23+ Sample Economic Action Plan

-

Economic Development Strategy and Action Plan

download now -

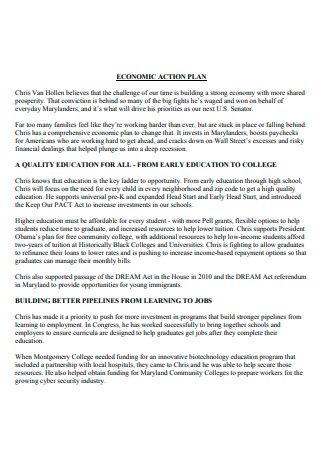

Economic Action Plan Example

download now -

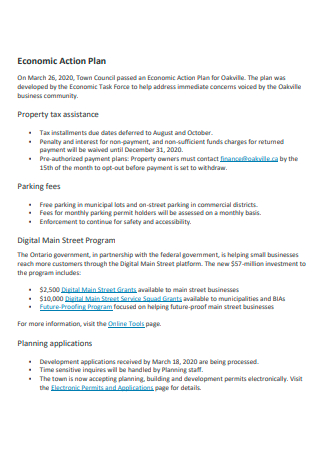

Economic Development Action Plan

download now -

Basic Economic Action Plan

download now -

Rural Economic Action Plan

download now -

Economic Prosperity Action Plan

download now -

Printable Economic Action Plan

download now -

Socio Economic Action Plan

download now -

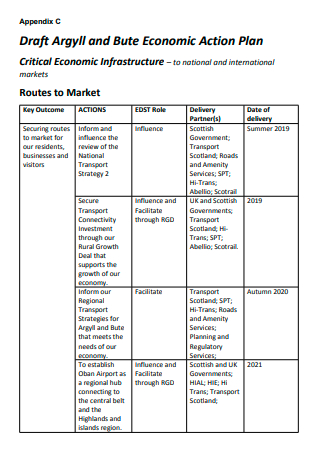

Draft Economic Action Plan

download now -

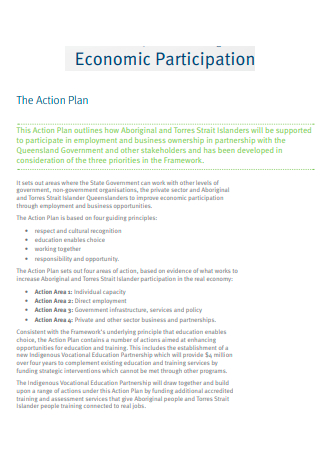

Economic Participation Action Plan

download now -

Economic Action Plan in PDF

download now -

National Park Economic Action Plan

download now -

Formal Economic Action Plan

download now -

Economic Region Action Plan

download now -

Economic Action Plan Format

download now -

Economic Development Commission Action Plan

download now -

Economic Action Plan Report Card

download now -

Economic Stimulus Action Plan

download now -

Rural Economic Action Plan Grant

download now -

Economic Growth Action Plan

download now -

Simple Economic Action Plan

download now -

Standard Economic Action Plan

download now -

Economic Recovery Action Plan

download now -

Economic Action Plan in DOC

download now

FREE Economic Action Plan s to Download

23+ Sample Economic Action Plan

What Is an Economic Action Plan?

Tips For Composing an Economic Action Plan

Sample Ideas For Economic Action Plans

How to Create an Economic Action Plan

What is an economic action plan?

How do I make an economic plan?

What are examples of economic strategies?

What Is an Economic Action Plan?

An economic action plan is a comprehensive plan that targets economic policy or reform. Its aim is to boost economic activity by outlining strategies and plans that address various concerns such as livelihood, infrastructure, trade, commerce, etc.

According to an online article by Investopedia, the United States and China top the list of the World’s Top 25 Economies. The economy of the United States is the largest based on its nominal GDP measurement amounting to $21.43 trillion.

