6+ Sample Product Cost Proposal

-

Product Cost Allocation Proposal

download now -

Product Cost Savings Sales Proposal

download now -

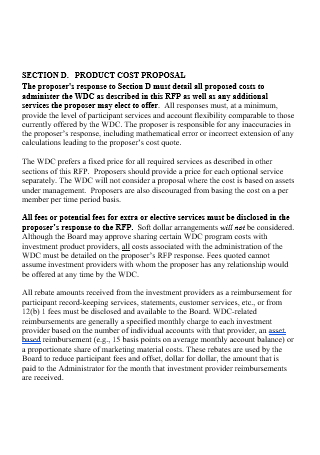

Product Cost Proposal Example

download now -

Standard Product Cost Proposal

download now -

Product Cost Proposal in PDF

download now -

Product Cost Analysis Proposal

download now -

Product Cost Proposal in DOC

download now

What Is a Product Cost?

Product cost is a word used in accounting to describe the overall expenses associated with producing and preparing a product for sale. Product expenses in manufacturing consist of expenditures for raw materials, labor, and production overhead. Product costs in retail may include fees connected to a supplier and any costs associated with stocking products. Product expenses must be disclosed in financial statements. Some require firms and individuals to disclose these costs in their financial statements because they contain overhead. So, managers may sometimes disregard overhead expenses while making short-term production and selling-price decisions. In other circumstances, managers may consider a product’s direct material costs and time in a bottleneck activity. Statistics indicate that small businesses win 38% of their offers.

Benefits of Product Costing Offers

Product costing allocates costs to inventory and production based on the expenses incurred in creating or purchasing merchandise. It is a particularly crucial process for manufacturers. There are various costing methods from which organizations can choose based on their ease of use, precision, or other criteria. If a company outsources accounting services, the accounting firm may include a comprehensive product costing study as part of its offering. There are numerous advantages to such personalized pricing.

Types of Product Cost

Product cost refers to all costs incurred by a company to develop its product or offer its services to clients. These costs are included in the company’s financial statement when they become part of the selling price of the firm’s products. Material and labor costs are direct costs, whereas factory overheads are indirect costs; all are required to produce a finished product ready for sale. By GAAP and IFRS, product costs must be capitalized as inventory on the balance sheet. They should not be expensed in the statements of income and expenses, as such costs provide benefits and value for future periods. In this section, we will examine various sorts of product costs.

Types of Pricing Strategies

Setting prices for your products requires a delicate balance. A low price is not always optimal, as a product may see a high sales volume without generating a profit. Similarly, when a product’s price is too high, a store may experience fewer sales and “price out” more budget-conscious buyers, losing market position. Ultimately, every small firm must conduct research. The art of pricing entails calculating how human behavior influences how we perceive price. To accomplish this, you will need to explore several pricing strategy examples, their psychological impact on your clients, and how to price your goods appropriately.

1. Retail price

Numerous retailers base their pricing decisions on keystone pricing (described below), which is essentially doubling the price of a product to establish a sustainable profit margin. However, depending on various conditions, you will often need to price your products more or cheaper. Although this is a very straightforward markup calculation, this pricing strategy does not apply to all products or retail businesses.

2. Keystone pricing

Keystone pricing is a simple pricing method utilized by merchants. Essentially, it is when a merchant estimates the retail price of a product by doubling the wholesale price they paid. Having keystone pricing can result in a product being priced too cheap, too high, or exactly right for your organization in various situations. With keystone pricing, you may be selling yourself short if your products have a low turnover rate, have considerable shipping and handling charges, or are distinctive or scarce. In each of these instances, a vendor might utilize a significant markup formula to boost the retail price of these popular products. However, keystone pricing may be more challenging if your products are highly commoditized and readily available elsewhere.

3. Manufacturer suggested retail price

As its name implies, the manufacturer suggested retail price (MSRP) is (no pun intended) the fee a manufacturer recommends retailers use when selling a product. Manufacturers initially implemented MSRPs to standardize product costs across many regions and merchants. Retailers frequently use the MSRP for highly standardized products. Remember that MSRP is a reasonably technical term. Although you can establish any price you choose, a significant variation from the MSRP could terminate your partnership with the manufacturer, depending on your supply agreements and their MSRP-related objectives.

4. Multiple pricing

We’ve all seen this pricing approach at grocery stores, but it’s also prevalent in clothing stores, particularly for socks, underwear, and t-shirts. Retailers sell many products for a single price using the multiple pricing technique, often known as product-bundle pricing.

