8+ Sample Co-operative Business Plan

-

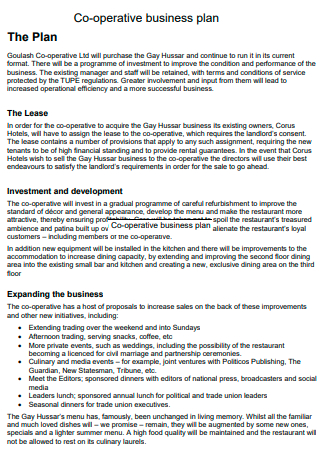

Co-operative Business Plan Template

download now -

Basic Co-operative Business Plan

download now -

Co-operative Business Plan Outline

download now -

Power Co-operative Business Plan

download now -

Food Co-operative Business Plan

download now -

Investment Co-operative Limited Business Plan

download now -

Co-operative Valley Business Plan

download now -

Co-operative Business Plan in PDF

download now -

Printable Co-operative Business Plan

download now

FREE Co-operative Business Plan s to Download

8+ Sample Co-operative Business Plan

a Co-operative Business?

Benefits of a Co-operative

Types of Co-operatives

How To Start a Co-operative Business Plan

FAQs

How do co-operatives generate revenue?

Who benefits from a co-operative’s profits?

What is the maximum number of owners that a co-operative can have?

What Is a Co-operative Business?

A cooperative is a business established by the consumers of its products or services. Cooperatives are distinguished from other types of companies by their emphasis on member benefit rather than shareholder profit. Cooperative enterprises can be as small as a neighborhood purchasing club. Individuals typically join a suitable business to take advantage of group purchasing, risk pooling, and the empowerment of owning and controlling the company. Co-ops are formed to provide competition, strengthen bargaining power, reduce business startup costs, expand new and existing market opportunities, and obtain previously unavailable products or services. Research shows around 3 million cooperatives worldwide, and approximately 12% of the world’s population is one member. Cooperatives employ about 10% of the world’s population or roughly 280 million people.

Benefits of a Co-operative

Unlike business ownership, which is based on a person’s percentage ownership, cooperative ownership is based on equity contribution or how much of the cooperative’s products or services a member purchases. This is the primary distinction between a joint venture and other organizational structures. Traditional corporations allocate one vote per share in terms of control, allowing investors to purchase as many shares as they wish to obtain a specified number of votes. Each cooperative member is entitled to one vote, ensuring that all members have equal voting benefits. All members are expected to join and share in the organization’s governance. As with any business structure, cooperatives have several advantages, including the following:

Types of Co-operatives

Simply put, their purpose defines cooperatives; their members purchase goods and services and provide them to the cooperative. For example, cooperative grocery members buy groceries from their cooperatives, whereas cooperative worker-members provide labor to their cooperatives. Occasionally, members contribute goods or services to the cooperative and buy them; for example, members of the arts and crafts cooperative can purchase supplies from the cooperative and contribute their artwork and labor to market their skills through a cooperative store. Cooperatives are involved in a wide range of industries, including the following:

Agricultural Cooperatives

An agricultural cooperative, alternatively referred to as a farmers’ co-op, is a cooperative in which farmers pool their resources in particular areas of activity. A broad classification of agricultural cooperatives differentiates between agricultural service cooperatives, which provide various services to their individually farming members, and agricultural production cooperatives, which pool production resources and farm cooperatively. Agricultural service cooperatives are classified into two types: supply cooperatives and marketing cooperatives. Supply cooperatives provide inputs for agricultural production to their members while farmers form marketing cooperatives to handle the transportation, packaging, distribution, and marketing of farm products. Farmers also heavily rely on credit cooperatives for working capital and capital investments.

Business Cooperatives

Businesses form business cooperatives to save money on supply and services. They range in size and type and include cooperatives of individual business proprietors, such as respective taxi-cab owners pooling their resources to provide dispatch services. While cooperatives of small businesses, such as retail pharmacies, hardware stores, or plant nurseries, pool their purchasing power and cooperatives that share real estate information.

Child care and preschool Cooperatives

Child care and preschool cooperatives attract parents because they provide high-quality, inexpensive child care and early education programs. Parent involvement enables parents to contribute their perspectives and personal information of their preschoolers’ out-of-home experiences and the opportunity to communicate with other mothers. Parents elect a board of directors who develop policies and recruit qualified staff to manage the business operation. The majority of contemporary preschool cooperatives offer enrichment activities for children for two to four hours every workday. Parent involvement improves the program’s quality and also helps to reduce operating costs. Because PPNS programs frequently need extensive parental involvement, they attract children who have one parent at home full-time. Cooperatives for child care provide high-quality care for children while their parents work. Although many parts of the programs are identical to PPNS programs, they often differ in three important ways: they provide full-day care, hire additional staff, and dramatically reduce parent engagement requirements.

Credit Union

A credit union is a consumer-owned, not-for-profit financial cooperative founded by consumers to promote savings and low-cost borrowing. Its members are united by a common link, such as shared employment or employer, affiliation with the same association or religious organization, or residence in the same community. On a one-member-one-vote basis, members elect a board of directors. Credit unions arose when banks were uninterested in the consumer sector, particularly in small deposits and loans often required by working-class people. Development of Communities Credit Unions is a cooperative financial institution founded in mostly low-income neighborhoods. They have a declared objective of neighborhood reinvestment and revitalization in addition to meeting consumer requirements. They finance the acquisition and renovation of houses and small businesses, both privately and collectively owned.

