9+ SAMPLE Equipment Sales Proposal

-

Equipment Product Sales Proposal

download now -

Equipment Rental Sales Proposal

download now -

Laboratory Equipment Sales Proposal

download now -

Heavy Equipment Sales Proposal

download now -

Internal Equipment Sales Proposal

download now -

Equipment Maintenance Sales Proposal

download now -

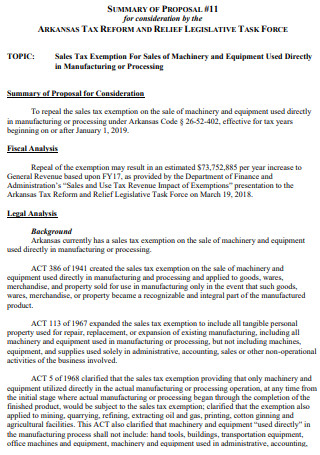

Equipment Sales Tax Summary Proposal

download now -

Equipment Sales Representative Proposal

download now -

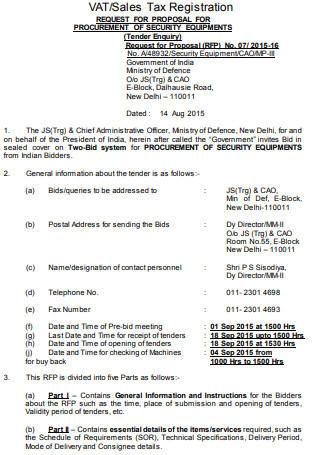

Security Equipment Sales Tax Proposal

download now -

Lab Equipment Maintenance Sales Proposal

download now

FREE Equipment Sales Proposal s to Download

9+ SAMPLE Equipment Sales Proposal

an Equipment?

Benefits of Buying New Business Equipment

Tips In Writing a Sales Proposal

How To Create an Equipment Supply Proposal

FAQs

What is a sales proposal for a product?

What is customer value?

What constitutes an effective marketing offer?

What Is an Equipment?

Equipment is most frequently referred to as a collection of tools or other objects often utilized to accomplish a specific task. Various jobs necessitate the use of a variety of different pieces of equipment. According to statistics, capital expenditures on structures and equipment grew 6.4 percent in 2019 for businesses with employees, from $108.7 billion in 2018 to $108.7 billion in 2019.

Benefits of Buying New Business Equipment

Upgrading or purchasing new equipment is critical to the growth of your organization. Businesses can reach a point where they have reached a stalemate and must invest in developing and becoming more profitable. You may be required to invest in new equipment, machinery, or cars. Taking the next step toward obtaining new equipment can be difficult and risky. Occasionally, businesses lack the finances necessary to purchase this new equipment; therefore, taking the plunge and getting an equipment finance loan may be the best course of action. There are numerous advantages to upgrading your business’s equipment. This will aid in the building of a successful business.

Tips In Writing a Sales Proposal

The importance of sales proposals in securing transactions cannot be overstated. Yet, all too frequently, sales organizations don’t know how to draft winning sales proposals, and as a result, they miss out on possibilities. Apply the following tactics to your presentations, whether you’re a new salesman or a seasoned pro, to prevent costly blunders and improve your sales performance.

-

1. Be brief

The longer your proposal is, the less possible it is that your prospect will read it all the way through. For better or worse, people have limited attention spans and will not devote the time necessary to trudge through a lengthy presentation. As a result, keep your proposal brief and to the point. A typical proposal should be between 8 and 20 pages long at most. While others say that one or two pages are sufficient, this length may not be feasible for many transactions. The size of your proposal should be determined by your company, client, and offer. The idea is to make every word matter. Look for areas where you can cut, condense, or alter. You’ll have a robust, more persuasive proposal to present once you’ve reduced the fat and refined the language.

2. Make your template unique.

Templates can save time and maintain uniformity for your staff. You’re missing an opportunity to engage with your prospect if you’re merely cutting and pasting the same boilerplate material on every proposal. It’s not about you when it comes to effective selling. It’s all about your chances. Everyone wishes to be heard and appreciated. Customizing your proposal is an easy method to demonstrate that you understand your prospects. Customize the presentation to the exceptional client as you create your submission. While some material will be nearly identical across offers, there are many opportunities to customize the request. Concentrate on their issue. Demonstrate that you better understand their problem than anyone else, and then describe how you can help them solve it. Your proposal will be more successful and clear if it is better personalized.

3. Instead of focusing on deliverables, concentrate on solving problems.

One of the most common errors salespeople make is focusing too much on the deliverables of the product or service rather than the prospect’s problem. It’s important to remember that selling isn’t about you. It all revolves around them. Emphasize your understanding of the challenges they’re seeking to solve in your proposal, and then show how your solution is the most effective method to solve those difficulties. This will far more entice a prospective customer than a list of features and perks. You’re forcing the customer to do the job of finding out how your solution will help them if you don’t go the extra mile to relate those benefits to the client and their specific pain spots. That’s a surefire way to lose a trade.