5. Penetration pricing and discount pricing

It is common knowledge that consumers enjoy sales, coupons, rebates, seasonal pricing, and other discounts. As a result, 97 percent of survey respondents in a Software Advice study identified discounting as the top price strategy for retailers. There are numerous advantages to discount pricing. The more obvious ones include increasing store foot traffic, liquidating unwanted merchandise, and attracting a more price-conscious customer base. For new brands, a penetration price plan is also beneficial. A temporary price reduction is utilized to debut a new product to win market share. Many new brands are willing to sacrifice additional profit for customer awareness to gain a foothold in the market.

How To Price a Product

Pricing a product is a challenging and complex duty a product manager must complete. There are, of course, apparent drawbacks, such as pricing items excessively high and driving away customers. However, psychological elements also play a role. For instance, individuals tend to place more excellent value on more expensive products. Pricing for B2B items gets much more complex. B2 B product teams must consider the budgets of their clients’ organizations or departments. And specifically for B2B SaaS applications, pricing strategy becomes even more complex due to the abundance of pricing options. The list of possibilities is exhaustive. There is no universal pricing structure for SaaS solutions. However, your team will need to evaluate the numerous pricing models accessible to SaaS businesses, choose one to test, and then commence testing. This article addresses the subject of how to price your SaaS solution. We will also explain a procedure to assist your team in determining the optimal rates for your products.

1. Select the optimal price approach.

There are three primary pricing strategies: price based on cost, competition based on competition, and customer value. Let’s briefly examine each one. Using cost-based pricing, a company calculates the overall cost to manufacture, distribute, sell, and service a product. The corporation then determines pricing that will allow it to earn a profit over and above this total cost. However, Price Intelligently’s business intelligence platform pointed out that the cost-based pricing method has disadvantages. You may not know all of your charges, or your fees may fluctuate over time. This issue indicates that your company may price its products too cheap, resulting in a loss rather than a profit, even if it sells well. Another fault with this method is that your customers do not care about your company’s expenses. They are solely concerned with the product’s utility for them. The competitive pricing model has disadvantages as well. Pricing your SaaS goods based on those of your competitors typically results in a race to the bottom. In addition, if your SaaS solution is priced similarly to comparable goods on the market, your clients may assume that all SaaS solutions are essentially the same, even though your solution offers significant benefits that others do not. The third pricing strategy is based on the amount of customer value your product will give. This strategy is optimal for several reasons. If you can demonstrate that your product will provide substantial benefits, you may demand a higher price, and customers will be willing to pay it.

2. Develop quantitative buyer personas.

Frequently, the purchasers of B2B SaaS goods and the end-users of those products are not the same individuals. They are instead managers, department leaders, and company executives. The next stage in determining how to price your products will be to determine who these individuals are and how to reach them most effectively.

3. Calculate the average customer’s lifetime value

Lifetime value (LTV) is the entire revenue a customer will add to the bottom line of your product, less the total costs of obtaining and retaining that customer. As products and businesses mature, their overall prices stabilize, and they can begin to reap the benefits of economies of scale. When this occurs, a product team might experience increasing income streams compared to their costs, increasing average customer lifetime value. However, as Jim notes, your product’s cost-to-revenue ratio may be higher in its early years. Understanding your customer’s LTV will allow you to price your products better and strategically.

4. Choose a price structure.

SaaS providers sell their goods using various pricing strategies, so you will have several alternatives to consider. It would help if you chose a pricing model that corresponds with your customer’s goals and ability to pay when deciding on your preferred pricing plan. It would help if you also employed a price scheme that distinguishes you from the competitors.

5. Experiment and learn

You’ve identified value-based pricing as your pricing approach at this point. You have created a profile of your most valued buyer personas, estimated customer lifetime value, and selected a specific price strategy. Now is the time to put this information to the test in the market. Today, many tools and methods are available to make determining the optimal price for you and your clients simple and reasonable.

FAQs

How is cost measured?

Each part has three general costing steps: identification, allocation, measurement, and valuation. It is advised to measure economic or opportunity costs primarily from a societal standpoint. The cost category includes direct medical, direct non-medical, and indirect expenses.

What is the definition of cost?

In accounting, the cost is the monetary worth of expenditures for raw materials, equipment, supplies, services, labor, goods, etc. It is the amount documented in accounting records as an expense.

What are indirect costs?

Indirect costs are running a business that can’t be easily linked to a specific grant, contract, project function, or activity. However, they are still needed for the organization to run and do the things it does.

Writing a cost proposal can be tricky since it requires significant effort and focuses on minimizing errors and inaccuracies. Take your time to tailor your proposal to your client’s needs and writing style, and be sure to update it after you’re finished. You may also solicit assistance from a colleague in reviewing your plan. Download our free templates listed above to help you create your proposal!