Housing Cooperatives

Housing cooperatives are one of the state’s main cooperative sectors. Housing cooperatives are corporations owned by members or shareholders who get housing services from the corporation. Each member has a share of the corporation, which entitles them to live in a housing unit. Typically, cooperatives are financed by a blanket mortgage covering the entire property. Numerous cooperatives have been formed to provide low- and moderate-income households with cheap housing and ownership options. Also, these cooperatives get governmental subsidies to maintain affordable carrying charges. These cooperatives often have modest share prices, and member households may not possess more than one share. To further ensure affordability and to discourage speculative resale, price restrictions on share sales are imposed.

Insurance Cooperatives

Insurance cooperatives are similar to retail cooperatives. However, they specialize in insurance services rather than consumer goods. The membership is made up of policyholders who elect the board of directors. Cooperative insurance companies operate by pooling and investing member premiums. The revenue produced is then utilized to offset the expenses of insurance provision. Because policyholders are also owners, any earnings are returned to customers in the form of dividends. Insurance cooperatives can provide members lower insurance prices and increased control.

Retail Cooperatives

Cooperative retail stores supply consumer items to both members and non-members. On the other hand, members receive discounts, patronage refunds, or a combination of the two. Patronage refunds are calculated as a percentage of the total amount of money spent on purchases by a member over a given period. The cooperatives’ earnings fund these refunds. Additionally, retail cooperatives provide control. Because members elect representatives to the board of directors and have the right to vote at general membership meetings, consumers control the cooperative’s administration and policy.

Student Cooperatives

Students form and administer student cooperatives to address specific needs. The most frequent types of student cooperatives are housing and food cooperatives. Additionally, child care cooperatives and bookstores exist. Through the one-member-one-vote premise, student cooperatives are democratically administered. Although most members are students, the board may also include alumni, university officials, and other non-student members. Student cooperatives give significant additional benefits, besides cost savings on necessities such as accommodation and food. Students can take part in cooperative management and develop crucial commercial and organizational skills. Students can obtain beneficial experience living with people from diverse cultural and social backgrounds in cooperative housing.

Utility Cooperatives

Utility cooperatives supply their members with utilities such as communication, energy, and water. Cable television cooperatives are pretty similar to utility cooperatives in their organizational structure. Members share in the costs of startup and capitalization. In exchange, they profit from the reduced charges associated with users who are also owners. Telephone cooperatives, which serve more than a million members nationwide, also play a significant role in rural areas.

Worker Cooperatives

A worker cooperative is a market in which the employees control the majority of the stock. The cooperative structure enables everyday people to pool their energy, capital, and abilities to secure stable employment and income, participate in their enterprise’s ownership and management, and share in their investment and labor profits. Workers are involved in decisions that affect them at work and those that affect their growth and profitability. Worker cooperatives give jobs and income to their members while also providing them with ownership and management. Workers-members gain a fair share of earnings and control over how their job is planned, performed, and managed due to their right and authority.

How To Start a Co-operative Business Plan

When establishing a cooperative, it is critical to have a broad perspective. The following are the fundamental steps that will assist you in developing a realistic understanding of what it takes to start a cooperative and how to keep the development process running smoothly.

Step 1: Form a steering group.

You must assemble a group of individuals who represent the cooperative’s prospective members. Determine your mission and fundamental principles. Also, create a strategy and timeframe for conducting research status reports and building the organization. Co-ordinate a meeting of prospective members to gauge interest in the co-op concept.

Step 2: Conduct a feasibility analysis.

Examine significant possibilities and impediments that could make or break the organization’s formation. Consider the common challenges such as market conditions, operating costs, and funding availability. Local or state authorities may provide financial and technical assistance to perform a feasibility study in specific instances.

Step 3: Develop a business plan and increase membership.

Create a thorough business plan that will serve as a roadmap for the organization’s development and beginning operations and supporting documents for members, financial institutions, and investors. A typical business plan has an executive summary, a description of the firm, a market study, product research and development, a sales plan and sales strategy, organizational structure, and financial analysis.

Step 4: Obtain funding.

Whatever your cooperative’s mission and members are, it will certainly require funding to operate and develop. This influx of funds might originate from a variety of sources. Members frequently invest part of their own money. Numerous cooperatives seek business loans, while others may qualify for start-up assistance. The capital investment required to get started varies. The business plan should mention the quantity and type of money the co-op requires and the methods for obtaining it.

Step 5: Launch

Establish an office and, if necessary, hire staff. Then open the doors and begin responding to member demands with goods and services. You should have a successful business at this point.

FAQs

How do co-operatives generate revenue?

Historically, cooperatives have made investment very simple for members. When members join an established cooperative, they may be asked to make a small initial investment and then agree to make more investments over time by allowing the cooperative to hold or retain a share of its revenues each year as equity capital.

Who benefits from a co-operative’s profits?

While shareholders own the business itself in a for-profit cooperative, their primary financial interest is in the stock they possess. Shares entitle the bearer to a percentage of the corporation’s profits, which the corporation distributes in the form of stock dividends.

What is the maximum number of owners that a co-operative can have?

A cooperative is a corporate structure owned by its members, each with equal voting rights regardless of activity or investment. Each member is expected to commit to the cooperative’s operation.

A co-operative is an adaptable business model for new ventures. It may be established by employees, consumers, neighborhood residents, or groups. There are numerous models for this process, and you should investigate your alternatives to see which one best meets the objectives of your group. Uncertain whether this is the best business model for your organization? For additional information on the best business structure alternatives for small firms, consult our guide.