24+ Sample Risk Action Plan

-

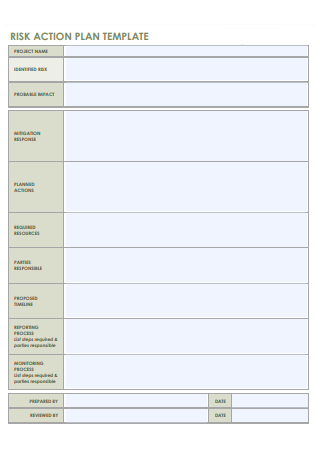

Risk Action Plan Template

download now -

Risk Management Strategy and Action Plan

download now -

Risk Improvement Action Plan

download now -

High Risk List Action Plan

download now -

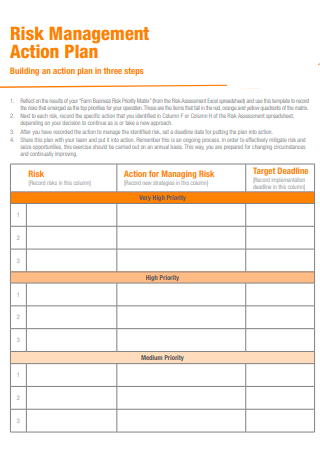

Risk Management Action Plan

download now -

Risk Action Plan Example

download now -

Risk And Treatment Action Plan

download now -

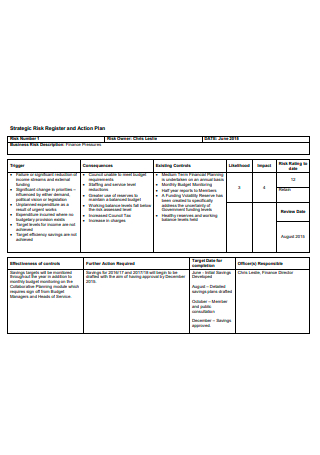

Strategic Risk Register and Action Plan

download now -

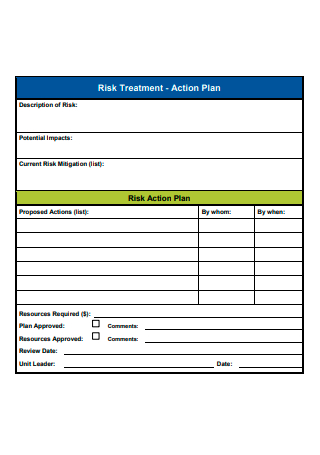

Risk Treatment Action Plan

download now -

Stress Risk Assessment and Action Plan

download now -

Risk Management Framework Action Plan

download now -

Investor Network on Climate Risk Action Plan

download now -

Risk Education Action Plan

download now -

Formal Risk Action Plan

download now -

Standard Risk Action Plan

download now -

Local Flood Risk Management Strategy Action Plan

download now -

Strategic Risk Register Action Plan

download now -

Risk Management Policy and Action Plan

download now -

Duty Risk Assessment Action Plan

download now -

Corporation Risk Action Plan

download now -

Team Stress Risk Assessment Action Plan

download now -

Re-opening Risk Assessment and Action Plan

download now -

Care Risk Assessment and Action Plan

download now -

Disaster Risk Reduction Action Plan

download now -

Risk Treatment Action Plan Form

download now

FREE Risk Action Plan s to Download

24+ Sample Risk Action Plan

What Is a Risk Action Plan?

Understanding How Critical a Risk Is

How to Write a Risk Action Plan

Distinguish between the Three Levels of Knowability

What Kinds of Business Risks Should You Prepare For?

FAQs

What are the many forms of risk management plans?

What is a risk action plan’s purpose?

Is a risk action plan the same as a risk management plan?

What Is a Risk Action Plan?

A risk Action Plan is a set of guidelines that a company commits to follow in order to handle possible risks, minimize the chance of them occurring, and mitigate the impact of these risks if they do. A plan is devised to guarantee that the appropriate steps are taken in a timely way. A plan also serves as a reference point in the event that something unanticipated happens. It prepares you to go on business by assisting you in developing contingency plans.

Understanding How Critical a Risk Is

An occurrence, a change in conditions, or their effects can all represent a risk. It is impossible to establish your objectives and devise tactics for attaining them without first recognizing risks. Integrating risk management into your Business Plan and planning out activities to address it is a recommended practice. Creating a risk action plan for your company is a step ahead from changing the outcome when encountering a risk against not having one at all, which may worsen situations and affect your employees.

How to Write a Risk Action Plan

Risks must first be recognized and analyzed before a risk action strategy can be developed. An organization must evaluate the likelihood of a risk occurring as well as the possible consequences to the company if that risk occurs while establishing a plan. If you are responsible for designing risk action plans, you must carefully examine whether the costs of preventing the risk from occurring are less than the costs of dealing with the risk if it does occur. If the cost of prevention is higher, you can either come up with a different plan or the company may decide to pursue other alternatives. Continue reading the steps to be guided on the different risk action plan components.

