Agreement Template

download now -

Agreement of Sale of Land

download now -

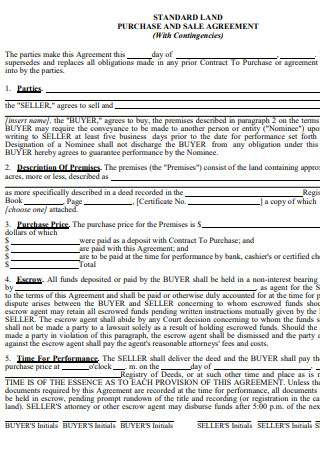

Standard Land Purchase and Sale Agreement

download now -

Land Sales Agreement Template

download now -

Land Purchase And Sale Agreement

download now -

Agreement for Sale of Property

download now -

Generic Land Sale Agreement

download now -

Specimen Agreement of Sale of House Property

download now -

Land Sales Agreement Format

download now -

Land Sale Contract Form

download now -

Purchase and Sale Agreement Surplus Property

download now -

Lot/Land Purchase and Sale Agreement

download now

FREE Land Sale Agreement s to Download

Land Sale Agreement Format

Land Sale Agreement Samples

What is a Land Sale Agreement?

Types of Land Sale Agreements

How to Create a Land Sale Agreement

FAQs

What are the drawbacks of signing a land contract?

Is it necessary to hire an attorney to analyze a land contract?

What are the drawbacks of land contracts?

What are common contingencies in a Land Sale Agreement?

What happens if the seller breaches the agreement?

What role does escrow play in a Land Sale Agreement?

What are the tax implications of a Land Sale Agreement?

How can the buyer ensure a clear title in the Land Sale Agreement?

What should sellers disclose in the agreement?

Download Land Sale Agreement Bundle

Land Sale Agreement Format

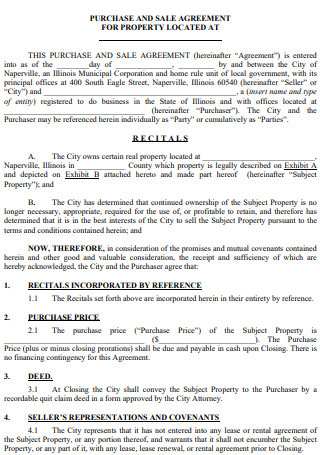

This Land Sale Agreement (“Agreement”) is made on this [Date] by and between:

Seller:

Name: [Full Name]

Address: [Complete Address]

Phone: [Phone Number]

Email: [Email Address]

Buyer:

Name: [Full Name]

Address: [Complete Address]

Phone: [Phone Number]

Email: [Email Address]

The Seller and Buyer may individually be referred to as a “Party” or collectively as the “Parties.”

1. Subject of Agreement

The Seller agrees to sell, and the Buyer agrees to purchase, a parcel of land located at:

[Property Address],

[City], [State], [Zip Code], [Country].

- Plot/Survey Number: [Plot/Survey Number]

- Total Land Area: [Total Area in square feet/meters]

2. Purchase Price and Payment Terms

- Total Purchase Price: [Total Amount in Currency]

- Deposit Amount: [Deposit Amount in Currency] (to be paid upon signing this Agreement)

- Balance Amount: [Remaining Amount in Currency] (to be paid upon completion of all legal formalities)

All payments must be made by [mode of payment] and completed within [time frame] from the date of this Agreement.

3. Possession and Transfer of Title

- The Seller will deliver physical possession of the land to the Buyer upon receipt of the full payment.

- The title to the land will be transferred to the Buyer through a legally valid document (e.g., a deed), duly executed and registered under the applicable law.

4. Representations and Warranties

- The Seller warrants that they have clear and marketable title to the land, free from any encumbrances, liens, or legal disputes.

- The Buyer warrants that they have the legal capacity to enter into this Agreement and fulfill the payment obligations.

5. Taxes, Fees, and Other Charges

- The Seller shall bear any pending property taxes, if any, up to the date of transfer of the title.

- The Buyer shall bear the stamp duty, registration fees, and other legal expenses related to the registration of this Agreement.

6. Termination and Cancellation

- In the event of breach by either Party, the non-defaulting Party reserves the right to terminate this Agreement by giving written notice to the defaulting Party.

- The Buyer may cancel the Agreement before the transfer of title; in such cases, the deposit will be forfeited unless mutually agreed upon otherwise.

7. Dispute Resolution

- Any disputes arising from this Agreement shall be resolved through negotiation between the Parties.

