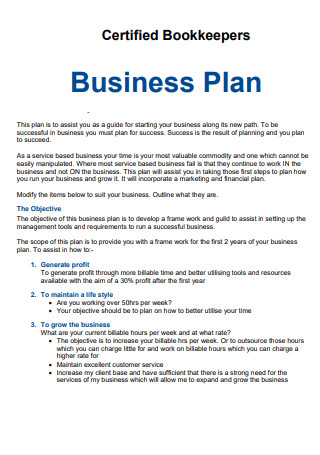

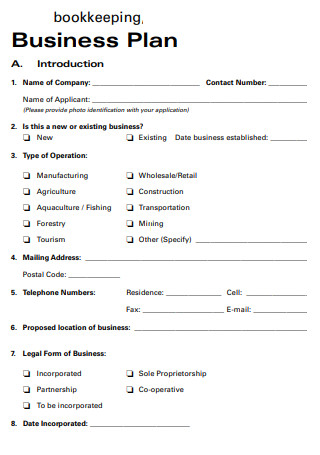

10+ SAMPLE Bookkeeping Business Plan

-

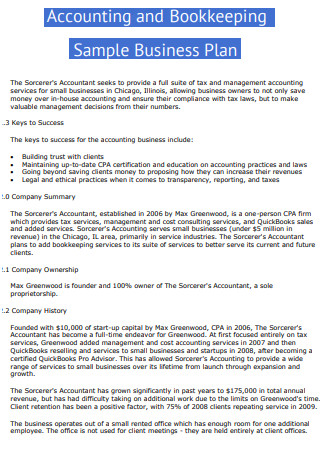

Accounting and Bookkeeping Business Plan

download now -

Basic Bookkeeping Business Plan

download now -

Company Bookkeeping Business Plan

download now -

Comprehensive Bookkeeping Business Plan

download now -

Detailed Bookkeeping Business Plan

download now -

Lengthy Bookkeeping Business Plan

download now -

Practical Bookkeeping Business Plan

download now -

Bookkeeping Business Plan Template

download now -

Bookkeeping Business Plan Example

download now -

Sample Accounting Bookkeeping Business Plan

download now -

Standard Bookkeeping Business Plan

download now

FREE Bookkeeping Business Plan s to Download

10+ SAMPLE Bookkeeping Business Plan

What Is a Bookkeeping Business Plan?

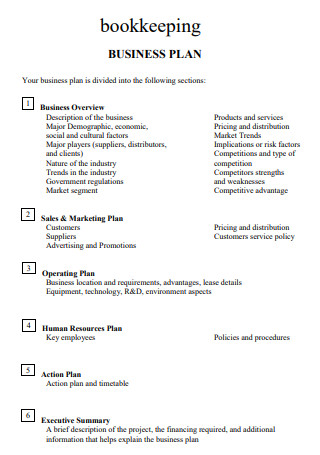

Elements Of a Bookkeeping Business Plan

Basic Types Of Bookkeeping

Step by Step Process in Bookkeeping

FAQs

What is a virtual bookkeeping system?

What is a business roadmap?

Why is a business plan needed for a bookkeeping business?

What Is a Bookkeeping Business Plan?

Before we get to the details of a bookkeeping business plan, we should know the basics first, starting with the definition of bookkeeping. Bookkeeping is defined as the process of recording your company’s financial transactions into organized accounts on a daily basis. It provides information to conduct accounting tasks and helps interpret the accounting information for decision-making by internal and external users.

A bookkeeping business plan refers to a business document that provides a small snapshot of where your bookkeeping business currently stands and it also lays out a visible growth plan for the foreseeable future. This document also explains the goals of your bookkeeping business and the strategy needed to reach them. It also includes market research to provide further support to your plans.