4. Give them choices.

There was just one option in traditional suggestions. However, if you don’t present different options, you can be leaving money on the table. Propose three solutions at other pricing points for the most outstanding results. This technique benefits you since it allows you to provide a variety of rates, including a higher-tier deal. Additionally, your prospective client is less likely to shop around at your competition by giving various possibilities within one proposal. This turns you into your competitor, resulting in a win-win situation. Also, prospects are happier with their final decision when they have options since they have more information and context. Simply presenting customers with a comparison of solutions at various tiers frequently leads to negotiations at a premium price. The prospect may better judge the value of the answers you’re offering and feel more confident in the one they choose by weighing each solution at various pricing points.

5. Order prices high to low

If you’re drafting a proposal, your solution will likely have enterprise-level prices, so even the cheapest offer may cause sticker shock for your prospect. List your cost points from highest to lowest to avoid scaring people away (or leaving them with a growing sense of dread). You can prevent intensifying an initial adverse reaction by starting with the most expensive option and working your way down. If you start low and work your path up to your most costly solutions, on the other hand, the prospect may get increasingly protective (and less likely to close the deal with you). This psychological tactic, albeit simple, can go a long way toward developing positive responses to your idea.

6. Make use of visuals

Humans are primarily visual beings. Images are processed 60,000 times faster in the brain than words. Take advantage of this. Visuals not only break up the monotony of a text-heavy proposal document, but they can also communicate information more quickly and efficiently. According to a study, presentations with visual aids are 43 percent more convincing than those without them. To display facts and break down complex ideas, include relevant visuals such as bar graphs, flowcharts, or tables. These graphics are examples of current and future state diagrams, a project roadmap, or documentation demonstrating how a solution will be implemented. Remember that whatever visuals you employ should be professional and consistent with your brand. Color palettes, typefaces, and visuals should be coordinated to make your proposal look more professional and convincing.

7. Maintain a straightforward approach.

Our brains are programmed to prefer ease of thought and simplicity. Cognitive fluency (or processing fluency) is a preference that affects how we make decisions and form judgments daily. Put another way; we trust people and things familiar or straightforward. And it is this bias that will determine whether your plan succeeds or fails. Competitors will be less likely to buy from you if your proposal is complex, challenging to read, or difficult to grasp. They will have to work harder to obtain and assess the data. Make sure your proposal is essential to avoid this reaction. You expand your chances of landing the deal by reducing your prospect’s mental work.

How To Create an Equipment Supply Proposal

It proposes when a material-selling corporation seeks to attract a new customer to provide materials. A proposal is a composed document that outlines the planned arrangement and specifies the sorts of materials to be provided, when and how they will be delivered, and the material and delivery costs. An excellent proposal gives the reader all the information they need to decide whether or not to accept the bid. Although there is no set measurement for a recommendation, expect it to be somewhere between two and ten pages long, depending on your industry. Basically, the longer the proposal, the more complicated or diversified your materials are.

-

1. Create an Awe-Inspiring Introduction

Write an introduction that includes a quick summary of the proposal’s contents. It discusses the issue, the proposed solution, and the advantages the reader will get by accepting it. The company producing this type of proposal should emphasize that the reader’s products and materials are available through this company. It should also state what benefits the customer will receive if he accepts the proposal, such as lower prices and faster delivery.

2. Make your proposal as detailed as possible.

In the body of the proposal, tell the reader what, how, when, and how much. All facts relating to the materials should be included in a materials supply proposal, including the particular sort of materials to be sold, delivery service, and costs. After reading the proposal, the reader must thoroughly understand the material expenses. Tell the reader how often the materials will be delivered and whether they will have to reorder or whether they will be automatically reordered.

3. Highlight the Advantages

Finish the proposal by emphasizing the customer’s advantages if they accept the offer. It should reassure the reader and demonstrate trust in the organization submitting the proposal. Explain the product’s quality and provide any available statistical information on customer satisfaction. This proposal step is the final attempt to persuade the customer to accept the proposal, so it’s critical to include facts that distinguish your company from the competition.

4. Present the Proposal

Sign the proposal and hand it over to the prospective client. Include any deadlines and offer to help the customer with queries or concerns. When the proposal is accepted, leave a blank on the bid for the customer to sign and date. Provide exceptional ongoing customer support after a client accepts your proposal. Keep an eye on his requirements as they change. Notify him right away if you have any fresh supplies that might be useful to him. To build successful business relationships and possibly gain leads, be honest and not oversell what you can’t deliver.

FAQs

What is a sales proposal for a product?

A sales proposal is an advertisement for a product or service to a prospective client. It is a convincing document, and every effort should be made to ensure that it is readable: rely on organization, editing abilities, and typography.

What is customer value?

Customer value is the customer’s opinion of a product or service’s value compared to other alternatives. The term “worth” refers to the customer’s perception that they received advantages and benefits over the price paid.

What constitutes an effective marketing offer?

An offer is beneficial in the simplest sense if it answers your target audience’s problems, needs, and interests. Additionally, this value could signify something different for offers used at various sales process stages.

Making this proposal and organizing everything from the activities to accomplishing the goal and allocating the budget could be difficult. To make things a bit easier, it’s a good idea to use all of the tools available online, including those on our site. So, what exactly are you waiting for? Take use of our templates right now!