- If no amicable resolution is reached, the dispute shall be referred to arbitration, as per the [applicable law] of [country/state].

8. Miscellaneous

- This Agreement shall be governed by the laws of [State/Country].

- This Agreement constitutes the entire understanding between the Parties and supersedes all prior discussions and agreements.

Signatures

IN WITNESS WHEREOF, the Parties have executed this Land Sale Agreement as of the date first above written.

Seller’s Signature: ____________________

Name: [Full Name]

Date: [Date]

Buyer’s Signature: ____________________

Name: [Full Name]

Date: [Date]

Witness 1: ____________________

Name: [Full Name]

Address: [Complete Address]

Witness 2: ____________________

Name: [Full Name]

Address: [Complete Address]

What is a Land Sale Agreement?

A Land Sale Agreement is a formal contract that establishes the legal framework for the sale and purchase of land, specifying the obligations, rights, and responsibilities of both parties involved in the transaction. You can also see more on Sale and Purchase Agreements.

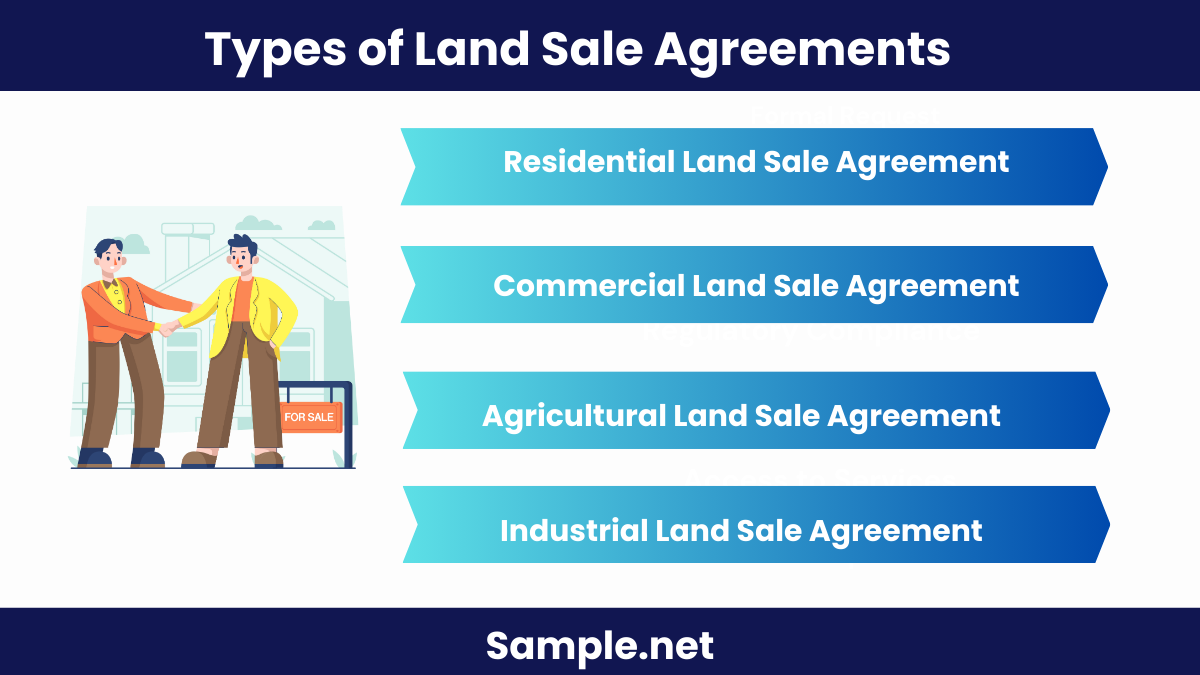

Types of Land Sale Agreements

1. Residential Land Sale Agreement:

This agreement is specifically designed for transactions involving plots meant for constructing residential buildings or developments, such as single-family homes, apartments, or gated communities. It includes clauses that focus on residential zoning regulations, utility access, environmental considerations, and local building codes to ensure that the land can legally support residential development. Additionally, it often outlines requirements for residential infrastructure like sewage, water supply, and road access. You can also see more on Sales Agreements.

2. Commercial Land Sale Agreement:

This type of agreement is tailored for the sale of land intended for business use, including offices, shopping centers, hotels, and other commercial establishments. It covers aspects like commercial zoning laws, potential commercial usage restrictions, and compliance with business development permits. Moreover, the agreement specifies terms regarding existing structures on the land, utility availability, and modifications required to transform the land for commercial use, making it suitable for revenue-generating activities.