Elements Of a Bookkeeping Business Plan

Here are some of the elements you need to consider and include whenever you create your bookkeeping business plan:

Basic Types Of Bookkeeping

Here are some of the basic types of bookkeeping you may not know about:

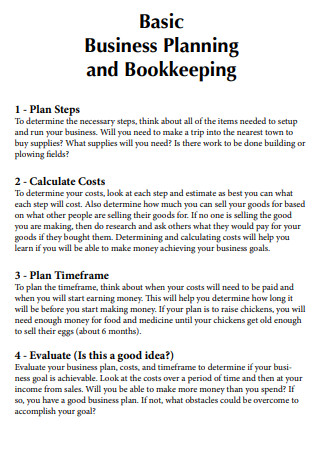

Step by Step Process in Bookkeeping

Here are the steps to be taken to keep things in order when doing the bookkeeping for a business:

-

1. Preparing the Source Documents

Prepare source documents for all transactions, operations, and other business events in this step; source documents serve as the starting point for the bookkeeping process. Purchase invoices, promissory notes payable, credit card slips, and salary rosters are examples of source documents. All of these key business forms are sources of information in the bookkeeping system, which the bookkeeper uses to record the financial effects of the business’s activities.

-

2. Determine and Record the Financial Effects of Transactions and Other Business Events

Transactions have financial consequences that must be recorded — the business is better off, worse off, or “different off” as a result of its transactions. Paying employees, making sales to customers, borrowing money from the bank, and purchasing products to sell to customers are all examples of typical business transactions. The bookkeeping process starts with determining the pertinent information about each transaction. The rules and methods for measuring the financial effects of transactions are established by the company’s chief accountant. Of course, the bookkeeper must follow these rules and procedures.

-

3. Create Entries of the Effects Into Journals and Accounts

The bookkeeper makes the first, or original, entry into a journal and then into the business’s accounts, using the source document or documents for each transaction. In recording transactions, only the official, established chart of accounts should be used. It is critical to enter transaction data correctly and in a timely manner. The prevalence of data entry errors was one of the primary reasons that most retailers began to use cash registers that read barcode information on products, which more accurately captures the necessary information and speeds up data entry.

-

4. Perform the Necessary End-Of-Period Procedures

A period is defined as a time span ranging from one day to one month to one quarter (three months) to one year that is determined by the needs of the business. A year is the longest time a company would wait to prepare its financial statements. Accounting reports and financial statements are required by most businesses at the end of each quarter, and many require monthly financial statements.

-

5. Compile an Adjusted Trial Balance

After completing all end-of-period procedures, the bookkeeper compiles a complete listing of all accounts, known as the adjusted trial balance. Small businesses keep hundreds of accounts for their various assets, liabilities, equity, revenue, and expenses. The accountant uses the adjusted trial balance to group similar accounts into a single sum that is reported in a financial report or tax return. The accountant should group the accounts in accordance with established financial reporting standards and income tax requirements.

-

6. Close the Books

The term “books” refers to a company’s entire set of accounts. Transactions in a business are a constant stream of activities that do not end neatly on the last day of the year, which can make preparing financial statements and tax returns difficult. The company must draw a clear line between activities for the previous year (the 12-month accounting period) and those for the coming year by closing the books for one year and beginning with fresh books for the next.

FAQs

What is a virtual bookkeeping system?

A virtual bookkeeper is an online agent who manages your financial records. Virtual bookkeeping services are popular among those who consider both single-entry and double-entry accounting systems to be complex and difficult to manage. Because of the cost savings, a virtual bookkeeper is a great alternative to an in-house bookkeeper or accountant; they cost a fraction of what an on-site employee would cost a small business, but they’re just as effective.

What is a business roadmap?

A business roadmap is a visual representation of your company’s major goals and strategies. Business roadmaps are used by stakeholders to illustrate initiatives and deadlines occurring in various departments. A roadmap, like a business plan, provides a long-term view of where your organization is going and how it will get there. Stakeholders must share a common understanding of the big picture for businesses to succeed. Business roadmaps break down team silos and provide a clear vision of the future.

Why is a business plan needed for a bookkeeping business?

A business plan is needed for a bookkeeping business because it will help you raise funding, if needed, and plan out the growth of your bookkeeping business in order to improve your chances of success. Your bookkeeping business plan is a living document that should be updated annually as your company grows and changes.

The business of bookkeeping can prove to be a big mountain to climb for new accountants because there are too many things for them to remember and organize. There are also far too many documents that they need to review, store, and organize frequently. To make matters a bit easier for them, they can put together a business plan for their startup business in order to make it a worthwhile endeavor for them. This makes the new accountants have a deeper understanding of the bookkeeping business, lets them get acquainted with their competition, and lets them have a greater knowledge of who their customers are. In this article, examples of an effective bookkeeping business plan are available for you to download and use as a personal reference.