Tips For Composing an Economic Action Plan

Whether a nation is considered a developed country or a developing country, economic policies may be similar or can vary from state to state. The political landscape of a country may also be an important contributing factor in the determination of an economic model. In other words, a democratic country may hold different positions and plans compared to communist nations when it comes to their economic framework. Even if countries differ in approach and belief, there are some basic ideals that can contribute to a truly sustainable economic action plan.

Sample Ideas For Economic Action Plans

A country’s economy is a broad and vast topic that requires careful planning and execution. Countries may have similar principles but differ in policies and procedures. The following are several sample economic plans and strategies that can be discussed deeper and further explored.

How to Create an Economic Action Plan

Crafting an economic action plan is no easy task. It can take multiple sitdown sessions and consultative meetings to finalize an agenda and actually write each section down. The format and structure of the action plan may vary depending on the needs of the committee, but there are simple steps on creating a basic and straightforward economic policy plan. Follow the guide below to get started.

-

Step 1: Establish the Objectives

The first step is determining what your objectives are for creating such an action plan. What are your goals that you wish to achieve with the creation of your economic action plan? To do this, you need to have a good grasp of the values and principles that you uphold. This will set the tone of the economic framework you and your co-authors will adopt. For instance, if you value fairness and equity, your objectives might revolve around inclusive employment and accessible livelihood. Or if your values are aligned with environmental conservation and preservation, your economic policies and procedures will not support anything that stands in contrast to your principles. Knowing where you stand and what your boundaries are vital factors when setting objectives and establishing goals.

-

Step 2: Identify the Stakeholders

The economy concerns all people and is meant to encompass everyone in a functional society. So it is only reasonable to identify and involve all stakeholders in the Planning Process. Of course, the democratic way of achieving this would be to hold multiple consultations and meetings. But the main point of doing such is to get everyone’s input, no matter how miniscule. It can be a long and tedious process but it is a necessary one. There is too much at stake for just one group of people to determine the economic course of a society or country. Representation matters and it is important for all stakeholders- communities, business groups, advocacy groups, etc.- to be heard and be allowed to participate in the process.

-

Step 3: Develop a Framework

Economics is a broad and complex discipline in which there can be several ways to interpret certain theories and economic practices. For an economic action plan to take form, there should at least be a sense of structure for it to make sense or for there to be a Basic Argument. Developing a framework or lens through which you view policy and make decisions is a necessary step in coming up with a comprehensive and compelling action plan. There are several existing economic models that you can consult and subscribe to; but the important thing to remember is that these serve as a basis for building your arguments. And like any action plan, you want to build strong arguments for your case.

-

Step 4: Prepare Tools To Track Progress

A sound economic action plan is not all about persuasive arguments and educational information. There must be hard data and statistics to back your claims as well. You can incorporate relevant graphs, charts and timelines into your action plan. Having these may also help convey your plans and strategies better. In addition to figures and numbers, you also need to put in place a monitoring strategy to track the progress and development of your action plan. Having these tools in your economic action plan can help you craft a much more detailed execution plan.

FAQs

What is an economic action plan?

An economic action plan is a comprehensive and detailed plan that aims to boost economic activity and investment, fuel trade and commerce and also address economic issues such as unemployment, inflation, etc.

How do I make an economic plan?

To craft an economic plan, you need to lay out your objectives, identify the stakeholders involved, use a framework that enables you to craft economic policy, then prepare the necessary tools and data to support your framework or strategies.

What are examples of economic strategies?

There are many examples of economic strategies; one only needs the right determination, will and innovation to implement them. Some of these examples could be training communities in new and rising industries, encouraging citizens to be entrepreneurial, or offering federal loans to put up small businesses, etc.

Economic development is a major concern of any modern and functioning society. The more important thing to consider is whether or not economic policies can benefit everyone in society, not just one or a few groups. And it essentially boils down to crafting an economic action plan based on strong values and moral principles. Browse the sample action plans above to get started on your own today!