Step 1: Recognize possible risks

The first stage is to identify all of the possible threats to your project. This should happen at the start of the project and on a regular basis thereafter. Consider and identify which risk category it falls under and you should know the level of knowability the risk has. If you aren’t aware of the latter, the article provides you an explanation of the levels of knowability down below. Although there are different ways to identify risks and come up with a plan for them, you can also utilize the company’s resources to conduct interviews or even form a team for brainstorming sessions.

To conduct an assumption analysis, you would also need a risk Checklist, create one if your company doesn’t already have one and if it does, then it is high time to update it.

Step 2: Evaluate and appraise each possible risk

Before you should head straight into writing the risk you have identified to potentially be a challenge or a hazard to the company, you must first evaluate how the situation will unfold or how bad will the result be if the risk does transpire. This provides each of the context and relevance of your risk. You can comprehend just how dangerous they are and how much you should be planning ahead for them instead of simply hearing it as a simple statement. In this stage, you will assess the risk’s qualitative and quantitative effect before assigning a probability score as well as a risk effect score.

Step 3: Assign team members for a particular risk

It isn’t enough to jot down potential hazards and hope they don’t materialize. Each risk should be allocated to a member of the team, and these respective assigned team members should give their estimate of the resources required to address the potential risks. If the risk occurs and does become a real problem, the chosen team member will be responsible for taking accountability. As part of this, they must be aware of the risk triggers or warning signals that alert them to take action. In some situations, a risk trigger may be detected ahead of time, while in others, pinpointing the specific reason is nearly impossible. Risks should not be attributed to a single individual, but they should be apparent to everyone. This way, everyone knows what to look out for and who to call if one of the triggers is spotted.

Step 4: Create preventive strategies

A risk action plan’s purpose is to provide you with a clear roadmap to resolving any possible difficulties that arise. The project manager and the assigned teammate should come up with an appropriate solution for each of the identified hazards. After identifying the risk, you can suggest various ways to handle it such as avoid which is changing your plan to remove the cause of the threat, a transfer which is contacting a different team or authorities, mitigate which is conducting immediate steps to reduce the impact of the risk, and lastly accept which is assuming the negative consequences and budget lost in the cost of dealing with the risk.

Step 5: Collaborating with project stakeholders

While every endeavor has some Risk, there are those where the potential negative consequences are simply too great to risk. The amount of risk your organization or stakeholders are prepared to take is known as your risk threshold. It’s critical to keep in touch with your key stakeholders while you develop your risk management strategy and get their feedback. While this may be inconvenient, it’s preferable to make adjustments now rather than later after may you have already invested time and work.

Step 6: Stay updated on the risks

This step may not be necessary for the process of formulating your risk action plan but after the implementation stage, you should know better than to immediately abandon the plan right away.

Risk Analysis and management need to be updated from time to time because you and your company are dealing with the unknown. Whoever is in charge of the risk must keep track of it, update it in the risk action plan, and ensure that others who were involved are aware of what is going on. There’s a strong possibility that new risks may emerge as your project proceeds, or that existing risks will adapt and alter. Perhaps what appeared to be a low-probability danger at first will increase and become more of a threat.

Distinguish between the Three Levels of Knowability

Although all project Risks are unplanned, only a few are unexpected. Identifying the level of the knowability of the risk that you are creating a plan for help in the later steps of the process of conducting a solution for it. This helps to set up an efficient risk action plan. Risks are classified into one of three levels based on their knowability:

The goal of a Risk action plan is to anticipate both positive and negative risks. It’s an important component of the project planning process since it keeps your team proactive rather than reactive and passive. The more you plan for the unexpected, the less likely it is that your business scheme will be derailed.

What Kinds of Business Risks Should You Prepare For?

Business is never constant, down to the stocks or market involved up to the employees busy with finishing deals and creating projects to benefit their respective companies. There is a vast scope of risks that can affect companies and these business risks presented by American Express are just one set of examples that you need to look out for. Check out the provided example of a risk action plan for a better reference.

FAQs

What are the many forms of risk management plans?

There are two most known forms which are the risk avoidance plans which incorporate steps aimed at entirely avoiding the hazards at hand by preventing them from occurring. While risk reduction plans contain actions to minimize the chance of a risk that is occurring or the consequences of it.

What is a risk action plan’s purpose?

Although they serve the same purpose to ensure your company or business faces the least amount of risks or has a plan to address the challenge, the main difference is that the risk action plan is created in the midst of the Risk Management process, between the risk evaluation and the monitoring phase.

Is a risk action plan the same as a risk management plan?

A risk assessment action plan assists you in preparing for any risks that may arise as part of a business, as well as assisting you in dealing with any challenges that may arise. A risk action plan will offer you solutions that are appropriate for the levels of risk that your company is exposed to.

Even though business risks or any type of risks that can potentially harm your company cannot be completely eliminated, through the use of a risk action plan, you are coming up with a plan to not only address it but be steps ahead to possibly lessen the damages it may cause. You need to accept that not all plans are perfect and no business is safe from experiencing challenges. But the main thought is that it can be thoroughly solved. With the risk action plan samples provided, your plans will come with ease and less hassle than starting from scratch.