3. Agricultural Land Sale Agreement:

This agreement is crafted for land sales dedicated to farming, ranching, and other agricultural activities. It includes specific clauses related to soil quality, water rights, irrigation access, and land-use restrictions to ensure compatibility with farming needs. Additionally, the agreement may outline allowances for livestock facilities, cultivation equipment, crop types, and agricultural subsidies or grants, making it a comprehensive guide for transactions within the agricultural sector.

4. Industrial Land Sale Agreement:

Designed for transactions involving land meant for industrial development, this agreement addresses key considerations like factory setups, manufacturing plants, storage facilities, or warehouses. It includes terms regarding heavy machinery installation, environmental compliance (e.g., waste disposal), zoning permits, and access to transportation networks such as railways, highways, or ports. The agreement ensures that the land is suitable for industrial-scale operations while covering aspects like safety regulations, utility requirements, and potential expansions. You can also see more on Real Estate Purchase Agreements.

How to Create a Land Sale Agreement

1. Identify the Parties Involved

Include the full names, contact information, and roles of the buyer and seller. This ensures clarity regarding who is responsible for the terms laid out in the agreement.

2. Describe the Property in Detail

Provide a clear description of the land, including its address, size, plot number, and any legal identifiers. Attach property plans or documents to ensure accurate information. You can also see more on Purchase Agreements.

3. Establish Payment Terms and Conditions

Clearly state the purchase price, deposit amount, payment method, and due dates. Include clauses for late payments or penalties to avoid future disputes.

4. Outline Seller’s Disclosures and Buyer’s Rights

The seller should disclose any known issues, such as zoning restrictions or liens. Grant the buyer the right to conduct inspections and appraisals before closing.

5. Include Legal Clauses and Signatures

Add clauses related to dispute resolution, governing laws, and any special terms agreed upon. Obtain signatures from both parties, witnessed by a notary or legal representative. You can also see more on Property Sale Agreement.

A Land Sale Agreement serves as a crucial tool for ensuring a transparent and legally compliant transaction when selling land. It safeguards the interests of both buyers and sellers, detailing all terms, rights, and obligations clearly. Creating a well-drafted agreement minimizes the risk of disputes and provides a reliable reference for a smooth property transfer. You can also see more on Real Estate Contracts.

FAQs

What are the drawbacks of signing a land contract?

Land contracts have some disadvantages, so buyers beware. A land contract is not a viable alternative if holding title is crucial to a buyer; the title does not instantly pass to the buyer in a land contract sale. Land contracts do not prohibit mortgages.

Is it necessary to hire an attorney to analyze a land contract?

Yes. For those looking to acquire or sell specific types of real estate, land contracts may be the best, or in some cases, the only option. Because real estate laws differ from state to state, you must use a local lawyer to design a land contract that includes terms and conditions that will allow you to take action to defend your interest if necessary. You can also see more on Property Agreements.

What are the drawbacks of land contracts?

Regardless of how much money you invest into the property, the seller keeps ownership until you pay in full. If you fail to make any payments, the seller has the right to terminate the contract immediately and keep every penny you’ve paid (state laws vary on how this goes down).

What are common contingencies in a Land Sale Agreement?

Contingencies often include financing approval, title verification, and property inspection. These conditions must be met for the sale to proceed. If not, either party can withdraw without penalty. You can also see more on Buy and Sell Contract.

What happens if the seller breaches the agreement?

If the seller breaches the contract, the buyer can seek remedies like specific performance, damages, or contract termination. Legal action depends on the severity of the breach and the terms of the agreement.

What role does escrow play in a Land Sale Agreement?

Escrow acts as a neutral third party that holds funds until conditions are met. It ensures a secure transaction, releasing money only when both parties fulfill their obligations. This minimizes risks for both buyer and seller.

What are the tax implications of a Land Sale Agreement?

Taxes depend on local laws, the sale price, and whether it’s classified as capital gains or income. Buyers may pay property transfer taxes, while sellers may incur capital gains tax. Consulting a tax professional is advisable.

How can the buyer ensure a clear title in the Land Sale Agreement?

Buyers should conduct a thorough title search before signing the agreement. This verifies that the land is free from liens or claims. The agreement can also include a clear title guarantee from the seller. You can also see more on Land Lease Agreements.

What should sellers disclose in the agreement?

Sellers should disclose any encumbrances, zoning restrictions, liens, or environmental hazards. Full transparency protects both parties and prevents legal issues. Disclosures should be documented within the agreement.